Payment Orchestration: Why Merchants Route Across Multiple Processors

Key Takeaways

- Payment orchestration is a routing layer that sits above multiple processors and acquirers and decides where each transaction goes. Single-processor checkout is a sensible default for a small merchant, but at scale it becomes a single point of failure and a quiet margin leak, because one processor's downtime is total downtime and one processor's authorization rate is the ceiling on revenue.

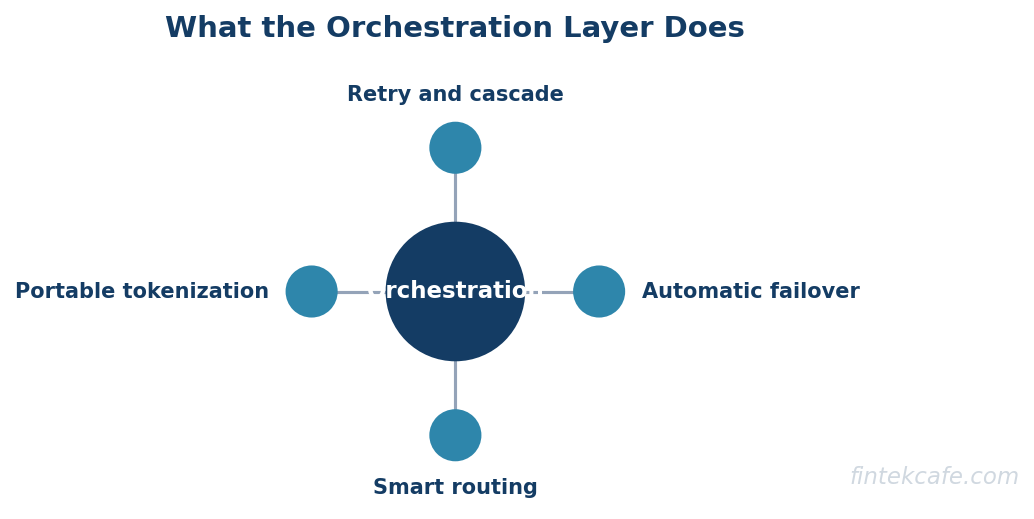

- The orchestration layer does specific work: smart routing by cost and performance, automatic failover when a processor is down, retry and cascade logic for declined transactions, tokenization that is portable across processors, network-token management, and unified reporting across every provider.

- Merchants adopt orchestration for four reasons that translate directly to money: higher authorization rates, lower processing cost, redundancy against outages, and geographic coverage through local acquiring. Of these, the authorization-rate gain is usually the largest, because a small percentage of recovered transactions on large volume is significant revenue.

- The build-versus-buy decision carries an irony. The orchestration layer exists to free merchants from lock-in to a single processor, yet a managed orchestration platform can become its own lock-in, because portable tokenization and routing logic are exactly what is hard to migrate away from. Owning the token vault is the hedge that preserves the independence orchestration is supposed to provide.

- Authorization-rate optimization is the mechanism that moves revenue. A transaction declined by one processor may be approved by another, and intelligent retry, cascade, and network-token management recover a meaningful share of would-be-lost sales. On large volume, moving the approval rate by even a point or two is a direct and recurring revenue gain.

Single-Processor Checkout Becomes a Liability at Scale

For a new merchant, connecting to one payment processor and accepting cards is the obvious and correct choice. One integration, one contract, one dashboard, one place to reconcile. The simplicity is worth far more than any theoretical benefit of complexity, and adding processors before there is volume to justify them is premature optimization. The single-processor default is right, until it is not.

The point at which it stops being right arrives with scale, and it arrives as two distinct problems. The first is reliability: when all transactions flow through one processor, that processor's downtime is the merchant's downtime, and an outage during peak hours means every attempted purchase fails with no fallback. The second is economics: one processor offers one set of authorization rates, one fee schedule, and one geographic footprint, and the merchant is capped by all three. A transaction that processor would decline is simply lost, a region that processor serves poorly is a region the merchant serves poorly, and a fee the processor charges is a fee the merchant pays, with no alternative to route to. At scale, that single point of dependence is both a reliability risk and a margin leak.

