What Is FedNow? The Fed's Real-Time Payments Rail and Why Adoption Is Stalling in 2026

FedNow launched in July 2023 as the Federal Reserve's long-awaited entry into real-time payment infrastructure. The premise was straightforward: the United States had fallen behind peer economies in instant payment capabilities, The Clearing House's RTP network had spent five years building without achieving universal bank coverage, and the Federal Reserve's participation would bring the institutional credibility, existing bank relationships, and access framework needed to drive adoption across the full banking system, including the community banks and credit unions that had been largely left out of RTP's early rollout.

Three years in, the honest assessment is this: FedNow is real infrastructure, technically sound, and meaningfully deployed. It is also stalling at exactly the tier of the banking system where adoption matters most, for reasons that are structural rather than technical. The model, the mechanics, and the messaging are not the problem. The problem is that the business case for mid-tier regional banks is genuinely ambiguous, the integration costs are high relative to near-term revenue, and the competitive pressure that typically forces infrastructure adoption has not materialized evenly across markets.

Executives at financial institutions evaluating FedNow, payment vendors building on real-time rails, and corporate treasury professionals considering whether to migrate payment workflows need a clear-eyed view of what FedNow is, how it compares to alternatives, what the barriers to adoption actually are, and what the trajectory looks like over the next two to three years.

How FedNow Works: Settlement Mechanics

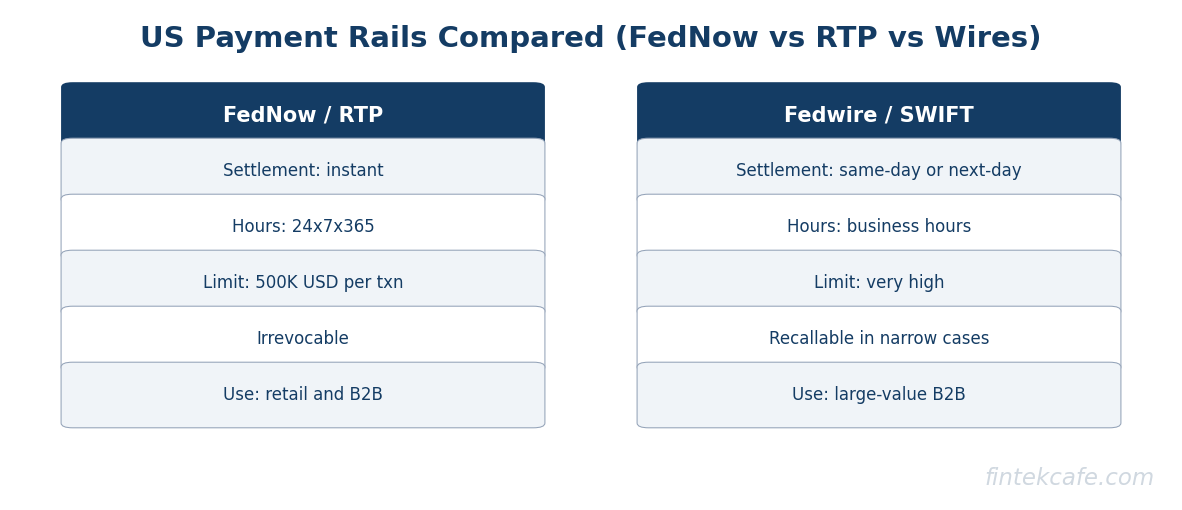

FedNow is a real-time gross settlement (RTGS) system. Unlike ACH, which batches transactions and settles in net positions multiple times per banking day, FedNow settles each payment individually and immediately using funds held in Federal Reserve master accounts.

The settlement process works as follows. When a consumer or business initiates a FedNow payment through their bank's application, the originating bank sends a payment message to the FedNow service. The Federal Reserve verifies that the originating bank holds sufficient funds in its master account, debits that account, and credits the receiving bank's master account. The receiving bank is then obligated to credit the end recipient within seconds. The full settlement cycle targets completion under ten seconds from initiation.

Three characteristics define FedNow's architectural properties.

Irrevocability. Once a FedNow payment settles, it cannot be recalled through the payment system by the originating institution. This property is foundational to the real-time model: the receiving bank credits the recipient immediately because it has received final settlement from the Federal Reserve and carries no counterparty risk. The trade-off is that fraud, misdirected payments, and social engineering losses cannot be reversed through standard payment system procedures. Recovery requires voluntary cooperation from the recipient.

