Embedded Finance in 2026: How Non-Banks Became Financial Companies

Key Takeaways

- Embedded finance is the integration of financial products, accounts, payments, lending, and cards, directly into the software of companies that are not banks. By 2026 it is a mainstream distribution model, not an experiment, and the brands embedding it span vertical software, marketplaces, and retailers.

- The stack has four layers: the sponsor bank that holds the charter and the regulatory liability, the banking-as-a-service middleware that translates banking into APIs, the program manager that runs the day-to-day program, and the brand that owns the customer. Confusing these roles is the root cause of most failures.

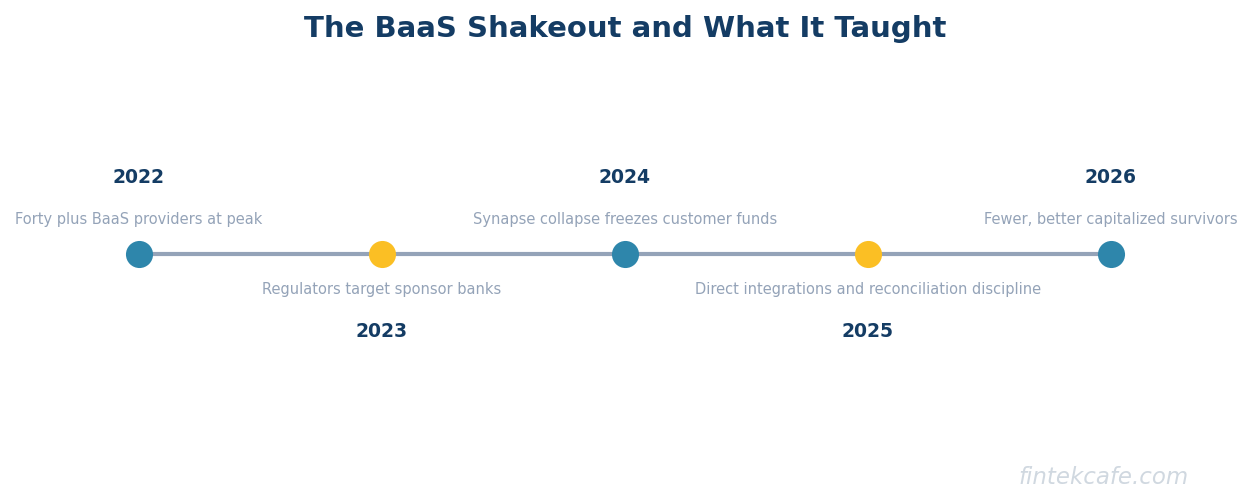

- The regulatory liability sits with the chartered sponsor bank, not the brand and not the middleware. The 2023 to 2025 shakeout happened when regulators made clear that banks own the compliance of every program they sponsor, and several middleware providers could not bridge the gap between fast software and slow banking compliance.

- The Synapse collapse in 2024 was the defining lesson: when the middleware layer fails, customer funds can be frozen because the ledgers reconciling who owns what live in the middleware, not the bank. The market response was direct bank integrations, reconciliation discipline, and fewer middlemen.

