Real-Time Cross-Border Payments: SWIFT GPI, Wise, Ripple, and the New Settlement Networks

A cross-border payment that took five business days in 2015 now settles in under a minute on most major corridors in 2026. The headline number that matters: the SWIFT gpi network reports that more than half of all cross-border payments on its rails reach the beneficiary bank within thirty minutes, and ninety percent settle within twenty-four hours. The same corridors served by Wise, RippleNet, Stripe Treasury, Airwallex, and stablecoin rails like USDC frequently settle in seconds at lower cost. Cross-border payment is no longer a single-rail business and treasurers buying it are no longer choosing between fast and cheap.

This article walks through how each settlement layer actually works, where each beats the others, the corridor-by-corridor cost and speed reality in 2026, and the decision framework a treasurer or CFO can use to pick the right provider per corridor rather than per program.

What "Cross-Border Real-Time" Actually Means

Cross-border real-time is shorthand for an end-to-end payment experience in which the beneficiary receives usable funds within seconds to minutes of the sender's instruction, the foreign-exchange rate is locked at initiation, and the total cost is disclosed up front. Three layers determine whether a corridor delivers that experience.

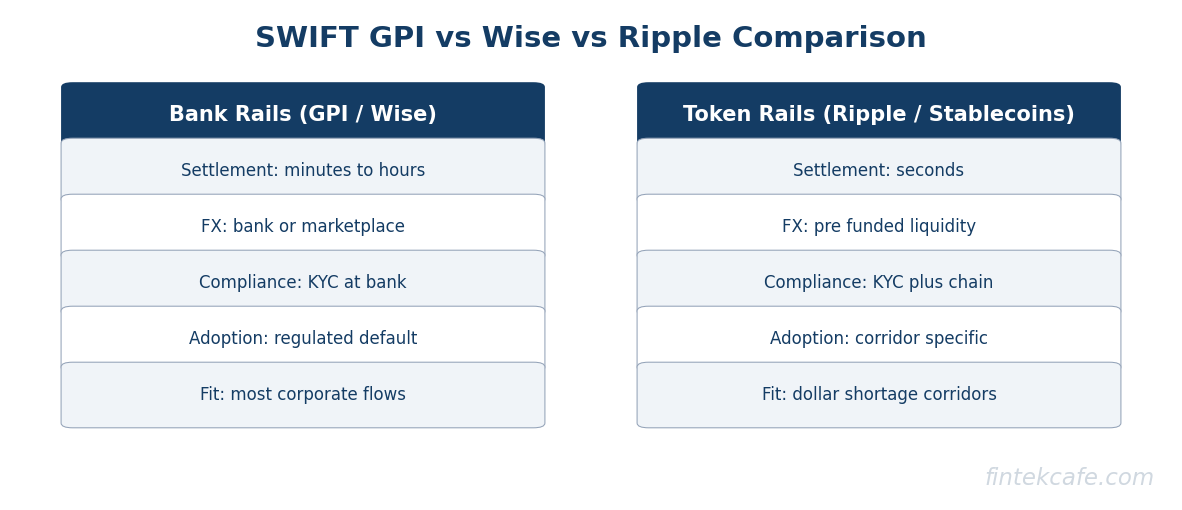

The messaging layer carries the payment instruction from one bank to another. SWIFT's MT and MX (ISO 20022) messages still dominate this layer for traditional bank-to-bank flows. The messaging layer is not the slow part anymore; SWIFT gpi instructions travel in seconds.

The settlement layer moves actual value between the two banks' accounts. Settlement is what historically took two to five days. Pre-funded liquidity on RippleNet, instant settlement on stablecoin rails, and same-day netting on SWIFT gpi have collectively compressed this from days to minutes for the corridors that have the operational infrastructure.

The foreign-exchange layer converts source currency to destination currency. The opacity that hides most of the cost lives here. A payment that looks "free" because the wire fee is waived often loses two to four percent inside the FX spread.

