Interchange Fees Explained: Who Really Pays for Card Payments

Interchange is the per-transaction fee that the merchant's bank pays to the cardholder's bank on every card payment, and the merchant ultimately funds it: typically around 1.5 to 2.5 percent of a US credit-card transaction and the dominant share of total card-acceptance cost. The networks set the rates but do not keep the money; the issuing banks collect it, and it funds the rewards points, cash back, and zero-liability protections that make cardholders prefer cards in the first place. The sums are enormous: Nilson Report data puts US merchants' total card-processing fees above one hundred seventy billion USD a year, most of it interchange. Interchange is simultaneously the largest cost line in card acceptance, the engine of the rewards economy, the subject of two decades of litigation and regulation on three continents, and the line item executives most consistently misread on their own processing statements. This guide explains where the money goes, why the rates are what they are, and what a merchant can and cannot do about it.

Key Takeaways

- Interchange flows from the merchant's acquiring bank to the cardholder's issuing bank, set by the card networks, and passed through to the merchant. On a typical hundred-dollar US credit transaction, roughly two dollars to two dollars fifty leaves the merchant, and the issuer's interchange is the largest slice by far; network assessments and processor markup split the remainder.

- Rates vary widely by design: card type (a premium rewards card costs the merchant more than a basic one), merchant category, channel (card-present versus online), and region. The rate table is a pricing instrument the networks use to steer issuance and acceptance, not a cost-recovery formula.

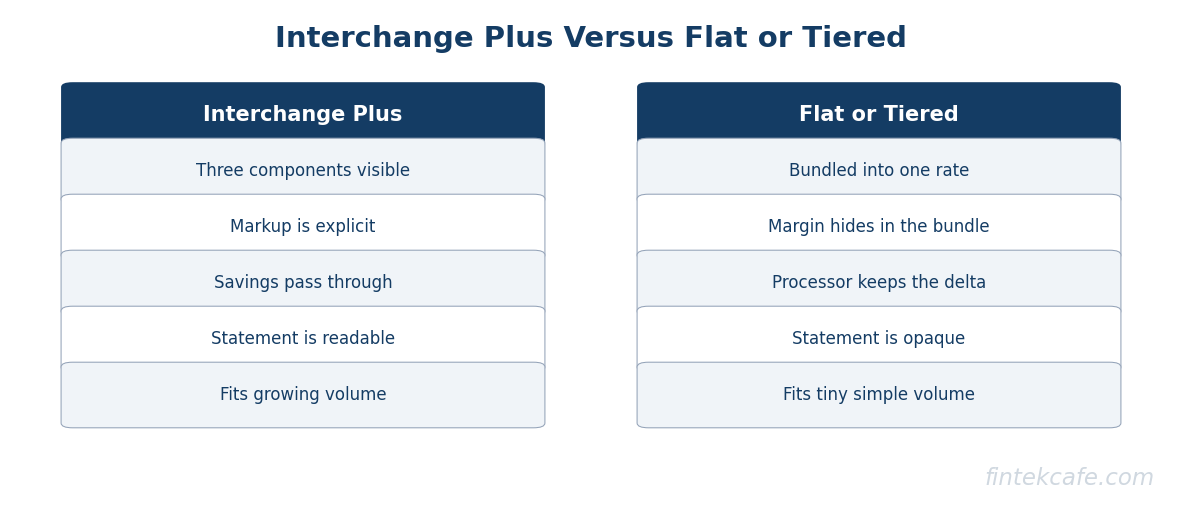

- The three components of card cost, interchange, network assessments, and processor markup, are only visible under interchange-plus pricing. Flat-rate and tiered pricing bundle them, and the bundle is where processors bury margin. Reading a statement starts with knowing which pricing model it is written in.

- Regulation reshaped interchange where it landed: the US Durbin amendment capped regulated debit at a fraction of its former level, and EU caps cut credit interchange to 0.3 percent and debit to 0.2 percent. Where caps landed, issuer rewards economics shrank with them; the pending US credit-routing fight is the next front.