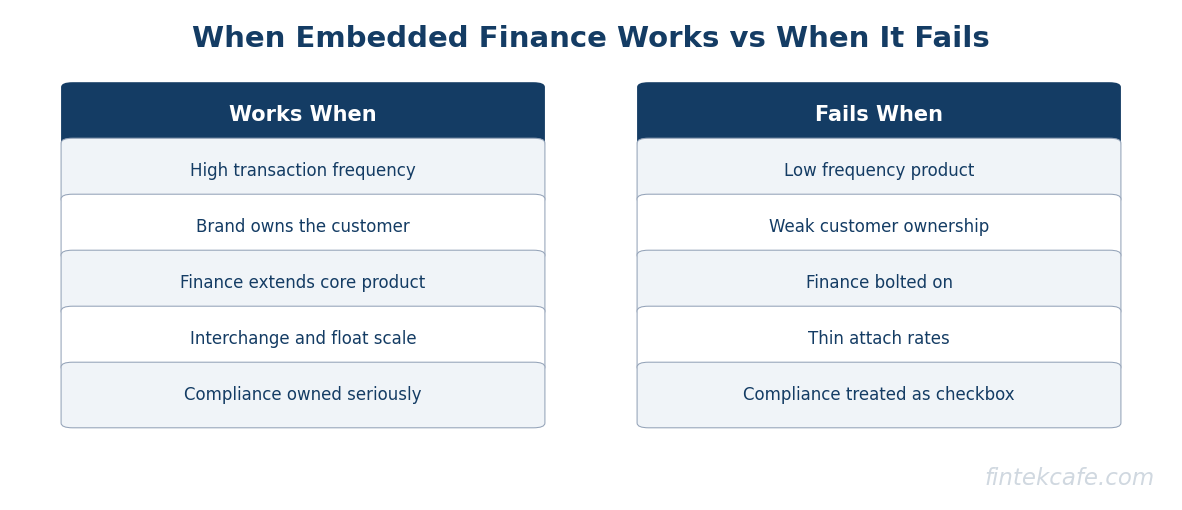

- The unit economics decide whether embedding finance is a margin engine or a distraction. It works when the brand has high-frequency transactions, owns the customer relationship, and can monetize through interchange, float, or lending spread. It fails when finance is bolted onto a low-frequency product with thin attach rates.

Software Companies Quietly Became Financial Companies

A decade ago, the companies that offered you a bank account, a debit card, a loan, or a payment service were banks and a handful of fintech startups trying to act like them. In 2026, the company offering you those products is just as likely to be your accounting software, your e-commerce platform, your rideshare app, or your favorite retailer. Finance has been absorbed into software, and the absorption is now the default for any platform with enough transaction volume to make it pay.

This is embedded finance: financial products delivered inside the experience of a company that is not, itself, a bank. The accounting platform that offers its small-business customers a checking account and a card. The marketplace that pays its sellers instantly and lends them working capital. The retailer with its own branded card and buy-now-pay-later at checkout. None of these companies hold a banking charter. All of them offer banking products. The layer that makes this possible, banking-as-a-service, sits underneath, invisible to the end customer and increasingly consequential to whether the whole arrangement is a profit center or a liability.

The story of embedded finance in 2026 is not the story of its rise, which is settled, but the story of its maturation. The model went through a hard shakeout between 2023 and 2025 that separated the durable from the fragile, killed several prominent middleware providers, and taught the market expensive lessons about where regulatory liability actually lives. This guide explains the stack, names who holds the risk, reconstructs why the middleware layer cracked and what it taught, and lays out the unit economics that determine whether a given company should embed finance at all. For the foundational version of the concept, the explainer on why every company wants to be a bank is the companion to this more advanced treatment.

The Embedded Finance Stack

The single most important thing to understand about embedded finance is that it is a stack of distinct parties with distinct roles and distinct liabilities. The end customer sees one brand. Behind that brand are three more layers, and the confusion of these roles is the source of nearly every failure in the category.

The Sponsor Bank

At the bottom sits a chartered bank. It holds the banking license, the relationship with the payment networks, and, critically, the regulatory liability for everything that happens in the programs it sponsors. The customer's deposits sit at this bank and are insured through it. When a regulator has a concern about an embedded finance program, it goes to the sponsor bank, because the charter is what is being regulated. The sponsor bank is usually a smaller community or regional bank for which sponsoring programs is a meaningful revenue line.

The Banking-as-a-Service Middleware

Banking-as-a-service middleware is the technology layer that translates a bank's regulated capabilities into developer-friendly APIs. A modern software company cannot integrate directly with a community bank's decades-old core banking system and slow processes. The middleware sits in between, exposing clean APIs for opening accounts, issuing cards, moving money, and running compliance checks, while handling the integration with the bank's core on the other side. This layer is what made embedded finance scalable, and it is also the layer that cracked in the shakeout. The mechanics of this translation layer are covered in depth in the guide to how banking-as-a-service lets companies become banks overnight.

