Chargebacks Explained: The Dispute System Behind Card Payments

A chargeback is a forced reversal of a card payment, initiated by the cardholder's bank, that pulls the money back from the merchant while the card networks adjudicate who keeps it. The mechanism dates to the Fair Credit Billing Act of 1974, a US consumer-protection law written for an era of paper receipts, and it now underpins dispute volume measured in the hundreds of millions: a Mastercard-commissioned Datos Insights study projected global chargebacks to reach 337 million annually by 2026, up from 238 million in 2023. For merchants the direct reversal is the smallest part of the cost. Each dispute carries a fee of roughly 15 to 100 USD regardless of outcome, consumes operational time, and counts against network monitoring thresholds that, past roughly one percent of transactions, can end a merchant's ability to accept cards at all. Executives tend to discover the chargeback system the first time it threatens that access. This is how it actually works.

Key Takeaways

- A chargeback is not a refund. A refund is a merchant's decision; a chargeback is the issuing bank reversing the payment on the cardholder's claim, with a fee attached, a ratio consequence, and a dispute process the merchant enters as the defending party.

- The lifecycle runs dispute, evidence, representment, pre-arbitration, arbitration. Each stage has deadlines measured in days, and a missed deadline is an automatic loss regardless of the merits.

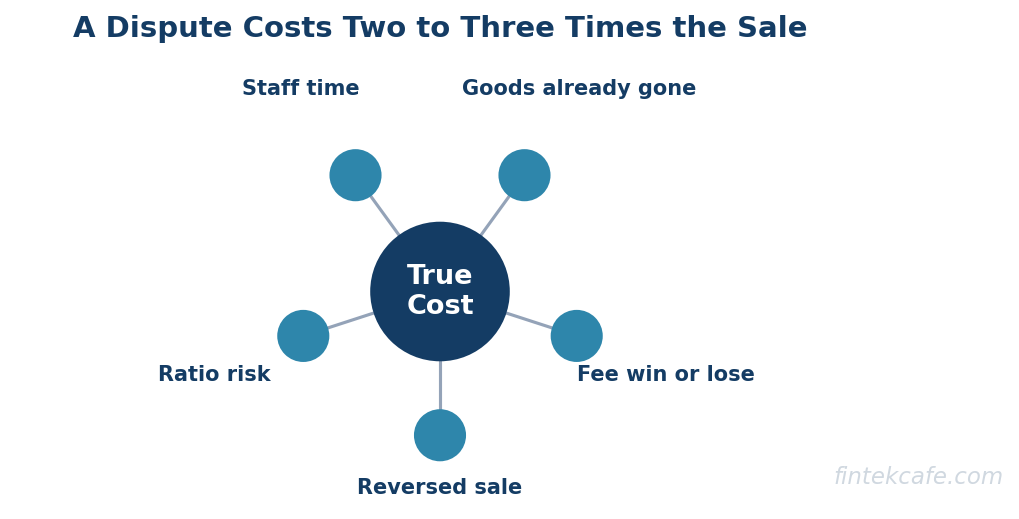

- The true cost of a dispute is a multiple of the transaction: the reversed sale, a per-dispute fee paid win or lose, shipped goods that are gone, and operational time. Industry estimates consistently put all-in cost at two to three times the disputed amount.

- Friendly fraud, a legitimate cardholder disputing a legitimate charge, is the dominant category; Visa has attributed as much as three quarters of card-not-present fraud disputes to first-party misuse. The networks' compelling-evidence rules exist specifically to give merchants a defense against it.

- The ratio is the existential number. Network monitoring programs flag merchants around 0.9 to 1.5 percent disputes-to-transactions; sustained breach brings fines, then termination, then industry blacklisting. Managing the ratio matters more than winning any individual dispute, which is why refunding is often the correct business decision even when the merchant is right.

What a Chargeback Is, and Why the Deck Is Stacked

The chargeback was designed as consumer protection, and it still works as one: a cardholder billed for goods that never arrived, or defrauded by a stolen card number, gets their money back without suing anyone. The design choice that matters for merchants is where the burden sits. The cardholder asserts; the merchant proves. The issuing bank that adjudicates the first round is the bank whose customer is making the claim. Money moves against the merchant at the start of the process, not the end. None of this is a conspiracy; it is a 1974 allocation of trust, built when the merchant was a storefront and the fraud was a stolen physical card, applied to an economy where the merchant is a website and the cardholder's word is the primary evidence.

