Pay by Bank: How Account-to-Account Payments Threaten Card Interchange

Key Takeaways

- Pay by bank is account-to-account payment at checkout: open-banking software initiates a transfer directly from the customer's bank account to the merchant's, over instant rails, with no card network in the middle. Removing the network removes interchange, which is the entire economic point.

- Interchange is the per-transaction fee the card-issuing bank takes, typically the range of one and a half to roughly three and a half percent on US consumer credit. For a merchant processing large volumes, account-to-account payment that costs a flat low fee or a few cents instead of a percentage is a direct margin improvement, and that is why merchants are pushing it.

- Adoption is still slow despite the cost case, and the reasons are not technical. They are consumer protections, dispute and chargeback handling, the absence of rewards, and a checkout experience that is still clunkier than tapping a saved card. The threat to cards is real but gradual, not a cliff.

- The dispute and fraud profile is fundamentally different. A card payment is a reversible pull with strong, regulated consumer chargeback rights. An account-to-account payment is closer to an authorized push, which reduces some fraud but weakens the buyer protection that makes consumers comfortable, and that gap is the adoption bottleneck.

- The card networks are not standing still. They are buying open-banking capability, building their own account-to-account and pay-by-bank products, and leaning on the rewards, protection, and ubiquity that pay by bank cannot yet match. The likely outcome is coexistence with margin pressure, not the disappearance of cards.

Merchants Have Always Hated Interchange. Now They Have an Alternative.

For as long as cards have existed, merchants have resented the fee they pay on every transaction, and for just as long they have lacked a real alternative at the point of sale. Cash does not work online, checks are dead, and every digital option eventually routed back through the card networks and their fees. That is the constraint that is now breaking.

Account-to-account payment, branded at checkout as "pay by bank," lets a merchant pull funds directly from a customer's bank account using open-banking rails, settling over instant payment systems, with no card and no card network involved. Because the card network is not in the transaction, the interchange fee that funds the network and the issuing bank simply does not exist. For a merchant, that is not a marginal saving. On high volumes it is a structural change to the cost of accepting payment, and it is why pay by bank has moved from a fringe option to a board-level topic for both merchants and the card networks that stand to lose.

The threat is genuine, but the timeline is widely overstated. Pay by bank solves the merchant's cost problem and creates several new problems for the consumer, and those consumer-side problems, not any technical limitation, are what keep adoption gradual. This article explains how pay by bank actually works, why merchants want it and why consumers hesitate, how disputes and fraud differ from cards in ways that matter, and what the card networks are doing to defend an economic position that has been remarkably durable. A comparison table sets cards, pay by bank, and wallets side by side on cost, settlement, disputes, and reach.

How Pay by Bank Actually Works

Pay by bank is a payment where money moves directly from the buyer's bank account to the merchant's bank account, initiated through open-banking software and settled over an instant payment rail, with no card network involved. It has two technical halves that have only recently matured at the same time.

The first half is initiation. Open banking gives licensed third parties permission, with the customer's consent, to initiate a payment from the customer's bank account. At checkout, the customer chooses pay by bank, authenticates with their bank (often through the bank's own app or a biometric approval), and approves the specific payment. The open-banking provider initiates the transfer on the customer's instruction. The legal and regulatory plumbing that makes this consent-based access possible is what open-banking rules establish, and in the US that framework is set out in the CFPB's Section 1033 open-banking rule, which governs who can access account data and initiate payments and under what consent.

The second half is settlement. Once initiated, the money has to move, and move fast, or the merchant is back to waiting days for funds. This is where instant payment rails matter. A real-time rail settles the transfer between banks in seconds, around the clock, with finality. In the US the relevant rail is the central bank's instant system, explained in the primer on how FedNow real-time payments work, alongside the bank-owned instant network. Without instant settlement, pay by bank is just a slow bank transfer wearing a checkout button. With it, the merchant gets near-immediate, final funds and pays a flat low fee or a few cents rather than a percentage of the sale.

The reason pay by bank is happening now and not five years ago is that both halves reached maturity together: open-banking initiation became legally and technically routine, and instant settlement rails reached enough coverage to make the funds actually arrive in real time. Neither half alone is enough. Together they remove the card network from the transaction entirely.