A corridor is "real-time" when all three layers run fast enough end-to-end. The 2026 reality is that the messaging and settlement layers are real-time across most major corridors; the FX layer is fast but not always cheap, and that is where the provider choice matters most.

How SWIFT GPI Compressed the Correspondent Model

SWIFT introduced gpi (Global Payments Innovation) in 2017 to solve the visible problems with correspondent banking: payments getting lost, no end-to-end tracking, and unpredictable fees. The gpi service rule set requires participating banks to credit the beneficiary same-day, deliver an unmodified remittance information field through the entire chain, and provide tracking through a unique end-to-end transaction reference (UETR).

What changed operationally:

Tracking. Every gpi payment has a UETR that follows it from origination to credit. Treasurers can now confirm landing in minutes rather than calling correspondent banks to ask where the money is.

Same-day credit. The gpi service-level commits participating banks to credit the beneficiary on the same business day, which is what reduces the multi-day tail that defined the legacy SWIFT experience.

Transparency. Sender banks see the deduction schedule from each correspondent bank in the chain at initiation, not after the fact. The "lifting fee" that used to disappear into a middle-bank's spread is now visible.

No new settlement layer. Gpi did not replace correspondent banking. It tightened the operational discipline on top of the existing rail. Settlement still moves through nostro accounts; the speed-up is in operational compliance, not in the underlying ledger.

The result, by SWIFT's published data: as of late 2025, more than half of gpi payments reach the beneficiary bank in thirty minutes, and the median end-to-end credit time is under one hour on major corridors. The full corridor latency includes the beneficiary bank's own crediting practice, which can add a few hours even after the gpi payment lands.

The ISO 20022 migration that hit its main milestone in November 2025 deepens this story. SWIFT MX messages carry structured purpose codes, structured remittance information, and legal entity identifiers that the legacy MT format could not. Banks that ingest the structured data into their fraud and reconciliation systems clear payments faster and reject fewer in pending queues. We covered the standard, the cutover, and the readiness checklist in our executive guide to ISO 20022.

How Wise's Mid-Market FX Model Beats Banks on Cost

Wise (the rebranded TransferWise) built a business on a single observation: most retail cross-border payments do not need to actually leave the country. A USD-to-EUR transfer through Wise typically pairs a USD inbound from a sender against a EUR outbound to a different beneficiary, settling both legs domestically in their respective rails and keeping the net imbalance on Wise's own books. The result is a payment that never traverses correspondent banking and never pays the cumulative spread that correspondent banking imposes.

What Wise actually delivers:

Mid-market FX with disclosed margin. Wise quotes the interbank mid-market rate plus an explicit percentage markup (typically 0.4 to 1.0 percent for major corridors). There is no hidden spread; the markup is itemized on the receipt.

Local-rail settlement on both ends. A USD-to-EUR Wise transfer touches ACH (or wire) in the United States and SEPA in the Eurozone. Neither leg crosses a border in the settlement sense.

Multi-currency accounts. Wise Business gives treasurers local account details in fifty-plus currencies, so receivables from European customers land in a local EUR balance without converting to USD until needed.

Limits and counterparty risk. Wise is a regulated electronic money institution, not a bank. Balances are safeguarded rather than deposit-insured. Limits on per-transfer size are real (typically capped in the low millions for business accounts, with negotiated higher limits for enterprise customers). Treasurers moving large blocks still use traditional banks for the largest transfers and Wise for the smaller, frequent ones.

The structural cost advantage holds for retail and SMB cross-border flows. For the high-value end of the corporate market, Wise's pricing per dollar is competitive but the operational story is different: treasurers care about counterparty risk, integration with their TMS, and the ability to settle very large amounts on a fixed timeline, which is where the global banks still win.

How Ripple and RippleNet Changed the Settlement Risk Profile

Ripple's product is two things that are easy to confuse: a payments network and a digital asset. The network (RippleNet) is a set of bilateral connections between financial institutions that uses Ripple's messaging and on-demand liquidity services. The digital asset (XRP) is sometimes used inside RippleNet's On-Demand Liquidity (ODL) product to bridge currencies in seconds without requiring either bank to pre-fund a nostro account in the destination currency.