Understanding the flow requires knowing the cast: the cardholder and their issuing bank on one side, the merchant and its acquiring bank (usually fronted by a processor) on the other, with the card network in the middle setting rules and running arbitration. The network is not a neutral party in spirit: its brand promise to cardholders is that the card is safe to use anywhere, and the dispute system is how that promise is funded. How these parties connect in the underlying payment flow is covered in how Visa processes a transaction, and the division of labor on the merchant's side in payment gateway versus payment processor.

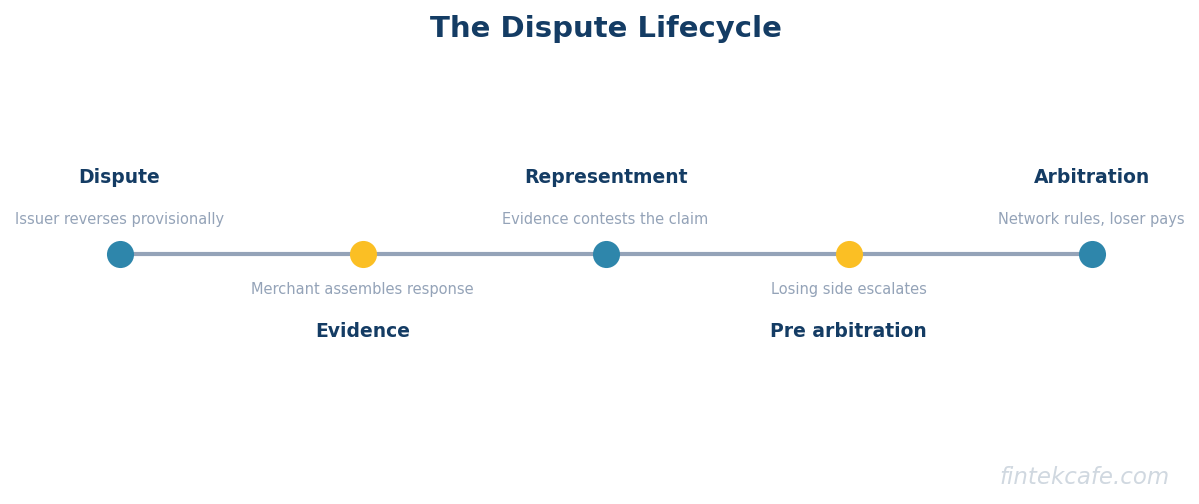

The Dispute Lifecycle, Stage by Stage

Every dispute walks some prefix of the same five-stage path. Most end at stage one or three; almost none reach five.

| Stage | What happens | Who acts | Typical window |

|---|---|---|---|

| 1. Dispute | Cardholder contests the charge; issuer assigns a reason code and reverses funds provisionally | Cardholder, issuing bank | Up to 120 days from transaction or expected delivery |

| 2. Evidence | Merchant is notified and assembles its response | Merchant, processor | Days, inside the response window |

| 3. Representment | Merchant submits evidence contesting the dispute; issuer re-reviews | Merchant via acquirer | Roughly 20 to 45 days to respond, by network |

| 4. Pre-arbitration | Losing side escalates; second exchange of positions | Either side | Weeks |

| 5. Arbitration | Network rules; loser pays fees in the hundreds of USD | Card network | Final, no appeal |

Stage one: the dispute. The cardholder contacts their issuer, or increasingly taps a "dispute this charge" button in a banking app. The issuer assigns a reason code and, in most cases, pulls the funds from the merchant's acquirer immediately. The cardholder generally has 120 days from the transaction or the expected delivery date to initiate, which means a merchant's dispute exposure outlives the sale by four months.

The reason-code system. Every dispute carries a code that determines what evidence is relevant. The networks each maintain their own taxonomy, but all of them reduce to four families: fraud ("that was not authorized," Visa's 10.x codes), consumer disputes ("the transaction was authorized but the merchant failed," such as goods not received, code 13.1), processing errors (duplicate or wrong-amount charges, 12.x), and authorization issues. The code is the dispute's legal theory. Evidence that would win under one code loses under another, which is why competent dispute operations start by reading the code, not the transaction.