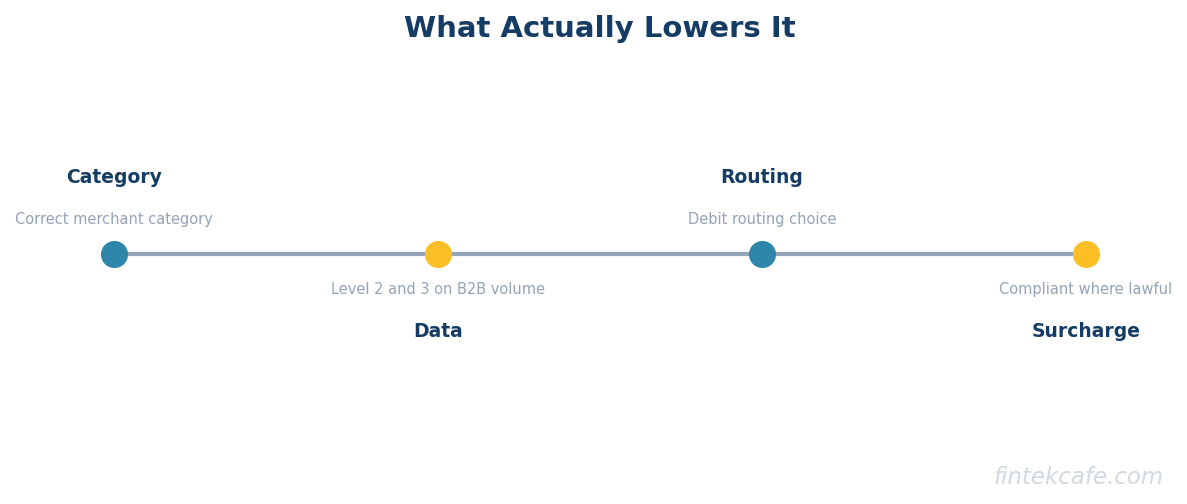

- Merchants reduce interchange with unglamorous mechanics, correct merchant category, level 2/3 data on B2B volume, debit-routing choice, and compliant surcharging where lawful, worth tens of basis points each in the right circumstances. The tactics that promise to make interchange disappear generally do not survive contact with network rules.

The Four-Party Model: Who Pays Whom, in Order

Every card transaction involves four parties beyond the network: the cardholder, the issuing bank that gave them the card, the merchant, and the acquiring bank (in practice fronted by a processor) that accepts cards on the merchant's behalf. The network, Visa or Mastercard in the standard model, sits in the middle, routing messages and setting rules; the mechanics of that message flow are covered in how Visa processes a transaction, and the division of labor between the merchant-side players in payment gateway versus payment processor.

The money flow is best followed through a concrete example, written in words because the order matters more than the cents. A customer pays one hundred dollars at an online retailer with a mid-tier US rewards credit card:

| Step | Who pays whom | Amount on a hundred-dollar sale |

|---|---|---|

| 1. Purchase | Cardholder's issuer commits to pay; cardholder owes their issuer | One hundred dollars |

| 2. Interchange deducted | Acquirer pays issuer the transaction amount minus interchange | Issuer keeps roughly one dollar eighty (about 1.8 percent for a rewards card online) |

| 3. Network assessments | Both banks pay the network its fees | Roughly fourteen cents (about 0.13 to 0.14 percent, plus small per-item fees) |

| 4. Processor markup | Acquirer/processor takes its margin | Roughly twenty to fifty cents for a mid-sized merchant on interchange-plus; more on flat-rate |

| 5. Merchant settles | Merchant receives the remainder | Roughly ninety seven dollars and change |