The Program Manager

Someone has to run the program day to day: monitor for fraud and money laundering, handle customer disputes, manage the compliance obligations the sponsor bank delegates, and keep the books reconciled. This is the program manager role. Sometimes the brand performs it, sometimes the middleware provider does, sometimes a specialist third party does. The shakeout revealed that ambiguity about who is actually doing this work, and whether they are doing it well, is a direct path to regulatory trouble.

The Brand

At the top is the company the customer actually sees: the software platform, marketplace, or retailer whose name is on the card and in the app. The brand owns the customer relationship, the user experience, and the distribution. What it does not own, and what many brands wrongly assumed they could outsource entirely, is the compliance responsibility, because the regulator holds the bank accountable and the bank, in turn, holds the brand accountable through their contract.

Who Actually Holds the Liability

The defining hard truth of embedded finance is this: the regulatory liability lives with the chartered sponsor bank, and it cannot be contracted away. A brand can delegate operations to a middleware provider and a program manager, but if a program launders money, mistreats customers, or mismanages funds, the regulator holds the sponsor bank responsible. The bank then holds the brand and middleware responsible through their agreements. Liability flows down by contract, but it originates and ultimately rests at the charter.

This is exactly what the 2023 to 2025 period made unavoidably clear. Regulators issued a series of consent orders and enforcement actions against sponsor banks for failures in the embedded programs they hosted, sending an unmistakable signal: a bank owns the compliance of every program it sponsors, full stop. The era when a bank could rent out its charter, collect a fee, and look away was over. Banks responded by demanding far more oversight, far more compliance investment, and far higher standards from the middleware and brands they worked with, and by exiting relationships they could not adequately supervise.

The practical consequence for any company considering embedded finance is that the regulatory burden is real and shared, not outsourced. The brand inherits compliance obligations through its bank relationship. The diligence questions, who is the sponsor bank, how strong is its compliance program, who actually runs the program management, and where do the customer funds and ledgers live, are not legal fine print. They are the difference between a stable program and the next casualty. This dynamic connects directly to the broader regulatory shift in US open banking under Section 1033 of the CFPB rule, which is reshaping who controls financial data and access.

The Shakeout: What the Middleware Collapses Taught

The middleware layer was the innovation that scaled embedded finance, and it was also the layer that proved most fragile. Between 2023 and 2025, several prominent banking-as-a-service middleware providers collapsed, restructured, or were forced into fire sales. The most consequential was the failure of Synapse in 2024, which became the cautionary tale the entire industry now references.

The Synapse collapse mattered because of what it revealed about where the risk actually concentrated. When the middleware provider failed, end customers of the brands it served found their funds frozen, in some cases for extended periods, because the records reconciling who owned how much, the ledgers tracking funds across the brands and the underlying banks, lived in the middleware layer, not cleanly in the banks. When the middleware went down, the map of who owned what went with it. Customers who believed their money sat safely in an insured bank account discovered that the path between them and that account ran through a private company that had just failed.

The lessons the market absorbed were direct and they reshaped the architecture of the category:

- Reconciliation discipline is existential. The ledgers that track customer funds must be accurate, continuously reconciled, and ideally held in a way that survives the failure of any single intermediary. Fuzzy reconciliation is not a back-office detail. It is a customer-funds risk.

- Fewer middlemen, more direct integration. Brands with the scale to do so moved toward direct relationships with sponsor banks, cutting out or reducing reliance on the middleware layer, to shorten the chain between the customer and the insured deposit.

- Compliance cannot move at software speed alone. The collapses happened in part because some middleware providers grew faster than their compliance and risk functions could support. Banking compliance is slow for reasons, and the providers that survived were the ones that respected that rather than treating it as friction to be engineered away.

- Consolidation was inevitable. The category emerged from the shakeout smaller, more concentrated, better capitalized, and more closely supervised. The survivors are the providers that combined real banking-grade compliance with genuine software capability, and there are fewer of them.

The shakeout did not kill embedded finance. It killed the version of embedded finance that treated banking as a pure software problem and compliance as an afterthought. What remains is a more sober, more durable, and more bank-aligned version of the model. The same pattern of partnership friction and consolidation is visible across the sector, as the analysis of how fintech partnerships actually work details.