24/7/365 availability. FedNow operates continuously, including weekends, federal holidays, and outside normal banking hours. This is a structural departure from ACH, which observes banking business days and has defined processing windows, and from Fedwire Funds, which has limited daily operating hours. Always-on availability enables use cases that were not practical on traditional rails, including same-day payroll for weekend shifts, emergency vendor payments, and real-time insurance claim disbursements.

Transaction size limits. FedNow sets published per-transaction maximum amounts that financial institutions may configure within. Individual bank configurations vary by customer segment and product. Very large corporate treasury transactions above these limits continue to route to Fedwire Funds, which has no practical upper cap and serves as the high-value settlement layer.

For a deeper look at how FedNow fits into the broader US payment infrastructure, see How ACH Payments Work and Real-Time Payments Explained.

FedNow vs. RTP vs. SWIFT gpi: The Rail Comparison

Three real-time or near-real-time rails are relevant to most US financial institutions evaluating instant payment strategy. Understanding the structural differences is prerequisite to any infrastructure investment decision.

| Dimension | FedNow | RTP (The Clearing House) | SWIFT gpi |

|---|---|---|---|

| Operator | Federal Reserve | The Clearing House (privately owned by large banks) | SWIFT cooperative |

| Geographic scope | US domestic | US domestic | Cross-border, multi-currency |

| Settlement model | Real-time gross settlement | Real-time gross settlement | Correspondent banking with tracking overlay |

| Availability | 24/7/365 | 24/7/365 | Depends on correspondent chain |

| Irrevocability | Yes | Yes | Varies by message type and corridor |

| Participant model | Any Fed master account holder | Must contract directly with TCH | SWIFT member financial institutions |

| Launch year | 2023 | 2017 | 2017 (tracking overlay); expanded since |

RTP, operated by The Clearing House, has a five-year head start on FedNow. As of 2026, RTP has broader penetration among large and mid-tier banks, particularly those owned by or affiliated with TCH's bank shareholders. FedNow's structural advantage is the Federal Reserve's direct relationships with community banks and credit unions, which maintain master accounts with the Fed and are deeply embedded in the existing Federal Reserve operational network. These institutions, numbering several thousand, are the primary source of FedNow's current participant growth.

SWIFT gpi addresses a different workload: cross-border, multi-currency corporate payments. It is not a real-time rail in the same sense as FedNow or RTP, but the gpi overlay adds end-to-end tracking, same-day credit commitments, and fee transparency to the correspondent banking network. For US institutions with significant international payment volumes, gpi is complementary to domestic instant rails rather than competitive with them.

For more on cross-border payment infrastructure, see SWIFT vs. SEPA vs. UPI and Cross-Border Payments Explained.

Adoption Reality: The Numbers and the Gaps

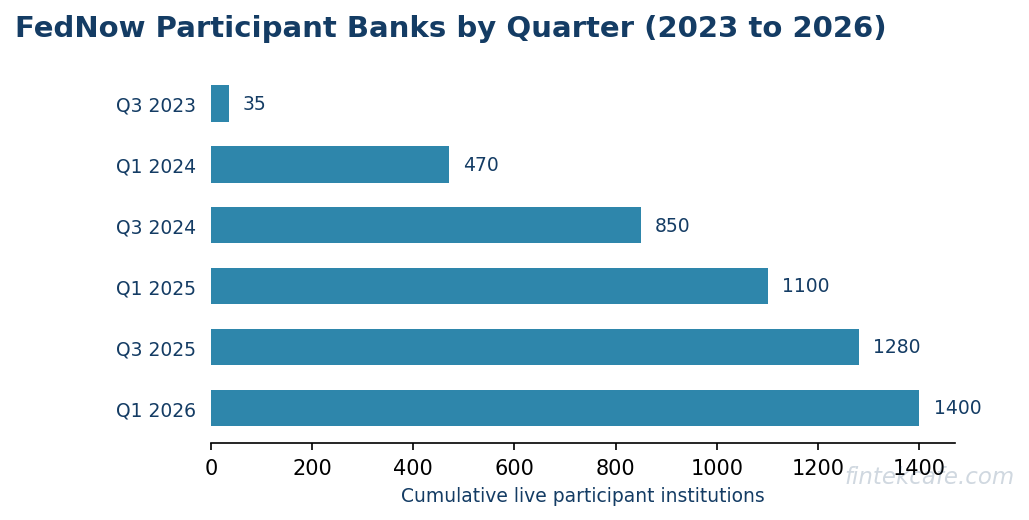

The Federal Reserve publishes a participant directory listing institutions connected to FedNow as senders, receivers, or both. As of early 2026, the directory lists over 1,000 financial institutions, per Federal Reserve published data.