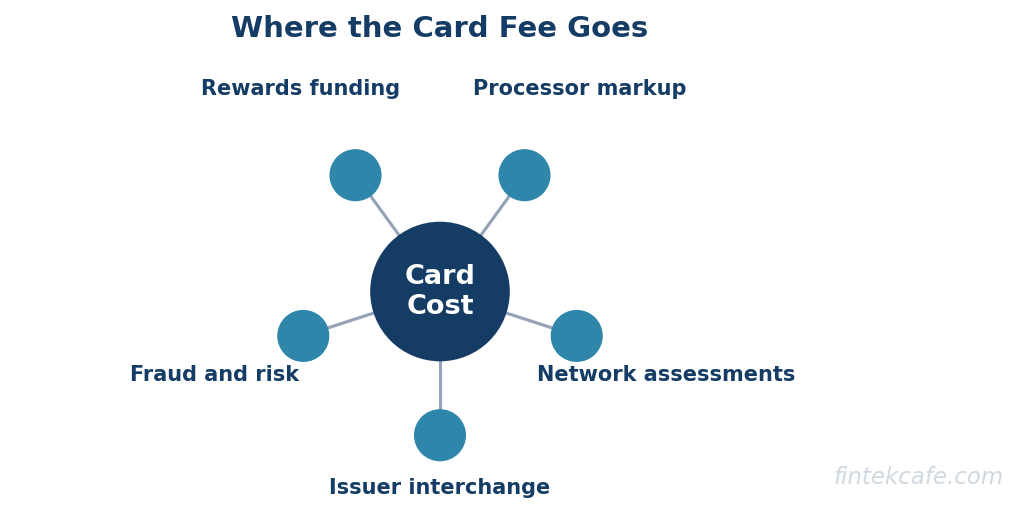

Two things about this flow surprise executives. First, the network's own take, the assessments, is the smallest slice on the table; the network's business is scale, not rate. Second, interchange is not revenue for anyone the merchant deals with: the acquirer and processor pass it through to the issuer, which is why a processor cannot negotiate interchange down, only its own markup. The issuer uses that interchange to fund rewards, float, fraud losses, and zero-liability guarantees, which completes the economic circle: interchange is the mechanism by which merchants collectively fund the incentives that keep customers paying with cards. That is neither scandal nor accident; it is the design, and it is why interchange politics never resolve, because the fee that is a cost to merchants is the product to issuers.

Why Rates Vary So Widely

There is no single interchange rate; the US networks each publish schedules with hundreds of categories, and the variation is deliberate. Four dimensions drive it.

Card type. Premium rewards and commercial cards carry materially higher interchange than basic consumer cards, often a half to a full percentage point more, because richer interchange funds richer rewards, which attracts the high-spending cardholders issuers compete for. The merchant, who cannot refuse a specific card tier within a brand they accept under network honor-all-cards rules, funds the arms race.

Merchant category. Interchange varies by merchant category code (MCC). Categories the networks want to penetrate, historically supermarkets, utilities, and government payments, get concessionary rates; travel and e-commerce sit higher. The MCC is assigned at onboarding, and a misassigned code quietly reprices every transaction a business processes.

Channel and risk. Card-present transactions, where the chip is read, carry lower rates than card-not-present, reflecting fraud risk; within e-commerce, transactions with stronger authentication and richer data qualify for better categories. Every downgrade, a transaction that fails to meet the data requirements of its best available category, reprices that transaction upward, and downgrades are pure waste: cost without any offsetting value.

Region. Interchange is set per market, and regulation has fractured the map: an identical transaction that carries 1.8 percent in the US carries 0.3 percent in the EU, which is the cleanest available evidence that rates reflect what markets and regulators will bear rather than underlying cost.

Interchange, Assessments, and Markup: Reading Your Statement

Total card cost has exactly three components, and a merchant's leverage differs completely across them. Interchange goes to the issuer, is set by the networks, and is non-negotiable; the play is qualifying for better categories. Assessments go to the networks, are small, uniform, and effectively fixed. Processor markup goes to the acquirer/processor, and it is the only fully negotiable component.

Whether a merchant can see these three lines depends on the pricing model. Under interchange-plus pricing, the statement shows actual interchange plus a stated markup, and every category and downgrade is visible. Under flat-rate pricing, one blended percentage covers everything, simple, predictable, and opaque; the flat rate is set high enough to cover the worst card mix, so merchants with favorable mixes systematically overpay for the simplicity. Under tiered pricing, transactions land in "qualified," "mid-qualified," and "non-qualified" buckets defined by the processor, an arrangement with the transparency of neither and the margin opportunities of both.