Payment orchestration is the response. This article defines what an orchestration layer actually does, explains the four reasons merchants adopt it and how each converts to money, confronts the build-versus-buy decision and the lock-in irony hiding inside it, and shows how authorization-rate optimization actually moves revenue. A comparison table sets single processor, orchestration platform, and in-house routing side by side on authorization rate, cost, redundancy, and effort.

What a Payment Orchestration Layer Does

Payment orchestration is a software layer that sits above multiple payment processors and acquirers and decides, for each transaction, which provider to send it to and what to do if that provider declines or fails. It abstracts the individual processors behind a single integration, so the merchant builds to the orchestration layer once instead of integrating each processor separately, and the layer handles the routing underneath. The work it does breaks into six functions.

Smart routing sends each transaction to the provider most likely to approve it at the lowest cost, based on factors like card type, geography, transaction size, and each processor's recent performance. Instead of every transaction going to the same place, routing matches the transaction to the provider that handles it best.

Automatic failover detects when a processor is down or degraded and reroutes traffic to a healthy provider, so a single processor's outage no longer means lost sales. This is the redundancy that single-processor checkout structurally cannot provide.

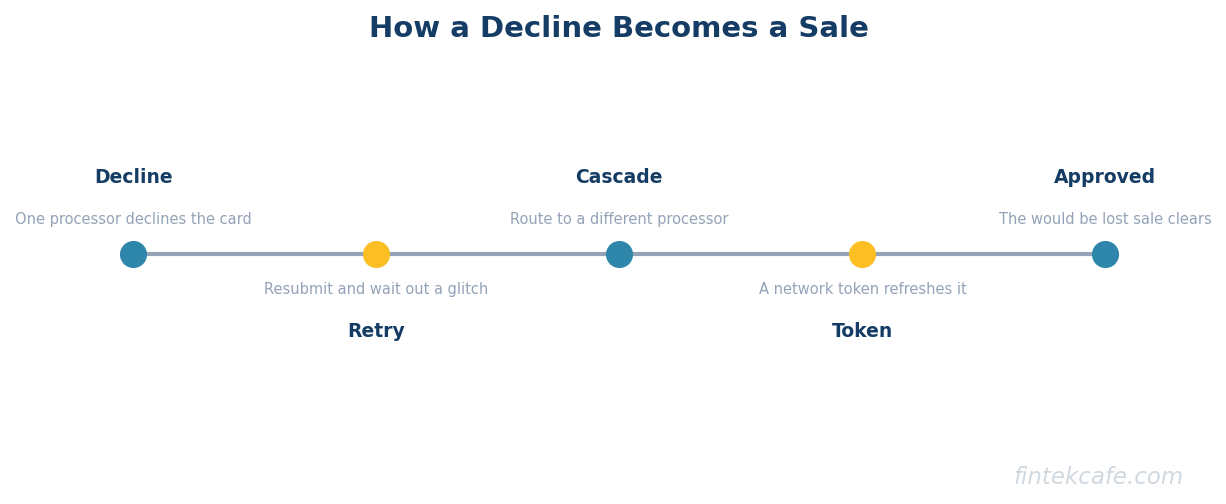

Retry and cascade logic handles declines intelligently. When a transaction is declined, the layer can retry it, potentially through a different processor, a cascade, because a decline by one provider does not mean every provider would decline it. This recovery is where much of the authorization-rate gain comes from.

Portable tokenization stores card credentials as tokens the merchant controls, rather than tokens locked to one processor. This is the function that preserves the merchant's freedom to route across providers and to switch providers, because the card data is not trapped inside any single processor's vault.

Network-token management handles the network-issued tokens that replace raw card numbers and keep credentials current when cards are reissued or expire, which lifts approval rates on stored-card and recurring transactions.

Unified reporting consolidates data from every processor into one view, so the merchant can reconcile, analyze cost and performance, and make routing decisions on complete information rather than stitching together separate dashboards. The distinction between the processor that moves the money and the gateway and routing layer that sits in front of it is foundational here, and it is laid out in the explainer on the difference between a payment gateway and a payment processor.