That number sounds substantial until placed in context. The United States has approximately 4,500 commercial banks and over 4,700 credit unions, totaling roughly 9,200 federally chartered or federally insured depository institutions. Current FedNow participation represents approximately 10 to 12 percent of that universe.

More telling is the participation structure. FedNow adoption skews heavily toward community banks and credit unions, where the Federal Reserve's existing relationships are strongest. Coverage among mid-tier regional banks, those in the range of USD 1 billion to USD 100 billion in assets, is materially lower as a share of institutions in that tier. Among large banks, the picture is uneven: some have connected on both the send and receive sides, while others have joined as receive-only participants, which limits the utility they can offer to business customers seeking to initiate payments.

Receive-only participation is a structural constraint on ecosystem value. A corporate treasurer cannot use FedNow to initiate time-sensitive vendor payments if their bank participates only as a receiver. The network effects that make instant rails genuinely useful, the ability to send to and receive from anyone, only activate when both the sending and receiving bank are fully participating.

Why Mid-Tier Banks Are Stalling

The mid-tier regional bank segment, roughly 400 to 600 institutions in the USD 1 billion to USD 50 billion asset range, is where FedNow adoption is most consequential and most stalled. These banks collectively serve the bulk of American small and medium-sized businesses. Their FedNow participation largely determines whether real-time payments become a practical tool for commercial customers or remain a consumer-facing novelty.

Three structural barriers explain the stall.

Core Integration Cost

FedNow connectivity requires integrating the bank's core banking system with the FedNow service. Most mid-tier banks run legacy core banking platforms from vendors including FIS, Fiserv, and Jack Henry. These vendors have developed FedNow connectivity modules, but deploying them requires a core upgrade or integration project that typically involves months of work and significant consulting and licensing fees.

Banks that recently completed an RTP integration have limited appetite for a second major core connectivity project within a few years, particularly when the incremental business case for FedNow connectivity on top of existing RTP access is unclear. The ROI calculation depends on customer demand for FedNow specifically, which is difficult to forecast when most end users cannot distinguish between RTP and FedNow at the application layer.

Fraud Exposure on Irrevocable Rails

Real-time gross settlement is irrevocable by design. This property makes instant payments useful. It also makes fraud losses expensive in ways that differ qualitatively from ACH.

On ACH, misdirected payments and many fraud scenarios are recoverable through reversal requests within defined windows. On FedNow and RTP, once payment settles, the funds are the recipient's. If the recipient is a fraudster, or if the payment was authorized under social engineering such as an impersonation scheme, the sending institution may bear restitution liability for retail customers protected by applicable consumer protection regulations.

Mid-tier banks with limited fraud operations infrastructure face a specific risk: enabling send-side FedNow access for retail and small business customers without first investing in real-time fraud detection that can make a risk decision in under two seconds. Investment in transaction monitoring, behavioral analytics, and customer authentication capable of operating at the speed of instant payments is a prerequisite for safely enabling FedNow send access. Many institutions have not made that investment.

ROI Ambiguity

The business case for FedNow investment is genuinely unclear for many mid-tier institutions. FedNow does not generate direct fee income for sending banks; the Federal Reserve charges per-transaction fees to the bank, and most consumer-facing instant payment products are not priced to recover those fees plus a margin. The primary ROI case rests on customer retention and competitive differentiation from institutions that offer instant payment capabilities.

For banks in markets where competing institutions are also slow FedNow adopters, competitive pressure is low. The ROI case strengthens materially when a competitor enables real-time payroll credit or real-time vendor payment initiation and begins winning commercial accounts on that basis. Until that competitive pressure materializes in a specific bank's local or regional market, the investment is difficult to justify on financial metrics alone.