The executive guidance is uncomplicated: at meaningful volume, interchange-plus is the only pricing under which a statement can be audited, and moving to it is frequently worth more than any subsequent optimization, because it converts an unexaminable blend into a line-item negotiation. Flat-rate remains rational for small or low-volume merchants who are buying simplicity, which is precisely what it charges for.

The Regulatory Battles

Interchange has been litigated and regulated for two decades because of the structural quirk at its center: the fee is set by networks, collected by issuers, and paid by merchants who are not party to the setting. Three fronts matter.

Durbin and US debit. The 2010 Durbin amendment capped debit interchange for banks above ten billion USD in assets at twenty one cents plus 0.05 percent (plus a small fraud adjustment), a fraction of prior levels, and its Regulation II routing rules require every debit card to support at least two unaffiliated networks, with the Federal Reserve clarifying in 2022 that this applies to online transactions as well. The observable aftermath: debit rewards programs largely disappeared, free-checking economics tightened, and a routing market emerged in which merchants can steer debit to cheaper networks.

The EU caps. The EU's Interchange Fee Regulation capped consumer card interchange at 0.3 percent for credit and 0.2 percent for debit from 2015. Merchant costs fell; rewards programs in capped markets thinned to near-vestigial levels compared with the US. The EU experience is the reference case both sides cite: proof that caps lower merchant costs, and proof that cardholders fund the difference through diminished perks, depending on who is presenting.

The pending US credit fight. The proposed Credit Card Competition Act would extend routing-style competition to credit, requiring large issuers to enable a second network on each card, on the theory that network competition for merchant routing would compress effective rates. Issuers and networks argue it would defund rewards and card benefits, as caps did elsewhere. As of mid-2026 the legislation remains proposed rather than enacted, and separately, the long-running merchant litigation against the networks continues to produce settlement proposals around modest rate relief and expanded surcharging freedom. The direction of travel across all three fronts is consistent: more routing choice, more merchant steering rights, slow compression of the most protected rates.

What Actually Reduces Interchange, and What Does Not

Merchant-side interchange optimization is real but bounded: it is a game of basis points, played through data quality and routing, and the realistic tactics fit in one table.

| Tactic | What it is | Realistic impact | The catch |

|---|---|---|---|

| Correct MCC | Verifying the merchant category code matches the actual business | Can be worth tens of basis points if miscoded | One-time fix; deliberately gaming the code violates network rules |

| Level 2/3 data | Submitting enhanced transaction data (tax, invoice, line items) on commercial cards | Half a point or more on qualifying B2B volume | Only applies to commercial/purchasing cards; requires integration work |

| Avoiding downgrades | Settling on time, passing required fields (AVS, auth data) so transactions qualify for their best category | Tens of basis points of pure waste recovered | Requires statement-level visibility, hence interchange-plus pricing |

| Debit routing | Steering debit transactions to the cheaper of the two required networks | Meaningful on debit-heavy volume | US debit only; needs a processor that exposes routing choice |

| Surcharging / cash discount | Passing card cost to the card-paying customer where lawful | Shifts the cost rather than reducing it | Capped and rule-bound by networks, banned or restricted in several US states and by law in some countries; compliance failures are expensive |

| Payment orchestration | Routing across multiple acquirers for cost and approval optimization | Varies; strongest for cross-border volume | Adds infrastructure; the economics are covered in the orchestration guide |

Larger merchants add two structural plays: negotiating processor markup at contract renewal, which is always available and always worth doing, and, at the very top of the market, negotiating directly with networks for strategic-merchant incentive agreements, which is available to roughly nobody else. Routing infrastructure that arbitrates across processors, covered in payment orchestration and multi-processor routing, is the industrial version of the same instinct.