Why Merchants Want It: The Interchange Math

To see why merchants are pushing pay by bank, you have to see what interchange costs them.

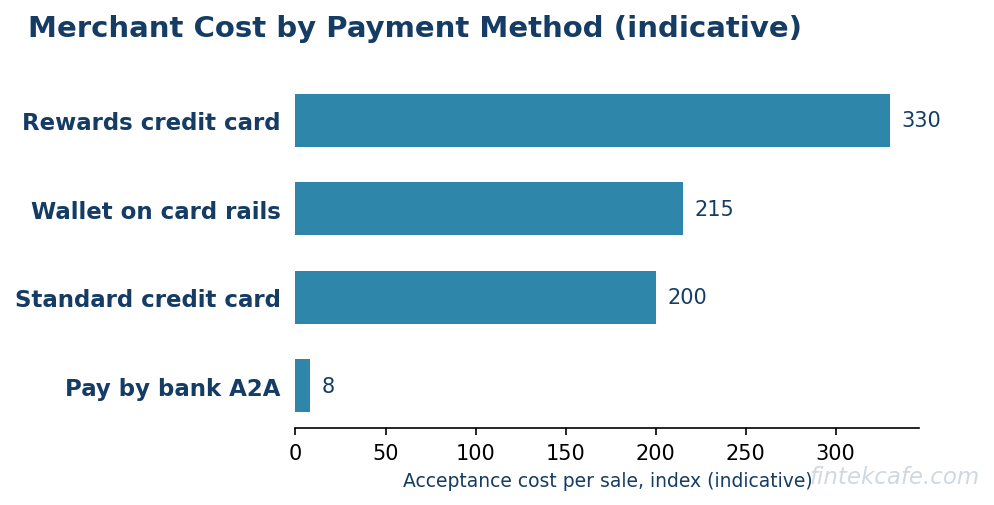

Interchange is the per-transaction fee the customer's card-issuing bank takes out of each card sale. It is the largest single component of what a merchant pays to accept a card, and on US consumer credit cards it commonly runs in the range of one and a half to roughly three and a half percent of the transaction, with rewards cards at the higher end because the fee funds the rewards. On top of interchange sit network assessment fees and the processor's markup, but interchange is the big number and the one that scales directly with sales.

Pay by bank replaces a percentage with something close to a fixed cost. An account-to-account transfer over an instant rail costs the merchant a flat fee measured in cents, or a small flat charge, rather than a percentage of the basket. The larger the transaction and the higher the volume, the more dramatic the difference. A merchant selling high-ticket items or processing large recurring payments can see payment-acceptance costs fall by a large multiple, and for thin-margin businesses that difference can be the difference between losing and making money on a sale.

There is a second merchant benefit beyond cost: settlement speed and cash flow. Card settlement typically arrives a day or more after the sale, and the funds can be reversed for months through chargebacks. Instant-rail settlement arrives in seconds with finality, which improves cash flow and removes a category of reversal risk. For merchants squeezed on working capital, faster final funds are worth real money on their own. This is part of why payment acceptance is increasingly bundled directly into software platforms rather than bolted on, a shift covered in the analysis of embedded finance and where it is heading, because the platform that controls checkout can route to the cheapest rail.

