How ISO 20022 Migration Reshapes Bank Technology Stacks Through 2027

Key Takeaways

- The SWIFT MT to MX coexistence window for cross-border payments closed in November 2025. Most large banks completed the messaging-gateway cutover before the deadline. The harder work, rewiring the systems downstream of the gateway, runs through 2027.

- The migration is not a messaging project. It is a data-model project. ISO 20022 carries structured fields where MT carried free-form text, which forces schema changes in payment hubs, sanctions screening, anti-money-laundering pipelines, fraud models, reconciliation systems, and customer-facing channels.

- The vendor scramble has clarified into two camps: incumbents (Volante, Bottomline, Finastra, FIS) competing on coverage and integration depth, and cloud-native payment-hub vendors pitching greenfield deployments to second-wave banks. Most large banks are buying the incumbent and rebuilding around it.

- Banks that finish migration in 2026 should be prioritizing data utilization, the actual reason ISO 20022 exists. Banks finishing in 2027 should be prioritizing minimum viable compliance, the structured fields that screening and reconciliation must consume, and deferring richer-data use cases.

- The post-coexistence opportunity is not a payment-rail story. It is a downstream-data story: ML on structured remittance fields, automated settlement instructions, lower false-positive rates in screening, and reconciliation systems that close the day without manual investigation queues.

The Coexistence Window Has Closed: Now What

For five years the SWIFT cross-border migration to ISO 20022 was discussed in terms of a deadline. The deadline, after one extension, was November 2025. As of May 2026, the coexistence window has been closed for six months. SWIFT cross-border payment instructions now flow as ISO 20022 messages (the MX format). The MT-format equivalents that banks relied on for four decades are no longer accepted on the network.

Most large banks crossed the deadline. The messaging-gateway cutover (translating internal payment flows into MX and parsing inbound MX traffic back to internal formats) was the visible piece. Some banks built it in-house. Most bought it from a payments vendor. Either way, by November 2025 the gateway was the front door of an otherwise unchanged stack.

The harder problem is everything behind the gateway. ISO 20022 messages carry structured fields where MT messages carried free-form text concatenated into 35-character lines. The downstream systems (payment hubs that orchestrate the flow, screening engines that check sanctions and watch lists, AML pipelines that score for suspicious activity, fraud models that look at counterparty and corridor risk, reconciliation systems that match settlements) were built to consume the legacy data shape. They now receive a richer shape they cannot fully use, often via a translation layer that flattens the new fields back into the old format and discards the structure.

That gap, between the messaging gateway being live and the downstream systems being upgraded to consume the richer data, is the work of 2026 and 2027. Banks that treat the deadline as the finish line will miss the point. Banks that treat the deadline as the start line are doing the harder project.