The non-tactics deserve equal clarity. No processor can discount interchange itself; a pitch claiming otherwise is repackaging the markup. Tiered-pricing "savings" that are not expressed against actual interchange are arithmetic theater. And cost reduction that damages authorization rates or invites disputes is negative-sum: a declined sale costs the margin, not the fee, and the dispute system carries its own fee schedule and thresholds, as covered in how chargebacks and the dispute system work.

Where Interchange Goes From Here

The strategic question for the next decade is not whether interchange rates move by basis points but whether transactions leave the interchange system entirely. Account-to-account payments, examined in how pay-by-bank works and what it threatens, settle directly between bank accounts over real-time rails with no interchange at all, and have reached mainstream scale in markets like Brazil and India; stablecoin settlement pilots aim at the same cost line from a different direction. The US and EU incumbency case rests on what interchange funds: rewards that steer consumer preference, dispute rights, and fraud guarantees that alternative rails mostly lack. The realistic near-term trajectory, visible in markets where alternatives scaled, is not replacement but segmentation: low-margin, high-trust, repeat payments (bills, B2B, government) migrate to cheaper rails first, while rewarded consumer discretionary spend stays on cards longest, because the cardholder is paid to keep it there. For a merchant, that means interchange strategy and alternative-rail strategy are becoming the same strategy: qualify existing card volume correctly, and build steering capability for the flows where customers will follow a cheaper rail.

FAQ

What is an interchange fee and who receives it?

Interchange is a per-transaction fee, set by the card networks, that the merchant's acquiring bank pays to the cardholder's issuing bank; the acquirer passes the cost through to the merchant. On US credit cards it typically runs around 1.5 to 2.5 percent of the transaction. The issuing bank uses interchange revenue to fund rewards programs, fraud protection, and cardholder benefits, which is why the fee is a cost line to merchants and a revenue line to banks.

What is the difference between interchange and processing fees?

Total card-acceptance cost has three parts: interchange, which goes to the issuing bank; network assessments, a smaller fee that goes to Visa or Mastercard; and processor markup, which goes to the merchant's processor. Only the markup is negotiable with the processor. "Processing fees" on a merchant statement usually bundle all three; interchange-plus pricing is the model that shows them separately.

What is interchange-plus pricing and why does it matter?

Interchange-plus pricing bills the merchant the actual interchange for each transaction plus a stated processor markup, making all three cost components visible and auditable. Flat-rate and tiered pricing blend them into one number that hides where the money goes, and the blend is priced for the processor's benefit. At meaningful volume, moving to interchange-plus is typically the highest-value single change a merchant can make to card costs, because it turns a blended rate into a negotiable line item.

Can merchants reduce interchange fees?

Within the card system, merchants reduce interchange by qualifying transactions for better rate categories rather than by negotiation: correct merchant category coding, level 2/3 data on commercial cards, avoiding downgrades through complete data and timely settlement, and routing US debit to the cheaper available network. Each tactic is worth tens of basis points to half a point in the right circumstances. No processor can discount interchange itself, so offers to do so are repriced markup.

Do interchange caps help consumers?

The evidence from capped markets cuts both ways. EU caps of 0.3 percent on credit and 0.2 percent on debit, and the US Durbin cap on debit, measurably lowered merchant costs, and merchants in competitive sectors passed some of that through in prices. Issuers, in turn, cut what interchange had funded: debit rewards effectively disappeared in the US and credit-card perks thinned in capped markets. Caps mainly relocate the cost of card benefits from merchants to cardholders, which is precisely why the policy fight never settles.

Related reading on FinTekCafe

Related Articles

The Consortium Stablecoin: Why the Card Networks Are Funding Their Own Disruption

Visa, Mastercard, and Stripe are backing an open stablecoin consortium. The playbook is older than it looks: own the new rail's governance before it owns you.

Merchant of Record vs Payment Facilitator: Who Holds the Risk in Your Payment Stack

The four payment models compared: who holds tax, chargeback, and compliance liability as merchant of record, payfac, marketplace, or processor, and which fits.

BNPL Grew Up: How Buy Now Pay Later Became a Balance Sheet Business

BNPL quietly became a balance sheet business. Who funds the receivables, who eats the credit cycle, and where the margin survives as banks move in.