Why Adoption Is Still Slow

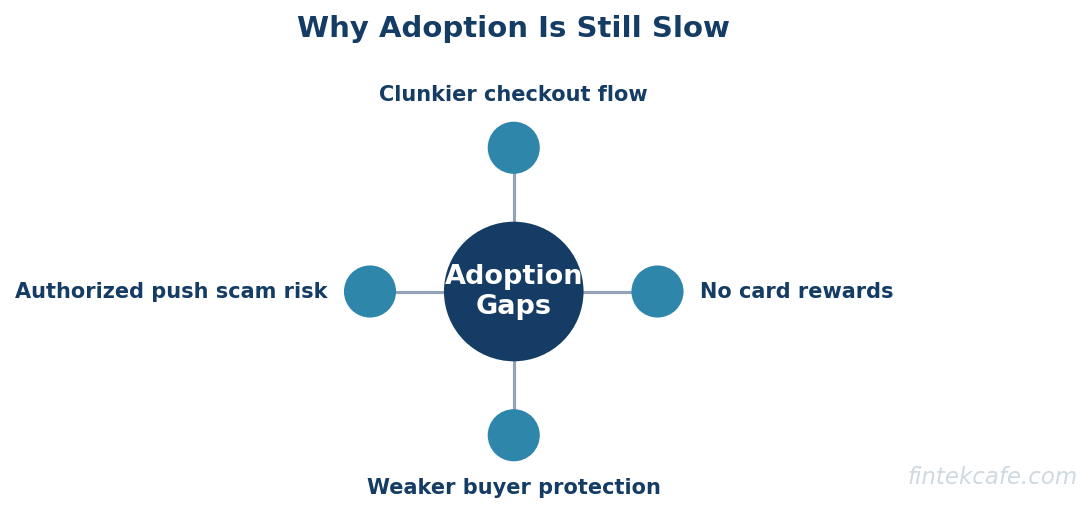

If pay by bank is so much cheaper for merchants, the obvious question is why it has not taken over. The answer is that merchants do not get to decide alone. Consumers do, and consumers have little reason to switch and several reasons not to.

Consumer protection is the first and largest gap. When a card purchase goes wrong, the buyer disputes the charge and, in most consumer cases, gets their money back while the card network and issuer sort it out. That chargeback right is a powerful, regulated form of buyer protection, and consumers have internalized it even if they could not name it. A pay-by-bank transfer, as an authorized push of funds, does not carry the same automatic, network-backed reversal right. The protections that exist are weaker and less familiar, and for any purchase a consumer is nervous about, that gap is decisive.

Rewards are the second gap. A large share of consumers use a particular card precisely because it pays them cash back or points, funded by the very interchange that pay by bank eliminates. Asking a rewards-motivated consumer to pay by bank is asking them to give up the rebate and take on more risk to save the merchant a fee they never see. Without a compelling incentive routed back to the consumer, the rational choice is to keep using the card.

User experience is the third gap. Tapping a saved card or a wallet is one motion. Pay by bank still often requires selecting a bank, authenticating in a separate app, and approving, which is more friction at the exact moment friction costs conversions. The experience is improving, but it is not yet as frictionless as the incumbent it is trying to displace, and at checkout, friction loses.

The honest assessment is that pay by bank has solved the merchant's problem and not yet solved the consumer's. Until the consumer gets protection comparable to a card, an incentive to offset lost rewards, and an experience as smooth as tapping, adoption grows steadily rather than suddenly. The threat to card economics is real, but it arrives as gradual margin pressure, not as a cliff.

The Dispute and Fraud Profile Is Different

The difference between a card payment and a pay-by-bank payment is not only who collects the fee. It is the direction of the money and the rights attached to it, and that changes the entire risk profile.

A card payment is a pull authorized by the cardholder, and it sits inside a mature, regulated dispute framework. If the goods never arrive, if the charge is fraudulent, or if the merchant misbehaves, the cardholder initiates a chargeback and the system is built to reverse the funds. This protects consumers strongly and pushes fraud and dispute costs onto merchants and the card ecosystem, which is precisely what funds part of the interchange fee.

A pay-by-bank payment is closer to an authorized push: the customer instructs their bank to send money, and once it settles on an instant rail, it is final. This cuts certain fraud types that depend on stolen card credentials, because there is no card number to steal and the customer authenticates directly with their bank. But finality is a double-edged property. It reduces some fraud and chargeback abuse for the merchant, and it removes the consumer's easy reversal path. The fraud that remains shifts toward authorized push payment fraud, where a victim is socially engineered into approving a payment to a fraudster, and that category is harder to reverse precisely because the customer did authorize it.