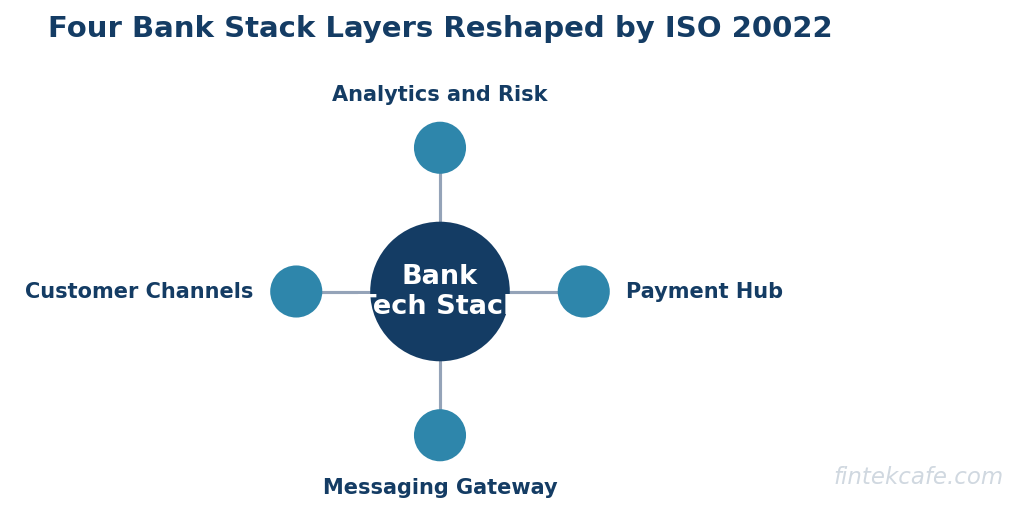

The Four-Layer Tech-Stack Impact

ISO 20022 touches four distinct layers in a bank's payment stack. Each has its own migration shape, its own vendor landscape, and its own definition of done.

Layer One: Messaging Gateway

The gateway is the integration point with SWIFT (and increasingly with domestic real-time payment rails that have already moved to ISO 20022, including TARGET2, CHAPS, Lynx, Fedwire ISO 20022, and most of the European instant-payments schemes). It handles message parsing, validation, format conversion, and routing.

The gateway work was the most visible part of the migration and is largely complete for the first wave. The interesting question now is whether the gateway exposes the full ISO 20022 schema downstream or collapses it back into the bank's internal format. Many gateways, under deadline pressure, were configured to do the latter. That choice protected the downstream systems from change. It also threw away the data the rest of the migration depends on.

A gateway that flattens MX messages back into MT-equivalent fields is a gateway that has to be revisited.

Layer Two: Payment Hub

The payment hub is the central orchestrator. It receives the parsed message from the gateway, applies business logic (correspondent-bank routing, fee calculation, currency conversion, value-date computation), invokes screening and AML services, and produces the outbound message for the next hop.

The hub is where the structured-data benefit either materializes or evaporates. A modern hub treats ISO 20022 as a first-class internal model: structured remittance information, structured party identification, structured purpose codes. A legacy hub treats ISO 20022 as a translation problem to be solved at the boundary, with the internal model unchanged.

Most banks are mid-rebuild of the hub. The vendor landscape (covered below) reflects this. The decision turns on whether to upgrade the existing hub vendor's product, replace the hub with a different vendor, or keep the hub and bolt a translation service on top.

Layer Three: Downstream Analytics and Risk

This layer is where the deadline-driven thinking did the most damage. Sanctions screening, AML transaction monitoring, fraud scoring, and reconciliation all consume payment data. They were built against legacy field structures. Updating them to consume the richer ISO 20022 fields is a multi-quarter project per system.

The early returns are visible. Sanctions screening systems that began consuming structured purpose codes and structured party identification have reported false-positive rate reductions of meaningful magnitude (industry reports cite figures of 30 percent or more for some workloads). AML models that have access to structured remittance information have richer features for typology detection. Fraud models can incorporate corridor and counterparty patterns that were buried in unstructured text.

These benefits do not arrive automatically. They arrive when the screening engine is upgraded, the AML feature store is extended, and the fraud team retrains models on the new data shape. None of that is a 2025 project. All of it is a 2026 and 2027 project.

Layer Four: Customer-Facing Channels

The last layer is where the corporate treasury and retail customer encounter the data. Corporate banking portals can now display structured remittance information cleanly. Bulk payment files can carry structured purpose codes that flow through the entire chain without being lost. Pre-validation services (verifying account name against account number before sending) become operationally cleaner with structured fields.

This layer is the most direct revenue argument for the migration. Corporate treasurers value the ability to reconcile payments automatically. The bank that delivers that capability earns retention. The bank that delivers ISO 20022 at the gateway but does not surface it to the customer earns nothing.

The Vendor Scramble

The vendor landscape clarified during 2024 and 2025 into two camps with different pitches.

Incumbent payment-hub vendors. Volante, Bottomline, Finastra, and FIS dominate the install base of large-bank payment hubs. Each has shipped ISO 20022-aware versions of its core product. Volante's pitch is on schema-aware integration and a low-code translation layer. Bottomline emphasizes its corporate-banking channels and pre-validation capabilities. Finastra leans on its breadth (payment hub plus core banking plus trade finance). FIS has the broadest North American install base, which matters because Fedwire's ISO 20022 cutover happened in 2025 as well.