The Unit Economics That Decide It

For an executive, the strategic question is not whether embedded finance is possible. It is. The question is whether it is a margin engine or a distraction for a specific company. The answer lives in the unit economics, and they are unforgiving.

Embedded finance generates revenue through a handful of channels: interchange, the fee earned every time the embedded card is used; float, the yield earned on customer balances held in the program; lending spread, the margin on credit extended to customers; and transaction or subscription fees on the financial features themselves. Against this revenue sits a real cost stack: the share paid to the sponsor bank and middleware, the compliance and program-management overhead, fraud and credit losses, and the engineering cost of building and maintaining the integration.

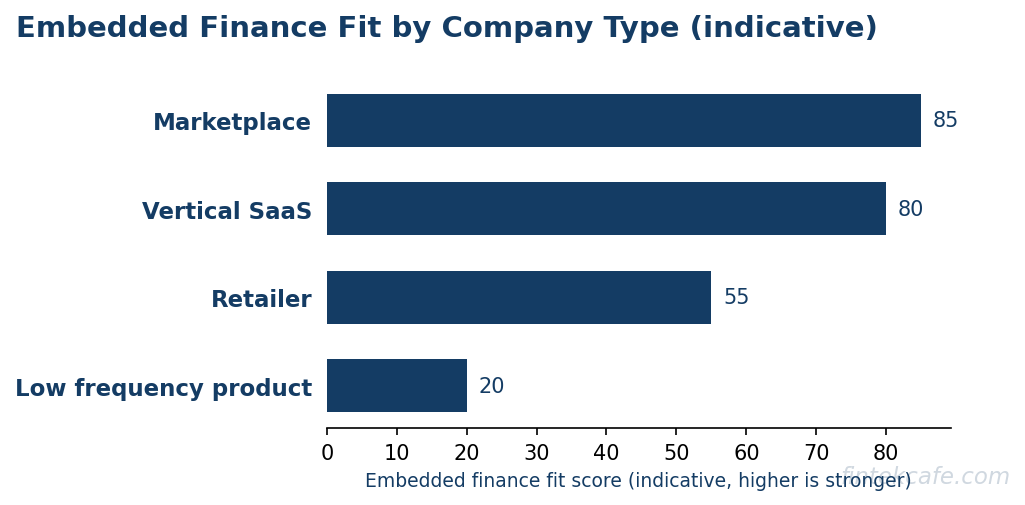

The arithmetic works when three conditions hold. First, the brand has high transaction frequency, because interchange and float scale with volume and a low-frequency product cannot generate enough of either to cover the fixed compliance overhead. Second, the brand genuinely owns the customer relationship, so attach rates for the financial product are high rather than the single-digit percentages that doom a bolt-on. Third, the financial product is a natural extension of the core product, so it deepens engagement rather than diluting focus. A marketplace paying sellers, a vertical software platform managing its customers' money flows, a retailer with a loyal high-frequency base: these have the shape.

The arithmetic fails when finance is bolted onto a product with low frequency, weak customer ownership, or no natural connection to money movement. In those cases the compliance overhead is fixed and heavy, the attach rate is thin, and the revenue never covers the cost. The financial feature becomes a distraction that consumes engineering and compliance attention for negligible margin. The discipline of evaluating attach rates, lifetime value, and acquisition cost before committing is the same discipline laid out in the breakdown of the unit economics of fintech.

A Decision Framework by Company Type

The right embedded finance strategy depends on the shape of the underlying business. Three archetypes capture most cases.

| Company type | Embedded finance fit | The play | The trap |

|---|---|---|---|

| Marketplace | Strong | Instant payouts and working-capital lending to sellers; finance deepens the core liquidity loop | Underestimating credit risk and fraud on the lending side |

| Vertical SaaS | Strong | Accounts, cards, and payments embedded where the software already manages money flows | Treating finance as a feature checkbox rather than a real program with compliance ownership |

| Retailer | Mixed | Branded card and pay-later at checkout for a loyal, high-frequency base | Low attach and thin frequency turning the program into fixed-cost overhead |

Marketplaces have the strongest natural fit because money already flows through them and embedding finance deepens the existing loop. Vertical software platforms are close behind when the software already sits on top of the customer's money movement, accounting, payroll, invoicing, because the financial product is a short step from what they already do. Retailers are the most mixed: a loyal, high-frequency base can make a branded card and pay-later pay, but a low-frequency or low-loyalty base turns the program into expensive overhead with thin returns.