Why Merchants Adopt It

Merchants do not adopt orchestration for elegance. They adopt it because each of its benefits converts to money, and at scale the amounts are large.

Higher authorization rates. This is usually the biggest prize. Not every legitimate transaction is approved on the first attempt: issuers decline for reasons ranging from risk models to temporary glitches, and a transaction one processor cannot get approved another sometimes can. Orchestration recovers a share of these through routing and cascade, and because the gain is a percentage of total transaction volume, even a modest improvement in the approval rate is significant revenue on a large base. The mechanics of how a transaction actually gets authorized across the network, covered in the breakdown of how a card transaction is processed, are what create the room for one provider to succeed where another fails.

Lower processing cost. Different processors charge different rates for different transaction types, regions, and card brands. Routing each transaction to the cheapest provider that will approve it reduces blended processing cost, and on high volume the saving compounds. Orchestration also gives the merchant negotiating leverage, because a merchant who can shift volume between processors has a credible alternative in every fee conversation, which a single-processor merchant does not.

Redundancy. Failover turns a processor outage from a revenue emergency into a non-event. For a merchant whose sales depend on checkout working every minute, the ability to reroute around a down provider is insurance whose value shows up the first time a major processor has an outage during peak traffic.

Geographic coverage. Authorization rates are higher and costs lower when transactions are processed through a local acquirer in the customer's region rather than cross-border. Orchestration lets a merchant route transactions to local acquiring in each market, improving both approval rates and cost for international sales, which a single global processor often cannot match everywhere it operates.

The Build-Versus-Buy Decision and Its Irony

A merchant that decides it needs orchestration faces the familiar choice: buy a managed orchestration platform, or build the routing layer in-house. The trade-offs are the usual ones, with one twist that is easy to miss.

A managed platform delivers orchestration quickly, with processor integrations, routing logic, tokenization, and reporting already built and maintained. It fits merchants that want the benefits without building and operating payment infrastructure, at the cost of a recurring fee and a dependency on the platform. Building in-house gives complete control over routing logic and avoids the platform fee, at the cost of substantial and ongoing engineering investment to build integrations, maintain them as processors change, and operate a system where bugs directly affect revenue.

The irony sits inside the buy option. Orchestration exists to free the merchant from dependence on any single processor, yet a managed orchestration platform can become its own lock-in. The very features that deliver the value, portable tokenization and the routing logic, are the features that are hardest to migrate away from, because the merchant's stored card credentials and the accumulated routing configuration live inside the platform. A merchant that solved single-processor lock-in by adopting a platform can find it has simply moved the lock-in up one layer, from the processor to the orchestrator. This is the same vendor-dependence dynamic that recurs throughout enterprise infrastructure, and the same instinct that drives interest in alternatives that avoid trapping the customer, including the merchant-cost pressure from pay-by-bank and account-to-account payments.

The hedge against the irony is the token vault. A merchant that retains control of its own tokenization, keeping the card credentials in a vault it owns rather than one the orchestrator owns, preserves the ability to switch orchestration platforms or move routing in-house later. Owning the vault keeps the independence that orchestration was adopted to gain. Merchants that treat portable tokenization as a checkbox feature rather than a strategic asset are the ones who discover the new lock-in only when they try to leave.

How Authorization-Rate Optimization Moves Revenue

The single most important thing to understand about orchestration is why authorization-rate optimization is worth so much, because it is the benefit that justifies the rest. The logic is arithmetic. A merchant processing large volume loses a measurable percentage of attempted transactions to declines, and a portion of those declines are recoverable: legitimate customers whose transactions failed for reasons that a retry, a different processor, or a current network token would resolve. Recovering even a small fraction of those is a direct revenue gain, and because it is a percentage of total volume, the absolute number is large for any merchant at scale.