For most large banks, the incumbent strategy is the path of least resistance. Replacing the payment hub during a migration is a higher-risk move than upgrading the existing one.

Cloud-native challengers. Modern Treasury, Form3, and a small group of newer entrants pitch greenfield deployments to second-wave banks (mid-tier and regional banks completing their migration in 2026 and 2027) and to non-bank financial institutions. Their pitch is cleaner data models, faster deployment, and lower long-run cost. Their disadvantage is that they have not yet been battle-tested at tier-one volumes.

The interesting cases are the banks bypassing the incumbents entirely for specific corridors. A bank that runs its legacy hub for general cross-border payments but uses a cloud-native vendor for a specific high-growth corridor (US to Mexico, UK to India, Singapore to Indonesia) is hedging the rebuild without committing to a full replacement.

This split mirrors the broader pattern of how cross-border payments are being rebuilt and reflects the same dynamics that shaped the SWIFT, SEPA, and UPI rail competition.

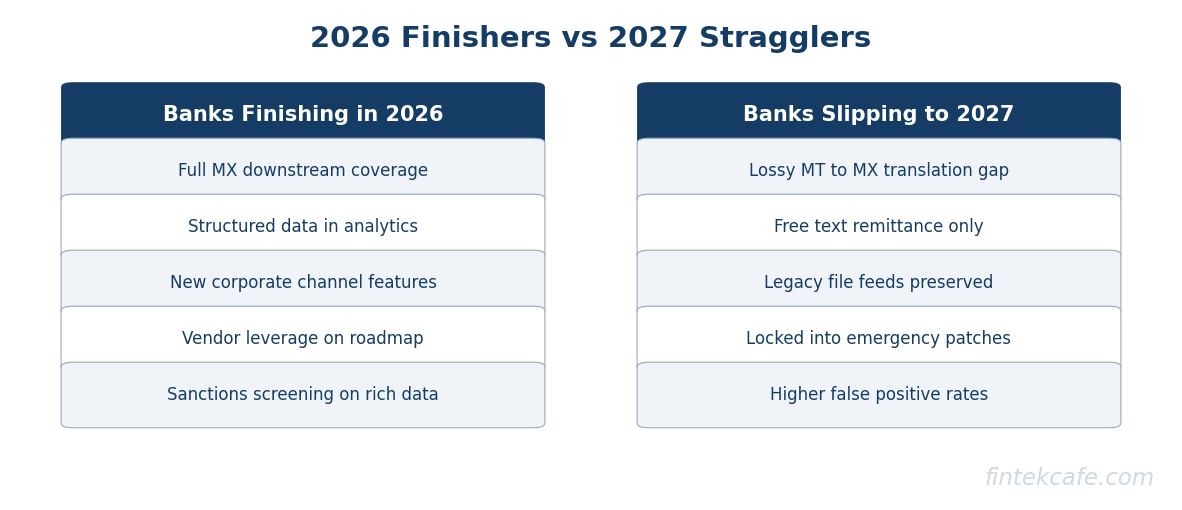

What 2026 Finishers Should Prioritize vs 2027 Stragglers

The deadline closed for SWIFT cross-border in November 2025. The downstream-systems deadline is whatever each bank sets for itself. Two patterns are emerging.

Banks Finishing the Downstream Work in 2026

These banks should be prioritizing the data-utilization upside. The messaging migration is sunk cost. The return on the migration comes from the downstream upgrades.

Specifically, the 2026 finishers should be:

- Upgrading sanctions screening to consume structured party identification and purpose codes. The false-positive reduction has a direct cost-takeout argument that pays for the work.

- Extending the AML feature store to capture structured remittance fields. The benefit is better models, lower investigation volume, and improved typology detection.

- Rebuilding the corporate-banking portal to surface structured remittance information. The benefit is corporate-customer retention.

- Building pre-validation services for high-corridor payments. The benefit is fewer returned payments and lower investigation cost.