The through-line for every archetype is the same. Embedded finance is not a feature you add. It is a regulated financial program you take on, with real liability flowing from a sponsor bank, real compliance overhead, and unit economics that only work at sufficient frequency and attach. The companies that succeed treat it with the seriousness that banking demands. The companies that struggle treat it as a product checkbox and discover, usually after a compliance scare or a reconciliation crisis, that there is no such thing as a casual financial company. The closely related shift in how consumer credit is reported, covered in the analysis of the BNPL credit-bureau reporting change, is one more reminder that embedding finance means inheriting the obligations of finance, not just its revenue.

FAQ

What is embedded finance in simple terms?

Embedded finance is when a company that is not a bank offers financial products, accounts, payments, lending, or cards, directly inside its own software or app. Your accounting platform offering a business checking account, a marketplace paying sellers instantly, or a retailer with its own branded card are all embedded finance. The company owns the customer experience, while a chartered bank holds the license and the regulatory liability underneath.

What is the difference between embedded finance and banking-as-a-service?

Embedded finance is the customer-facing outcome: financial products built into a non-bank's product. Banking-as-a-service is the infrastructure layer that makes it possible, the middleware that translates a chartered bank's regulated capabilities into APIs a software company can use. Embedded finance is what the customer sees. Banking-as-a-service is the plumbing underneath that connects the brand to the sponsor bank.

Who is legally responsible if an embedded finance program fails?

The chartered sponsor bank holds the regulatory liability and cannot contract it away. Regulators hold the bank accountable for the compliance of every program it sponsors, and the bank in turn holds the brand and middleware accountable through their agreements. This is the central lesson of the 2023 to 2025 enforcement wave: liability originates at the charter and flows down, so the diligence question of which bank sponsors a program, and how strong its compliance is, matters enormously.

Why did banking-as-a-service providers like Synapse collapse?

The middleware providers that failed grew faster than their compliance, risk, and reconciliation functions could support, and they sat in the critical path between customers and their insured deposits. When Synapse failed in 2024, customer funds were frozen because the ledgers reconciling who owned what lived in the middleware rather than cleanly in the banks. The market responded with stricter reconciliation, more direct bank integrations, and consolidation around better-capitalized, compliance-serious providers.

When does embedded finance actually make money for a company?

It makes money when the brand has high transaction frequency, genuinely owns the customer relationship, and offers a financial product that is a natural extension of the core business. Revenue comes from interchange, float on balances, and lending spread, all of which scale with volume and attach rate. It fails when finance is bolted onto a low-frequency product with thin attach, because the fixed compliance overhead then exceeds the revenue. Frequency and attach rate decide it.

Related reading on FinTekCafe

- Banking as a Service: How Fintech Companies Become Banks Overnight

- Embedded Finance Explained: Why Every Company Wants to Be a Bank

- How Fintech Partnerships Actually Work: Banks, BaaS, and Distribution

- Open Banking in the US: Section 1033 and the CFPB Rule

- The BNPL Credit-Bureau Reporting Shift

- What Is FedNow? The US Real-Time Payments Rail

- The Unit Economics of Fintech: CAC, LTV, and Why Most Startups Lose Money

Related Articles

The Consortium Stablecoin: Why the Card Networks Are Funding Their Own Disruption

Visa, Mastercard, and Stripe are backing an open stablecoin consortium. The playbook is older than it looks: own the new rail's governance before it owns you.

Merchant of Record vs Payment Facilitator: Who Holds the Risk in Your Payment Stack

The four payment models compared: who holds tax, chargeback, and compliance liability as merchant of record, payfac, marketplace, or processor, and which fits.

Interchange Fees Explained: Who Really Pays for Card Payments

What interchange fees are, who pays whom in the four-party model, why rates vary, what regulation changed, and how merchants realistically cut card costs.