For executives weighing pay by bank, the practical implication is that the dispute and fraud question is not "is it safer," but "safer for whom, and against which threat." Pay by bank reduces credential-theft fraud and chargeback abuse against the merchant, and it weakens the consumer's protection and shifts risk toward authorized-push scams. Who carries the loss when a pay-by-bank payment goes wrong is still being settled by regulation and scheme rules, and that unsettledness is itself a reason cautious consumers and merchants hesitate. The same reporting and data-sharing dynamics reshaping consumer finance more broadly, such as the shift toward BNPL reporting to credit bureaus, show how quickly the rules around newer payment methods can change once regulators engage.

Cards vs Pay by Bank vs Wallets

The three options at checkout differ on the axes a decision-maker actually cares about: what it costs, how fast and final the money is, what protection the buyer has, and how widely it is accepted.

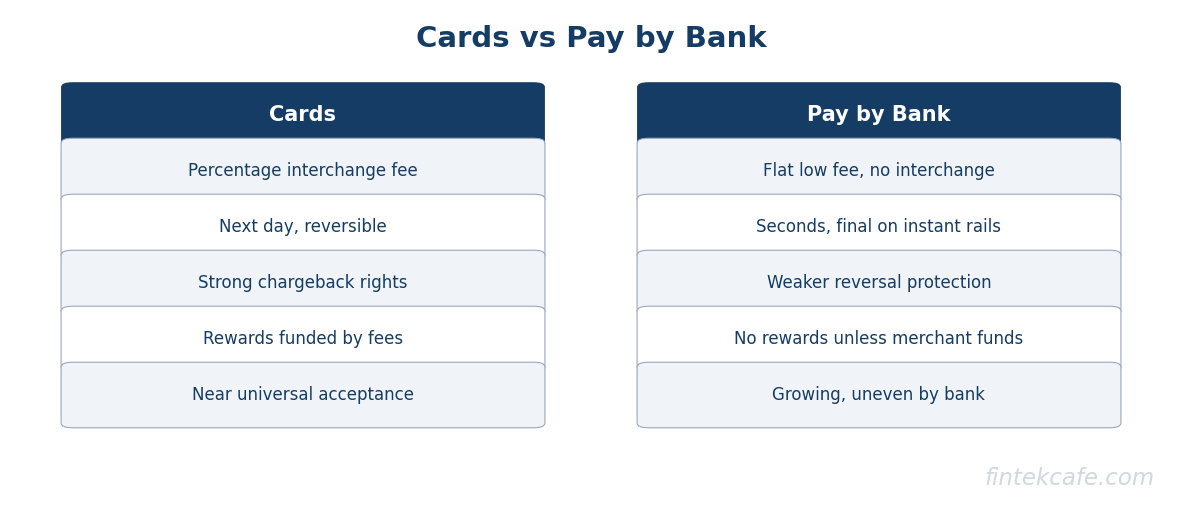

| Dimension | Cards | Pay by bank (A2A) | Wallets (Apple Pay, etc.) |

|---|---|---|---|

| Merchant cost | Percentage interchange plus fees, often one and a half to over three percent | Flat low fee or a few cents, no interchange | Card cost plus possible wallet fee, rides card rails |

| Settlement | Next day or later, reversible for months | Seconds, final, on instant rails | Same as the underlying card |

| Consumer protection | Strong, regulated chargeback rights | Weaker, no automatic network reversal | Inherits card chargeback rights |

| Fraud profile | Credential theft, chargeback abuse | Lower credential fraud, higher authorized-push scam risk | Tokenized, strong device authentication |

| Rewards | Common, funded by interchange | None unless merchant funds an incentive | Inherits card rewards |

| Consumer experience | Familiar, saved cards are one tap | Improving, often multi-step authentication | Very smooth, biometric one tap |

| Reach and acceptance | Near universal | Growing, uneven by market and bank | Wide on supported devices |

The table makes the strategic picture clear. Pay by bank wins decisively on merchant cost and settlement speed and loses on protection, rewards, experience, and reach. Wallets, importantly, mostly ride the card rails and therefore carry card economics, which is why the network's real threat is account-to-account, not wallets. The competition is not card versus wallet. It is card-rail versus bank-rail.

What the Card Networks Are Doing to Defend

The card networks have watched this coming and are not defending passively. Their response runs on three tracks.