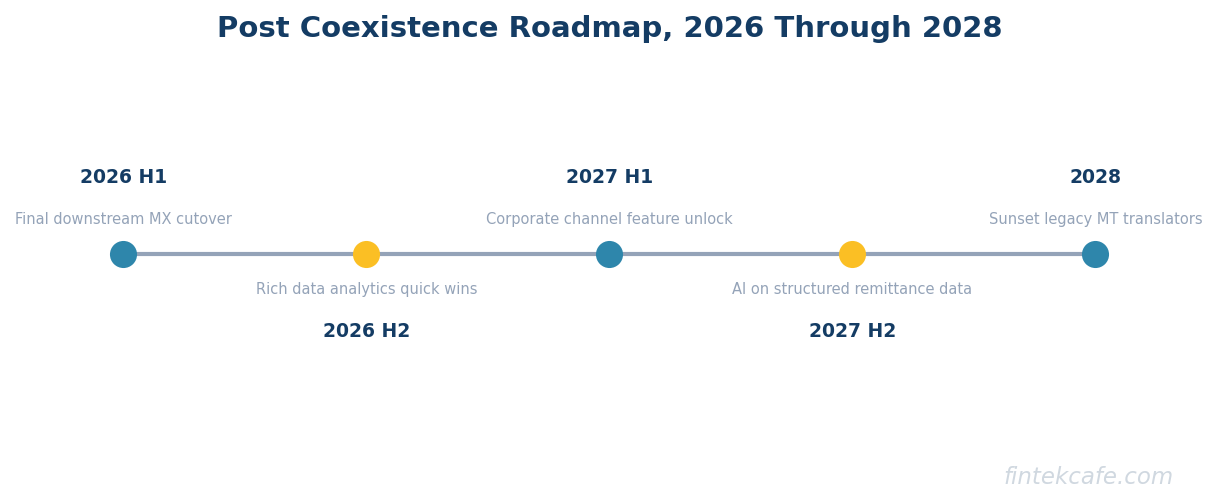

The bank that does this work in 2026 enters 2027 with a measurably better operating model. The bank that defers to 2027 spends 2026 paying the migration cost without earning the migration benefit.

Banks Finishing the Downstream Work in 2027

These banks (typically mid-tier, regional, or banks that started the migration late) should be prioritizing minimum viable compliance. The risk is taking on data-utilization scope before the foundational systems are upgraded.

The 2027 stragglers should be:

- Completing the payment-hub upgrade or replacement. This is the prerequisite for everything downstream.

- Ensuring sanctions screening and AML have at least basic ISO 20022 field consumption. Regulators will increasingly expect this.

- Deferring richer-data use cases (ML on remittance, advanced reconciliation automation) to 2028.

- Resisting the vendor pitch to do everything at once. A two-year sequenced plan beats a one-year overstretched plan.

The temptation for 2027 banks is to compare themselves to 2026 banks and try to catch up. That comparison is rarely the right operating frame. The 2026 banks made the investment earlier. The 2027 banks have the option to learn from their mistakes.

The Post-Coexistence Opportunities

The opportunities downstream of the migration are not a payments story. They are a data story.

Richer remittance data enables automated reconciliation. Corporate treasurers spend meaningful operations cost manually matching incoming payments against open invoices. Structured remittance information (invoice numbers, payment references, party identification) allows automated matching at much higher rates. The corporate bank that delivers this earns the treasury relationship.

ML on structured fields enables better screening and fraud detection. Models trained on free-form text are fundamentally limited. Models trained on structured purpose codes, structured party identifiers, and structured corridors have feature richness that did not exist before. The screening teams that retrain models on ISO 20022 fields will see false-positive rate reductions throughout 2026 and 2027.

Settlement instruction automation reduces operational risk. Pre-validation of account name against account number, supported by structured fields, reduces returned payments. Automated routing decisions based on structured corridor and purpose information reduce manual exception handling. Each of these wins is small individually. In aggregate they shift the cost base of the payments operation.

AI-augmented investigation reduces case-handling cost. AI applied to payment infrastructure is more effective on structured input than on unstructured text. The investigation analyst who reviews a payment with structured fields, supported by an AI summary, handles cases faster and with less context-switching.