What UPI and Pix Got Right

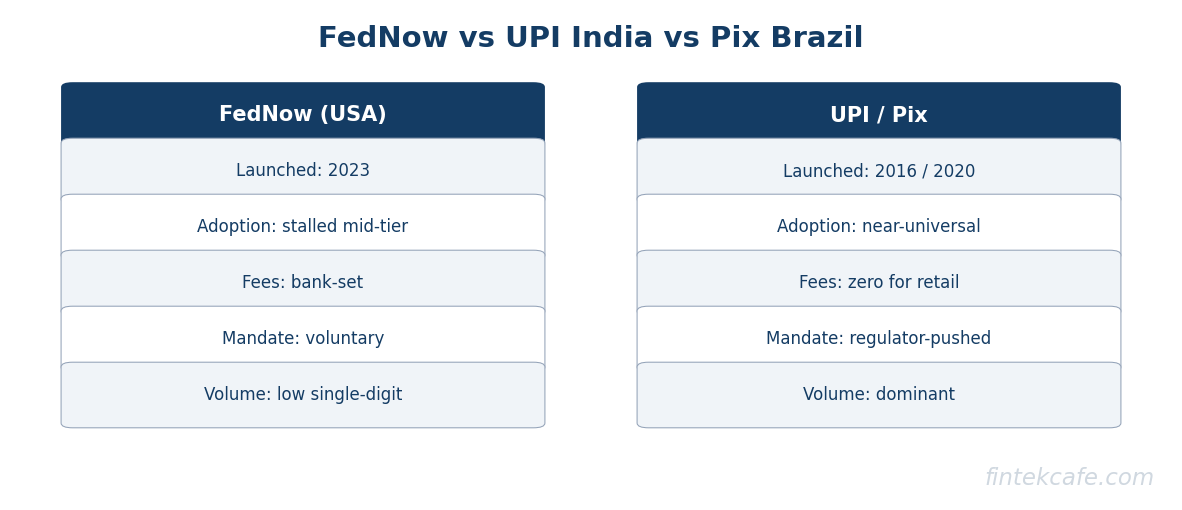

Two global instant payment systems, India's Unified Payments Interface (UPI) and Brazil's Pix, achieved rapid and broadly distributed adoption that FedNow has not replicated. Both offer instructive contrasts with the US voluntary participation model.

UPI was launched in 2016 by the National Payments Corporation of India. Adoption was driven by two factors with no direct US equivalent. First, the regulatory framework effectively required participation from scheduled commercial banks, eliminating the ROI ambiguity that stalls voluntary adoption. Second, the demonetization policy of November 2016, which removed high-denomination currency notes from circulation, created an acute and immediate demand shock that pushed both consumers and merchants onto digital rails within weeks. By the mid-2020s, UPI was processing billions of transactions per month, per NPCI monthly data releases.

Pix was launched by Brazil's central bank in November 2020 with mandatory participation for all financial institutions above a defined asset threshold. Mandatory participation solved the chicken-and-egg problem that voluntary frameworks struggle to overcome: every Brazilian bank account holder could receive Pix from day one, which meant every consumer had practical access. Adoption became near-universal within two years of launch.

The common thread is regulatory compulsion. Both UPI and Pix used central bank authority to require participation, eliminating the ROI ambiguity and competitive dynamics that characterize voluntary adoption. The Federal Reserve has not compelled FedNow participation, and the political and regulatory context in the United States makes mandatory participation unlikely in the near term. Commercial pressure, which operates more slowly than regulatory mandates, is the primary adoption mechanism available.

For context on global payment standards and how they interact with instant rails, see ISO 20022 Guide.

Participant-Tier Readiness Checklist

For financial institutions evaluating FedNow readiness, the following checklist covers key preparedness dimensions across four domains.