Three mechanisms do the recovering. Intelligent retry resubmits a failed transaction in a way more likely to succeed, including waiting out a temporary issue or adjusting how the transaction is presented. Cascade routes a declined transaction to a different processor that may approve it, because issuers and processors do not all decide identically. Network-token management keeps stored credentials current, so recurring and saved-card transactions do not fail because a card was reissued, which is a common and entirely recoverable cause of decline.

The reason this matters more than cost savings is that it is found revenue, not reduced expense. A point of processing-cost reduction improves margin on transactions that already succeeded. A point of authorization-rate improvement adds transactions that would otherwise have been lost entirely, which is new top-line revenue at almost pure margin. For a merchant weighing whether orchestration is worth the effort, the authorization-rate math is usually the deciding figure, and it is why the function is the centerpiece of the orchestration pitch. Recovering revenue also depends on not introducing new friction or false declines, which ties orchestration directly to the accuracy of real-time fraud detection in payments: a routing layer that lifts approvals while letting fraud through has not actually gained anything.

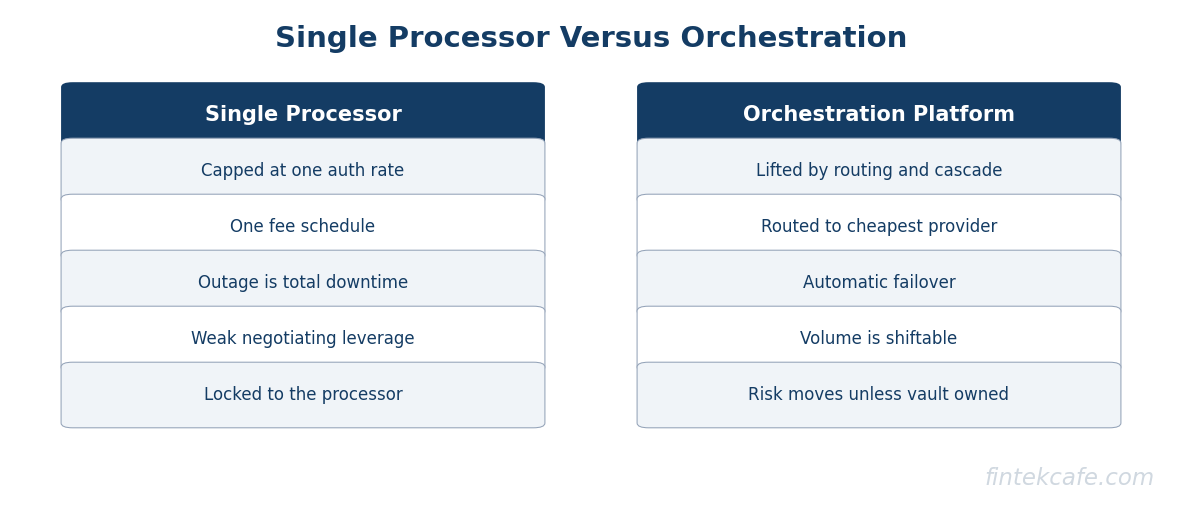

Single Processor vs Orchestration Platform vs In-House Routing

The three approaches differ on the axes a merchant actually weighs: authorization rate, cost, redundancy, and the effort to run them.

| Dimension | Single processor | Orchestration platform | In-house routing |

|---|---|---|---|

| Authorization rate | Capped at one provider's rate | Lifted by routing, cascade, network tokens | Lifted, limited by team's routing skill |

| Processing cost | One fee schedule, no leverage | Routed to cheapest provider, plus a platform fee | Routed to cheapest, no platform fee |

| Redundancy | None, outage is total downtime | Automatic failover across providers | Failover if built and maintained |

| Setup and operating effort | Lowest, one integration | Moderate, one integration to the platform | Highest, build and maintain everything |

| Negotiating leverage | Weak, no alternative to shift to | Strong, volume is shiftable | Strong, volume is shiftable |

| Lock-in risk | Locked to the processor | Risk shifts to the platform unless vault is owned | Lowest, merchant controls everything |

The pattern is that the single processor wins only on simplicity and is exposed on every other axis at scale. The orchestration platform captures most of the benefit for moderate effort, with the caveat that the lock-in risk moves rather than disappears. In-house routing maximizes control and avoids both the platform fee and the platform lock-in, at the price of the highest engineering investment, which makes it a fit mainly for the largest merchants with payments as a core competency.