Stage three: representment. The merchant re-presents the transaction with evidence: delivery confirmation, device and IP data, usage logs, correspondence, signed terms. Response windows run roughly 20 to 45 days depending on network, and silence is concession; a substantial share of disputes are lost by default because no one answered in time.

The compelling-evidence change. The most consequential recent rule shift is Visa's Compelling Evidence 3.0, live since April 2023. For card-not-present fraud disputes under code 10.4, a merchant who can show two prior undisputed transactions from the same device, IP, or account identity within the previous year can shift liability back to the issuer, on the logic that a customer with an established purchase history did not have their card stolen; they made a purchase and disputed it anyway. Mastercard's first-party fraud rules have moved the same direction. The networks, in effect, have conceded that a large share of "fraud" disputes are nothing of the kind, which is the system's most honest acknowledgment of the friendly-fraud problem.

Stages four and five: pre-arbitration and arbitration. The losing side can escalate to a second exchange, and then to the network itself, whose ruling is final and whose fees run into the hundreds of USD for the loser. Arbitration economics only make sense for large tickets; for a typical e-commerce transaction, the process is designed to end before it gets there.

What a Chargeback Actually Costs

The reversed transaction is the visible cost. The invisible costs are larger, and industry estimates consistently put the all-in cost at two to three times the disputed amount.

The components: the transaction amount, gone provisionally at stage one and permanently on a loss. The dispute fee, roughly 15 to 100 USD depending on processor and merchant risk tier, charged win or lose. The goods or services, already shipped or delivered, unrecoverable in most consumer categories. The operational load: evidence assembly is manual, deadline-driven work, and a dispute operation handling thousands of cases per month is a staffed function, not a side task. And the ratio, which is where cost becomes existential risk.

The monitoring programs. Both major networks run programs that track each merchant's dispute ratio. Visa's consolidated acquirer monitoring program, rolled out from April 2025, measures combined fraud and dispute activity against transaction counts, with the threshold for excessive activity set at 1.5 percent and tightening toward 0.9 percent from 2026. Mastercard's excessive-chargeback program flags merchants at 1.5 percent with at least 100 disputes in a month. A merchant inside a program faces escalating fines and remediation demands; a merchant who stays inside one faces termination by their acquirer and placement on Mastercard's MATCH list, the industry file that makes acquiring banks decline the relationship for years. For a business that sells online, that is not a fine; it is the revenue line going to zero. The ratio, not the individual dispute, is the number a CFO should track monthly.

Friendly Fraud: The Dominant Category

The dispute system's central irony is that its largest use case is the one it was not designed for. Friendly fraud, also called first-party misuse, is a legitimate cardholder disputing a charge they made: sometimes cynically (keeping the goods and the money), often casually (disputing instead of requesting a refund because the bank's app makes it one tap), and sometimes innocently (not recognizing a billing descriptor and assuming fraud). Visa has attributed as much as 75 percent of card-not-present fraud disputes to first-party misuse, and the category grew with exactly the forces that grew e-commerce: subscriptions people forgot, cryptic descriptors, one-tap dispute buttons, and household members using saved cards.

Friendly fraud is why chargeback management cannot be delegated entirely to fraud tooling. A fraud model screens the transaction; friendly fraud is a dispute about a transaction that was, at the moment it happened, perfectly legitimate. The defenses are different, and confusing the two categories is the most common structural error in merchant dispute programs. The transaction-screening side of the problem, stopping actual stolen-card fraud before authorization, is its own discipline, covered in real-time fraud detection in payments.

What Actually Reduces Chargebacks, and What Does Not

The effective interventions are unglamorous and mostly upstream of the dispute.

Clear billing descriptors. A meaningful share of "fraud" disputes are recognition failures: the cardholder sees an unfamiliar corporate name and taps dispute. A descriptor that matches the brand the customer bought from, with a reachable phone number or URL, removes the cheapest category of dispute a merchant can lose.