The first is to own the rails that threaten them. Rather than let open-banking initiation and account-to-account payment develop entirely outside their control, the networks have acquired open-banking providers and account-to-account capabilities, positioning themselves to offer pay by bank as a product they monetize, so that even a transaction that bypasses interchange can still run through network infrastructure they charge for. If account-to-account payment is inevitable, the networks intend to be in the middle of it.

The second is to compete on the things pay by bank cannot yet match: consumer protection, rewards, and dispute handling. The networks' core asset is consumer trust built on decades of reliable buyer protection, and they are emphasizing exactly the gaps where pay by bank is weakest. As long as the consumer who pays by card knows they can reverse a bad charge and earn rewards, the network has a defensible reason for that consumer to keep tapping a card.

The third is ubiquity and integration. Cards are accepted nearly everywhere, tokenized into every wallet, and embedded in every recurring subscription, and that incumbency is a moat that account-to-account payment has to overcome merchant by merchant and bank by bank. The networks are also modernizing the underlying messaging and data standards, the kind of upgrade reflected in the broader ISO 20022 migration reshaping bank technology stacks, to keep card-based payments rich in data and competitive on capability rather than only on habit.

The realistic forecast is coexistence with sustained margin pressure rather than displacement. Pay by bank will take share in the places where its cost advantage is largest and consumer protection matters least: high-value purchases, bill pay, account funding, and merchant categories where rewards and disputes are not decisive. Cards will hold the everyday consumer purchase where protection, rewards, and one-tap habit still win. The interchange that merchants have resented for decades will not vanish, but for the first time it faces a credible alternative, and the mere existence of that alternative is already a lever in every merchant's negotiation.

FAQ

What is pay by bank?

Pay by bank, also called account-to-account or A2A payment, is a checkout method where money moves directly from the customer's bank account to the merchant's bank account. Open-banking software initiates the transfer with the customer's consent, and an instant payment rail settles it in seconds. Because no card network is involved, there is no interchange fee, which is the main reason merchants are interested in it.

How is pay by bank different from a card payment?

A card payment routes through a card network, which charges interchange (often well over one percent), settles next day or later, and gives the consumer strong chargeback rights. Pay by bank skips the network, costs the merchant a flat low fee, settles instantly and finally, and gives the consumer weaker reversal protection. In short, pay by bank is cheaper and faster for the merchant but offers less built-in buyer protection.

Why are merchants pushing account-to-account payments?

Merchants pay interchange on every card sale, commonly in the range of one and a half to over three percent. Account-to-account payment replaces that percentage with a flat low fee, which is a large saving at scale, especially on high-value or high-volume transactions. Merchants also gain faster, final settlement over instant rails, which improves cash flow and removes months-long chargeback reversal risk.

Is pay by bank safe for consumers?

It reduces some fraud types, since there is no card number to steal and the customer authenticates directly with their bank, but it carries less buyer protection than a card. A settled account-to-account payment is final and lacks the automatic, network-backed chargeback right that cards provide, and fraud risk shifts toward authorized-push scams where a victim is tricked into approving a payment. The protection gap is the main reason cautious consumers stick with cards.

Will pay by bank replace credit cards?

Most likely not outright. The realistic outcome is coexistence with margin pressure on cards. Pay by bank will take share where its cost advantage is largest and protection matters least, such as high-value purchases, bill pay, and account funding, while cards hold everyday purchases where rewards, chargeback protection, and one-tap convenience still win. The card networks are also building their own account-to-account products to stay in the transaction.

Related reading on FinTekCafe

Related Articles

The Consortium Stablecoin: Why the Card Networks Are Funding Their Own Disruption

Visa, Mastercard, and Stripe are backing an open stablecoin consortium. The playbook is older than it looks: own the new rail's governance before it owns you.

Merchant of Record vs Payment Facilitator: Who Holds the Risk in Your Payment Stack

The four payment models compared: who holds tax, chargeback, and compliance liability as merchant of record, payfac, marketplace, or processor, and which fits.

Interchange Fees Explained: Who Really Pays for Card Payments

What interchange fees are, who pays whom in the four-party model, why rates vary, what regulation changed, and how merchants realistically cut card costs.