When Orchestration Is Worth It

Orchestration is not a universal upgrade, and adopting it too early is its own mistake. The signals that a merchant has crossed into the territory where it pays off are concrete: transaction volume large enough that a one-point authorization-rate gain is material revenue, a reliability requirement where a processor outage during peak hours is unacceptable, international sales that suffer from cross-border processing, and enough processing spend that routing to cheaper providers produces meaningful savings. A merchant with low volume, a single market, and modest reliability needs gets little from orchestration and pays its complexity for nothing.

The evidence consistently shows that merchants who adopt orchestration at the right time, when scale has turned single-processor checkout into a genuine point of failure and margin leak, capture real and recurring gains in approval rates, cost, and resilience. Those who adopt it too early carry complexity without a return, and those who adopt a managed platform without retaining control of their own tokenization solve one lock-in by creating another. The discipline is the same as with any infrastructure decision: match the solution to the scale of the actual problem, and keep control of the assets, the token vault above all, that preserve the freedom the solution was meant to provide.

FAQ

What is payment orchestration?

Payment orchestration is a software layer that sits above multiple payment processors and acquirers and decides, for each transaction, which provider to route it to and what to do if that provider declines or fails. It abstracts individual processors behind a single integration and handles smart routing, automatic failover, retry and cascade logic, portable tokenization, network-token management, and unified reporting. The goal is to lift authorization rates, lower cost, and add redundancy that a single processor cannot provide.

How does payment orchestration increase authorization rates?

A transaction declined by one processor is sometimes approved by another, because issuers and processors do not decide identically and some declines are temporary or recoverable. Orchestration recovers these through intelligent retry, cascade routing to a different processor, and network-token management that keeps stored credentials current. Because the gain is a percentage of total transaction volume, even a small improvement in the approval rate is significant new revenue for a high-volume merchant, and that revenue is at almost pure margin.

Should a merchant build or buy payment orchestration?

Buying a managed platform delivers orchestration quickly with integrations and routing already built, for a recurring fee and a dependency on the platform. Building in-house gives full control and avoids the fee but requires substantial ongoing engineering. The key caveat is the lock-in irony: a managed platform can become its own lock-in through portable tokenization and routing logic that are hard to migrate. Retaining control of your own token vault preserves the ability to switch later, regardless of which option you choose.

What is the lock-in risk with payment orchestration platforms?

Orchestration exists to free a merchant from dependence on a single processor, but a managed orchestration platform can become its own lock-in. The features that deliver the value, portable tokenization and accumulated routing configuration, are exactly what is hard to migrate away from, because the merchant's stored card credentials and routing logic live inside the platform. The hedge is to own the token vault, keeping card credentials in a vault the merchant controls so it can change platforms or move routing in-house.

When is payment orchestration worth it for a merchant?

Orchestration pays off when transaction volume is large enough that a one-point authorization-rate gain is material revenue, when a processor outage during peak hours would be unacceptable, when international sales suffer from cross-border processing, or when processing spend is high enough that routing to cheaper providers saves meaningfully. A low-volume, single-market merchant with modest reliability needs gets little from orchestration and should keep the simplicity of a single processor until scale changes the math.

Related reading on FinTekCafe

Related Articles

The Consortium Stablecoin: Why the Card Networks Are Funding Their Own Disruption

Visa, Mastercard, and Stripe are backing an open stablecoin consortium. The playbook is older than it looks: own the new rail's governance before it owns you.

Merchant of Record vs Payment Facilitator: Who Holds the Risk in Your Payment Stack

The four payment models compared: who holds tax, chargeback, and compliance liability as merchant of record, payfac, marketplace, or processor, and which fits.

Interchange Fees Explained: Who Really Pays for Card Payments

What interchange fees are, who pays whom in the four-party model, why rates vary, what regulation changed, and how merchants realistically cut card costs.