What RippleNet ODL changes:

Eliminates pre-funded nostro accounts. A bank serving USD-to-PHP corridors no longer needs to maintain a peso-denominated balance at a Philippine correspondent. The liquidity is sourced just-in-time through XRP, which settles between exchanges in three to five seconds.

Compresses settlement risk. Without nostro pre-funding, treasury capital is not stranded waiting for the next end-of-day netting cycle. The capital savings on a high-volume corridor can be substantial; published Ripple case studies cite working-capital reductions in the tens of millions of dollars per bank per corridor.

Adds a different counterparty exposure. RippleNet ODL introduces exposure to XRP market liquidity. A liquidity event in the XRP market can affect the corridor pricing, which most treasurers prefer to model explicitly rather than ignore.

Limited geography. RippleNet ODL is live on a defined set of corridors (Mexico, Philippines, Vietnam, Singapore, several Gulf states, plus the United Kingdom and continental European links). The footprint expanded steadily through 2024 to 2026; the corridor coverage is now broad enough that ODL is a serious option for treasuries with exposure in those geographies but is not a universal solution.

The 2024 SEC settlement and the subsequent regulatory clarity in the United States moved Ripple from a controversial venture-stage option to a credible procurement choice for banks that want pre-funding compression on specific corridors.

What Stablecoin Corridors Add

USDC, USDT, and increasingly the bank-issued tokenized deposits (JPM Coin, regulated tokenized deposit pilots from Citi and HSBC) offer a different cross-border story. Settlement runs on blockchains (Ethereum, Solana, Avalanche, Stellar, Layer 2 networks) or on permissioned ledgers, and the value transfer between two parties is final in seconds without correspondent banking in between.

What works in 2026:

B2B treasury movement between known counterparties. A U.S. exporter and a European subsidiary, both with regulated stablecoin custody, can settle inter-company balances in seconds at sub-basis-point cost. This is the corridor where stablecoins have genuine adoption.

Weekend and after-hours settlement. Stablecoin rails do not respect bank hours, holidays, or the SWIFT business day. For payments that must move when banks are closed, the operational advantage is real.

Last-mile corridor extension. Stablecoin senders can on-ramp in major currencies and off-ramp through local exchanges in destination currencies where correspondent banking is thin (parts of Sub-Saharan Africa, parts of Latin America).

What does not work in 2026:

Retail consumer payments. The KYC, AML, and tax-reporting friction at on-ramp and off-ramp still makes stablecoin remittance more expensive than Wise for retail consumers on most major corridors.

Large-value institutional settlement. Counterparty risk concerns at the stablecoin issuer level (reserve composition, redemption rights, regulatory perimeter) keep institutional treasuries away from large stablecoin balances absent strict policy approval.

The regulatory perimeter is the variable that will determine 2027 to 2028 adoption. The GENIUS Act in the United States, MiCA in the European Union, and the FSB's global stablecoin guidance set the reserve, redemption, and supervisory expectations that determine which stablecoins survive as serious institutional rails.