Fast, findable refunds. Every dispute begins as a customer who wanted their money back. A refund policy that is easy to find and fast to execute intercepts disputes before they exist, at the cost of the refund and nothing else: no fee, no ratio impact. Merchants who make refunds adversarial are buying chargebacks at a two-to-three-times markup.

3-D Secure where the economics fit. 3DS authentication shifts liability for fraud disputes to the issuer on authenticated transactions. The trade is checkout friction and some approval-rate impact, which is why the correct deployment is selective, applied to risky segments rather than all traffic.

Network alert services. Verifi (owned by Visa) and Ethoca (owned by Mastercard) notify merchants of disputes in a pre-chargeback window, allowing a refund before the case becomes a chargeback: the fee and the ratio hit are avoided even though the revenue is not. For a merchant near a monitoring threshold, alerts are the cheapest ratio relief available.

Evidence hygiene by design. Merchants who win representments decided to win them at integration time: capturing device fingerprints, IP addresses, delivery confirmations, and login telemetry as a matter of course, so that compelling-evidence submissions are a query rather than an archaeology project.

What does not work is equally consistent. Fighting every dispute on principle loses money on fees and labor for cases with no evidence. Blanket 3DS on all traffic trades approval rate for protection most transactions did not need. Aggressive fraud-rule tightening after a chargeback scare quietly declines good customers, a cost that never appears on the chargeback report. And "chargeback guarantee" services priced as a percentage of all revenue frequently cost more than the disputes they absorb; the arithmetic depends on the merchant's actual dispute rate, and the vendor knows the arithmetic better than the buyer. Merchants processing across multiple providers have an additional structural option, since routing and provider redundancy change the dispute-handling surface, a topic covered in payment orchestration and multi-processor routing.

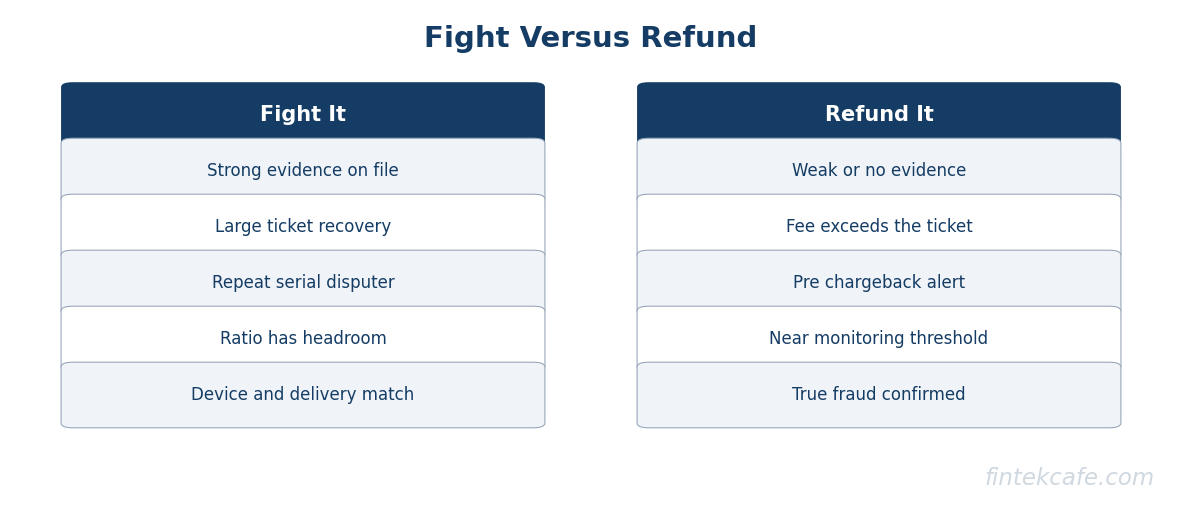

Fight or Refund: The Decision Framework

For each dispute, and more usefully for each dispute category, the decision reduces to comparing expected recovery against total cost of fighting, under the shadow of the ratio.