The connecting principle is that ISO 20022 is a data-structure project that happens to be delivered through a messaging migration. The banks that internalize this will compound. The banks that treat the deadline as the project will spend the rest of the decade paying the migration cost without earning the migration benefit. A useful baseline for the underlying technology stack remains core banking systems and the migration economics they impose, and the broader framing of the standard sits in the ISO 20022 reference guide.

What This Means for Bank Executives in 2026

For the executive sponsor of payments transformation, the right question to ask the team is not whether the migration is complete. It is which of the four layers (gateway, hub, downstream analytics, customer channels) is complete, which is in flight, and which is still on the backlog. A migration that stops at the gateway is a half-finished migration. A migration that stops at the hub is a project that has paid for itself but has not yet earned its return.

The vendor decisions made in 2026 will shape the payments stack into the early 2030s. Choosing to upgrade with the incumbent is the lower-risk path. Choosing to rebuild with a cloud-native vendor is the higher-upside path. Choosing to delay is a third option that the deadline removed for the gateway but is still on the table for the downstream layers. The wrong move is to make all three choices at once because no single one has been thought through.

FAQ

Has the ISO 20022 migration deadline already passed?

For SWIFT cross-border payments, yes. The coexistence window closed in November 2025. MT messages for the cross-border categories are no longer accepted on the SWIFT network. Domestic real-time rails (TARGET2, CHAPS, Fedwire) also completed their cutovers in 2023 to 2025. The downstream-systems work inside banks continues through 2026 and 2027.

What is the difference between MT and MX message formats?

MT is the legacy SWIFT message format, structured around fixed-width fields with free-form text for most remittance information. MX is the ISO 20022 XML-based format with deeply structured fields for parties, accounts, purpose, remittance, and regulatory reporting. MX carries more data and carries it in a way that downstream systems can consume programmatically.

Why is the messaging-gateway upgrade not enough?

The gateway translates the message format. It does not change how the rest of the bank's systems process the data. If the payment hub, screening engine, AML pipeline, and reconciliation system are still built around legacy field structures, the gateway just translates the new format back to the old internal shape and discards the structure that ISO 20022 carries. The benefits of the migration are downstream of the gateway.

Which vendors dominate the ISO 20022 payment-hub market?

The incumbents are Volante, Bottomline, Finastra, and FIS. They cover the bulk of the large-bank install base and have shipped ISO 20022-aware versions of their core products. Cloud-native challengers (Modern Treasury, Form3) are growing share with mid-tier banks and non-bank financial institutions, particularly in greenfield deployments and specific corridors.

What is the biggest mistake banks are making with ISO 20022?

Treating the deadline as the project. The deadline was about messaging. The benefit is about data. Banks that completed the gateway cutover and assumed the migration was done are now discovering that the downstream systems still operate on the legacy data shape, which means the screening, AML, and reconciliation systems do not see the richer fields. The migration is a multi-year program. The deadline was the first milestone, not the last.

Related reading on FinTekCafe

- SWIFT vs SEPA vs UPI: Global Payment Networks Compared

- Real-Time Cross-Border Payments: SWIFT, Wise, Ripple in 2026

- What Is ISO 20022? The Executive Guide

- Core Banking Systems: The Technology That Runs Every Bank

- How AI Is Reshaping Payment Infrastructure

- How Cross-Border Payments Work and Why They Are So Slow

Related Articles

The Consortium Stablecoin: Why the Card Networks Are Funding Their Own Disruption

Visa, Mastercard, and Stripe are backing an open stablecoin consortium. The playbook is older than it looks: own the new rail's governance before it owns you.

Merchant of Record vs Payment Facilitator: Who Holds the Risk in Your Payment Stack

The four payment models compared: who holds tax, chargeback, and compliance liability as merchant of record, payfac, marketplace, or processor, and which fits.

Interchange Fees Explained: Who Really Pays for Card Payments

What interchange fees are, who pays whom in the four-party model, why rates vary, what regulation changed, and how merchants realistically cut card costs.