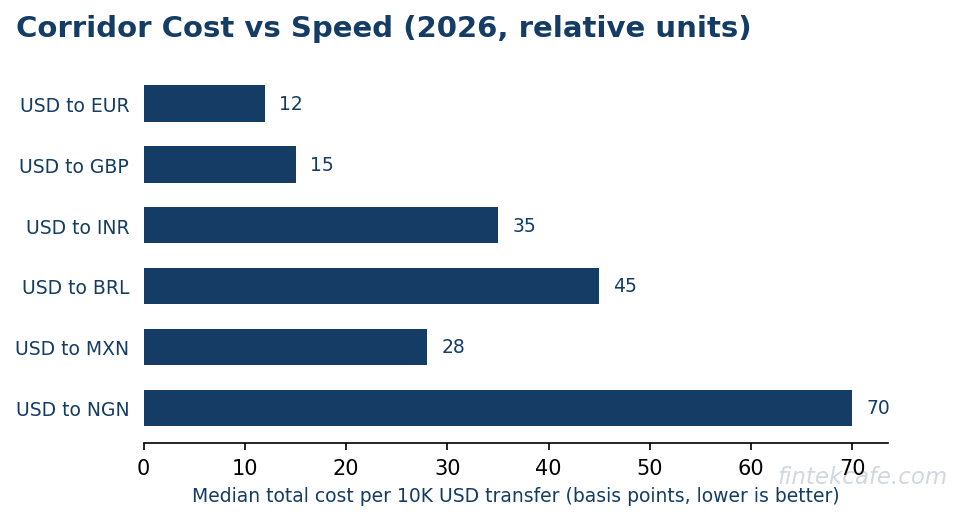

Corridor-by-Corridor Reality in 2026

The 2026 cross-border market is corridor-specific. A USD-to-EUR payment looks nothing like a USD-to-PHP payment, and pretending one product is best for both is the dominant procurement mistake. The table below captures the practical picture for the four corridors that dominate global enterprise treasury volume.

| Corridor | SWIFT gpi (median end-to-end) | Wise (cost + speed) | RippleNet ODL | Stablecoin (USDC) |

|---|---|---|---|---|

| USD to EUR | Under 1 hour; well-developed; FX margin varies by bank | Mid-market plus 0.4 to 0.6 percent; seconds to minutes | Available; limited adoption vs Wise on this corridor | Bank-issued tokenized deposits emerging; USDC viable for B2B |

| USD to INR | 1 to 3 hours typical; regulatory friction at receiving end | Mid-market plus 0.5 to 1.0 percent; minutes | Available via select Indian banks; growing volume | Less common; INR off-ramp friction |

| USD to BRL | 1 to 4 hours; PIX integration accelerates last mile | Mid-market plus 0.6 to 1.2 percent; minutes | Limited; not a primary ODL corridor | Growing; USDC-to-BRL via local exchanges, still retail-skewed |

| USD to MXN | Under 1 hour for major banks; SPEI receiving rail is fast | Mid-market plus 0.5 to 0.8 percent; minutes | One of RippleNet's flagship ODL corridors; seconds | Active corridor for B2B and remittance, regulated bridges |

The figures above are practitioner-reported ranges based on published vendor data and 2025 to 2026 industry surveys. The actual cost for any specific treasurer depends on the volume tier, the bank relationship pricing, and the destination-bank crediting practice.

A Decision Framework for Treasurers

The procurement question in 2026 is not "which provider," it is "which provider per corridor, per use case." The framework below captures how sophisticated treasury teams are structuring the choice.

- Segment by corridor volume. Group flows into high-volume corridors (where pricing leverage and integration justify a single provider) and long-tail corridors (where flexibility matters more than per-unit price).

- Segment by ticket size. Retail and SMB ticket sizes have different optimal providers than large-value treasury movements. A single provider rarely wins both segments cleanly.

- Segment by counterparty trust. Inter-company flows between subsidiaries can use settlement layers that retail flows to unknown counterparties cannot.

- Layer the providers. A treasury team in 2026 typically runs two to four cross-border rails: a global bank for large-value and regulatory cover, Wise or Airwallex for mid-market FX efficiency, RippleNet ODL on specific corridors where pre-funding savings justify it, and a stablecoin custody for inter-company and after-hours settlement.

- Measure landing reliability, not just speed. Median speed is easy to game. The metric that matters is the ninetieth-percentile landing time, the failed-transaction rate, and the time to resolve a stuck payment. Vendor selection on median alone produces operational disappointment.

The corridor-by-corridor approach replaces the legacy "primary banking partner" model with a portfolio model. The treasury teams running this well report fifteen to thirty percent reductions in cross-border cost per million dollars moved, with no degradation in landing reliability, compared to the single-bank baseline.