Technical readiness: - Core banking vendor has a certified FedNow connectivity module available and tested - Federal Reserve master account is in good standing with adequate intraday liquidity buffers - Integration and load testing with the FedNow pilot environment is completed - End-to-end API connectivity to the FedNow service is verified and documented

Fraud and risk readiness: - Real-time transaction monitoring is capable of rendering a risk decision within two to three seconds - Out-of-pattern transaction alerting is configured for instant payment channels separately from batch channels - Customer authentication step-up logic for high-value transactions is defined and tested - Irrevocability is documented in customer-facing terms and service agreements

Operational readiness: - 24/7 operations coverage for payment monitoring and exception handling is confirmed - Customer service protocols for misdirected and disputed payments are documented - Dispute escalation process accounts for the absence of a standard reversal mechanism - Regulatory compliance review is completed for applicable state money transmission requirements

Business readiness: - Fee model for instant payments is defined across consumer and business customer segments - Product and marketing materials reflecting FedNow capabilities are updated - Commercial relationship managers are trained on FedNow use cases, limitations, and the distinction from RTP

Key Takeaways

- FedNow settles each payment individually in real time through Federal Reserve master accounts; once settled, payments are irrevocable with no standard reversal mechanism.

- Over 1,000 institutions have joined FedNow per Federal Reserve published participant data, representing roughly 10 to 12 percent of US depository institutions; mid-tier regional banks are the critical gap.

- Three structural barriers explain mid-tier stall: core integration cost, fraud exposure on irrevocable rails, and ROI ambiguity in the absence of local competitive pressure.

- RTP has a five-year head start and stronger penetration among large and mid-tier banks; FedNow has stronger traction among community banks and credit unions through existing Federal Reserve relationships.

- UPI and Pix achieved rapid universal adoption through mandatory participation frameworks; the US voluntary model produces slower and uneven coverage that self-reinforces through network effect gaps.

- Receive-only participation does not create network effects; full adoption requires send-and-receive participation from the banks on both sides of a transaction.

FAQ

What is the difference between FedNow and Zelle?

Zelle is a consumer-facing payment application operated by Early Warning Services, owned by a consortium of large banks. It routes payments across the banking system using ACH and, increasingly, RTP rails. FedNow is the underlying settlement infrastructure on which applications like Zelle can be built. Zelle is a product layer; FedNow is settlement plumbing. Consumers interact with Zelle; banks and payment vendors interact with FedNow.

Can businesses use FedNow today?

Yes, with constraints. Businesses can receive FedNow payments and, if their bank offers it, initiate FedNow payments to vendors, employees, or customers. The primary constraint is bilateral participation: both the sending and receiving banks must be FedNow participants for the payment to route successfully. Many mid-tier and smaller regional banks do not yet offer send-side FedNow access to commercial customers.

Is fraud a bigger problem on FedNow than on ACH?

The risk profiles differ rather than one being simply larger. ACH fraud is often recoverable through reversal windows, which caps loss exposure but also enables certain fraud patterns that exploit the delay. FedNow fraud is irrevocable, which eliminates the reversal window as a recovery mechanism and concentrates risk in authorization-time decisions. Authorized push payment fraud, where the legitimate account holder is deceived into authorizing a payment to a fraudster, is particularly challenging on instant rails and requires investment in customer education and pre-authorization detection.

How does FedNow handle payments sent to the wrong account?

There is no automated reversal mechanism in FedNow. If a payment is sent to an incorrect account number, the sending bank must contact the receiving bank and request voluntary return of funds by the account holder. The Federal Reserve can facilitate communications between institutions but does not compel fund return. This is a material operational risk for treasury teams migrating high-value recurring payment workflows to instant rails without appropriate pre-payment account validation steps.

Will FedNow adoption become mandatory?

The Federal Reserve has not indicated plans to mandate participation. The more likely path to broad adoption is competitive pressure: as more institutions enable FedNow on the send and receive sides, non-participating banks face growing customer attrition from businesses and consumers who expect instant payment capabilities from their primary financial institution. Commercial pressure has historically been a more effective adoption mechanism in the US banking context than regulatory mandates for domestic payment rails, but it operates on a longer timeline than the regulatory compulsion that drove UPI and Pix adoption.

Related Articles

The Consortium Stablecoin: Why the Card Networks Are Funding Their Own Disruption

Visa, Mastercard, and Stripe are backing an open stablecoin consortium. The playbook is older than it looks: own the new rail's governance before it owns you.

Merchant of Record vs Payment Facilitator: Who Holds the Risk in Your Payment Stack

The four payment models compared: who holds tax, chargeback, and compliance liability as merchant of record, payfac, marketplace, or processor, and which fits.

Interchange Fees Explained: Who Really Pays for Card Payments

What interchange fees are, who pays whom in the four-party model, why rates vary, what regulation changed, and how merchants realistically cut card costs.