| Situation | Decision | Reasoning |

|---|---|---|

| Pre-chargeback alert received, any ticket size | Refund via alert | Avoids fee and ratio hit; cheapest exit the system offers |

| Small ticket, weak or no evidence | Refund or concede | Fee plus labor exceeds recovery even on a win |

| Small ticket, strong evidence, repeat disputer | Fight | Win rate is high and conceding trains serial abuse against the merchant |

| Large ticket, strong evidence (delivery, device match, usage logs) | Fight, escalate if needed | Expected recovery justifies fees; CE 3.0 data can shift liability entirely |

| Large ticket, weak evidence | Refund and fix upstream | A loss costs fee plus ratio; the money was already gone |

| Merchant near a monitoring threshold | Refund aggressively, buy alerts | Ratio survival outranks individual recoveries; termination risk dominates |

| True stolen-card fraud confirmed | Concede, tighten screening | The dispute is legitimate; fighting it wastes money and goodwill |

Two principles generalize the table. First, the ratio outranks the recovery: a merchant at 0.8 percent should be refunding disputes a merchant at 0.2 percent should be fighting, because the marginal dispute costs them different things. Second, fight rate is a symptom, not a strategy: a merchant whose win rate is high is probably not fighting enough, and one whose win rate is low is fighting cases the evidence never supported. The durable wins come from descriptors, refund speed, alerts, and evidence capture, which is to say from treating chargebacks as a system to be engineered rather than a stream of individual injustices to be litigated.

FAQ

What is a chargeback and how is it different from a refund?

A chargeback is a payment reversal initiated by the cardholder's bank after the cardholder disputes a charge; a refund is a voluntary return of funds initiated by the merchant. The difference matters because a chargeback carries a dispute fee of roughly 15 to 100 USD regardless of outcome, counts against the merchant's network dispute ratio, and puts the merchant into an adjudication process as the defending party. A refund costs only the refunded amount.

How long does the chargeback process take?

Cardholders generally have up to 120 days from the transaction or expected delivery to dispute. Once a dispute is filed, the merchant has roughly 20 to 45 days to respond with evidence depending on the network, the issuer then re-reviews, and optional pre-arbitration and arbitration stages add weeks each. A contested dispute commonly runs two to four months end to end; arbitration cases run longer and are rare because the loser pays fees in the hundreds of USD.

What is friendly fraud?

Friendly fraud, or first-party misuse, is a legitimate cardholder disputing a charge they actually made: because they did not recognize the billing descriptor, forgot a subscription, preferred the bank's dispute button to the merchant's refund process, or intended to keep both the goods and the money. It is the dominant dispute category in card-not-present commerce; Visa has attributed as much as three quarters of CNP fraud disputes to first-party misuse, and rules like Visa Compelling Evidence 3.0 exist to give merchants a defense against it.

When should a merchant fight a chargeback instead of refunding?

Fight when the evidence is strong and the ticket justifies the cost: delivery confirmation, matching device and IP history, or usage logs, on a transaction large enough that recovery exceeds the fee and labor. Refund when evidence is weak, the ticket is small, or the merchant is near a network monitoring threshold, where protecting the dispute ratio is worth more than any individual recovery. A pre-chargeback alert should almost always be resolved with a refund, since it avoids both the fee and the ratio impact.

What happens if a merchant gets too many chargebacks?

Card networks monitor each merchant's ratio of disputes to transactions. Sustained ratios in the 0.9 to 1.5 percent range place a merchant into monitoring programs with escalating fines and remediation requirements, and continued breach leads the acquiring bank to terminate the merchant account and file the business on Mastercard's MATCH list, which causes other acquirers to refuse it for years. Losing card acceptance entirely is the terminal risk, which is why the ratio matters more than any single dispute.

Related reading on FinTekCafe

Related Articles

The Consortium Stablecoin: Why the Card Networks Are Funding Their Own Disruption

Visa, Mastercard, and Stripe are backing an open stablecoin consortium. The playbook is older than it looks: own the new rail's governance before it owns you.

Merchant of Record vs Payment Facilitator: Who Holds the Risk in Your Payment Stack

The four payment models compared: who holds tax, chargeback, and compliance liability as merchant of record, payfac, marketplace, or processor, and which fits.

Interchange Fees Explained: Who Really Pays for Card Payments

What interchange fees are, who pays whom in the four-party model, why rates vary, what regulation changed, and how merchants realistically cut card costs.