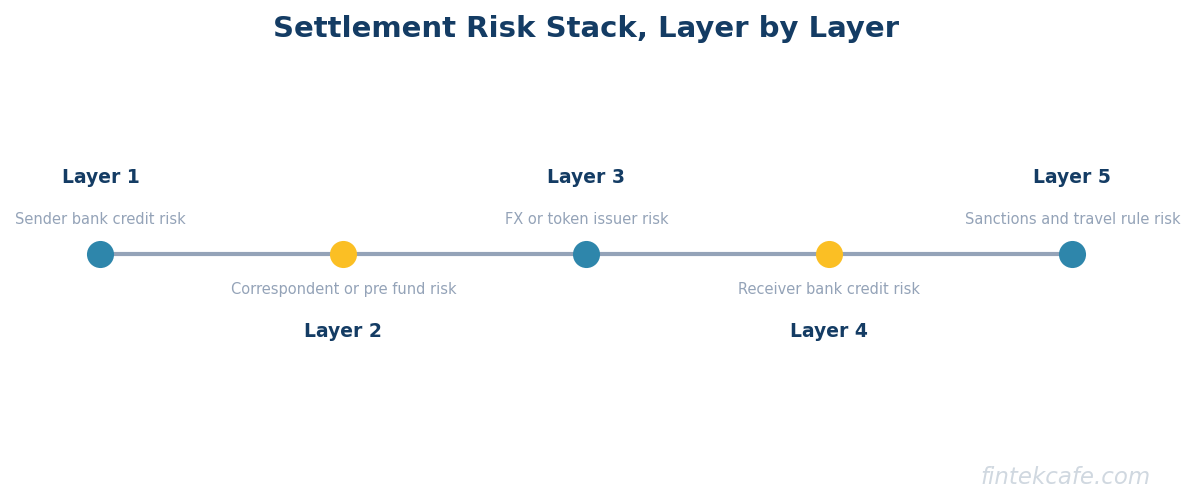

What This Means for Settlement Risk

Settlement risk is the chance that a payment is debited from the sender but never credited to the beneficiary, or is credited only after a delay long enough to affect liquidity decisions. The 2026 picture:

Correspondent banking under gpi. Settlement risk is operationally low but recovery time on a stuck payment can still be days. SWIFT gpi tracking dramatically reduces the "lost payment" failure mode but does not change the fundamental settlement model.

Wise and similar EMI providers. Settlement risk is concentrated at the EMI itself. Balances are safeguarded under regulatory frameworks but not deposit-insured. Counterparty diligence on the EMI's safeguarding bank is a real treasury control.

RippleNet ODL. Settlement risk is compressed in time (seconds to settle) but the exposure to XRP market liquidity is a different risk to model. Most banks running ODL also run hedging at the XRP layer.

Stablecoin rails. Settlement is final on-chain in seconds, which eliminates the recovery problem. The risk shifts to issuer credit risk (reserve composition, redemption rights), exchange counterparty risk on the on-ramp and off-ramp, and operational risk on the custody side.

The 2026 best practice for high-value flows is to model settlement risk per rail explicitly, not to assume "it cleared so it is final" across rail types.

Frequently Asked Questions

Is SWIFT going away?

No, but SWIFT in 2026 is a different network than SWIFT in 2015. The gpi service-level discipline, the ISO 20022 migration, and the connectivity to instant-payment networks (FedNow, RTP, Pix, UPI) on the receiving end have collectively made SWIFT a competitive option on most major corridors for most use cases. The narrative that SWIFT is being displaced is true at the edges (specific corridors, specific products) and not true in aggregate; SWIFT volumes have grown each year through 2025. We compare SWIFT to its closest regional alternatives in our SWIFT vs SEPA vs UPI guide.

Are Wise and Airwallex banks?

Neither Wise nor Airwallex is a bank in any major jurisdiction. Both operate as regulated electronic money institutions (EMIs) under UK, EU, Singapore, and Australian frameworks (with comparable licensing in other jurisdictions). Customer balances are safeguarded with regulated banks rather than insured under deposit-insurance schemes. The practical implication is that the counterparty risk profile is different from a Tier 1 bank, and treasurers should run that diligence explicitly.

Does RippleNet require holding XRP?

Only for the On-Demand Liquidity (ODL) product. RippleNet's messaging and bilateral payment services do not require XRP. ODL specifically uses XRP as the bridge asset that lets a participating bank source destination-currency liquidity without pre-funding a nostro account. Banks using ODL typically do not hold XRP directly; the liquidity is sourced through market makers and exchanges in real time.

Are stablecoin payments legal for corporate cross-border use?

In most major jurisdictions in 2026, yes, with conditions. The European Union's MiCA framework, the United States' GENIUS Act, Singapore's MAS framework, and Japan's payment-services act all permit corporate use of regulated stablecoins under defined rules. The conditions matter: corporate users typically need a regulated on-ramp and off-ramp counterparty, robust travel-rule compliance for cross-border movement above defined thresholds, and clear treasury policy on accepted stablecoin issuers. The regulatory perimeter continues to tighten, and treasurers should consult counsel for specific corridors. For a fuller comparison of fast-rail alternatives in the United States, see our FedNow real-time payments guide.

What is the realistic cost of cross-border in 2026 versus 2015?

For the dominant retail and SMB use cases, the all-in cost of a USD-to-EUR cross-border payment has fallen from roughly four to six percent in 2015 (combined fees plus FX spread on a typical small remittance) to roughly 0.5 to 1.5 percent in 2026 on the same corridor using Wise, Revolut, or similar providers. For large-value institutional flows, the per-payment cost has fallen less dramatically (the FX spread on a one hundred million dollar trade was always tight) but the operational and settlement-risk improvements are substantial. The frontier is not pure cost reduction anymore; it is operational reliability and settlement-time predictability.

Key Takeaways

- SWIFT gpi has compressed the legacy correspondent rail from days to under an hour for most major corridors. The messaging and settlement layer is no longer the slow part of cross-border payment. The remaining variance is at the beneficiary bank.

- Wise's mid-market FX model genuinely beats banks on cost for retail and SMB cross-border flows. It does not displace banks for large-value institutional settlement, and the EMI counterparty model is a different risk to size than a banking-license counterparty.

- RippleNet ODL eliminates pre-funded nostro accounts on the corridors it covers. The capital efficiency story is real on Mexico, the Philippines, and several other ODL corridors. The exposure to XRP market liquidity is a separate risk to model.

- Stablecoin rails are credible in 2026 for inter-company B2B treasury, weekend settlement, and corridor extension where correspondent banking is thin. They are not yet the dominant rail for retail or for large institutional settlement, and the regulatory perimeter is still tightening.

- The 2026 treasury procurement pattern is corridor-by-corridor and provider-portfolio. Single-provider strategies are giving up fifteen to thirty percent of the achievable cost reduction without buying meaningful risk reduction in return.

Related reading on FinTekCafe

- What Is ISO 20022? the structured payment-messaging standard behind SWIFT MX, FedNow, and the rest of the modern rail layer

- SWIFT vs SEPA vs UPI: Global Payment Networks Compared

- What Is FedNow? Real-Time Payments in the U.S.

- Cross-Border Payments Explained: How They Work and Why They Are So Slow

- How Wire Transfers Actually Work: The Anatomy of a Wire

Related Articles

The Consortium Stablecoin: Why the Card Networks Are Funding Their Own Disruption

Visa, Mastercard, and Stripe are backing an open stablecoin consortium. The playbook is older than it looks: own the new rail's governance before it owns you.

Merchant of Record vs Payment Facilitator: Who Holds the Risk in Your Payment Stack

The four payment models compared: who holds tax, chargeback, and compliance liability as merchant of record, payfac, marketplace, or processor, and which fits.

Interchange Fees Explained: Who Really Pays for Card Payments

What interchange fees are, who pays whom in the four-party model, why rates vary, what regulation changed, and how merchants realistically cut card costs.