Stablecoins for Treasury: The CFO Guide to USDC, Tokenized Deposits, and Where Settlement Risk Actually Lives in 2026

Key Takeaways

- Corporate treasury teams have quietly moved past the stablecoin curiosity phase. In 2026, the question is no longer whether to pilot but which instrument, in which corridor, and on which rails.

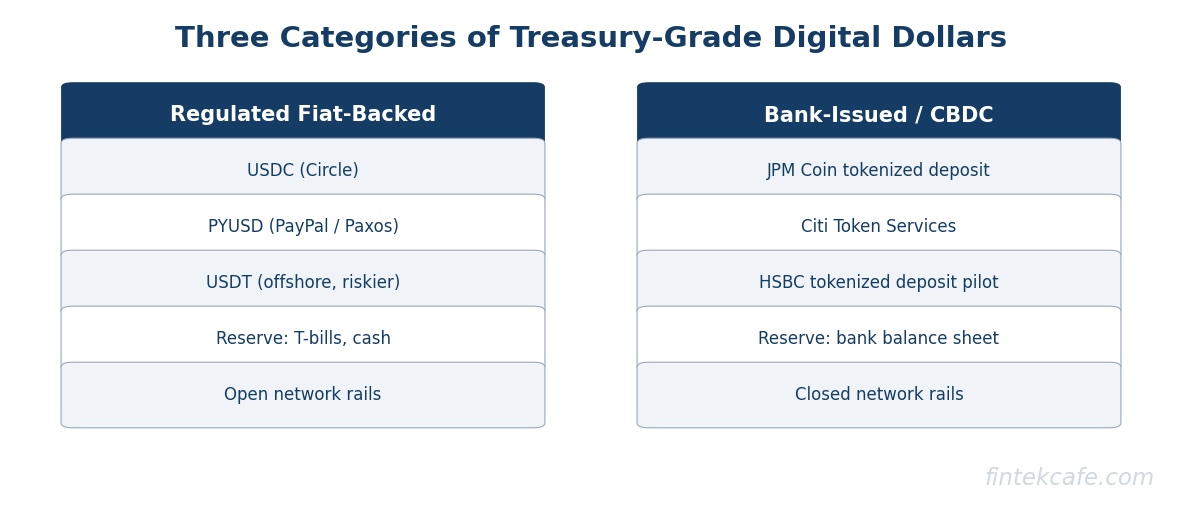

- Three categories matter and should never be conflated: regulated fiat-backed stablecoins (USDC, PYUSD, EURC), bank-issued tokenized deposits (JPM Coin, Citi Token Services, HSBC Tokenised Deposits), and central bank digital currency pilots.

- The use cases that survive scrutiny are narrow and specific. 24/7 cross-border settlement, intra-day liquidity inside a group, and supplier payments in dollar-shortage corridors are real. Most other claimed use cases dissolve under stress testing.

- Settlement risk does not live where the marketing implies. The real risk surfaces are reserve quality, redemption pathway integrity, smart-contract exposure, and the KYC chain that connects the treasurer to the eventual recipient.

- The post-MiCA, post-GENIUS Act regulatory state in 2026 is workable but uneven. CFOs piloting in the US, EU, Singapore, and the UAE face four different sets of constraints. Pretending it is one global framework is the fastest way to a finding.

The Quiet Shift Inside Corporate Treasury

For several years, stablecoin coverage was dominated by retail trading, crypto exchange flows, and the noisy collapse of unbacked algorithmic experiments. Inside corporate treasury, the topic was treated as a curiosity at best and a reputational hazard at worst. That posture has shifted.

The shift is not loud. No major corporate has issued a press release announcing that its treasury runs on stablecoins. Yet by 2026, treasury teams at multinational manufacturers, technology platforms, commodity traders, and global retailers have moved from declining the conversation to running quiet pilots. The pilots are typically small (low single-digit millions in USD-equivalent), narrow (one corridor or one supplier program), and time-boxed. They are also producing data that suggests at least some of the use cases are durable.

This piece argues a specific position. Stablecoins are not a treasury revolution. They are an addition to the treasurer's toolkit that solves a narrow set of problems better than the existing rails. Treating them as either a generational opportunity or an existential risk overstates both. The CFO's job is to know which problems they actually solve, where the risk lives, and how to pilot without creating exposure that the audit committee cannot defend.

Three Categories, Different Animals

The single most damaging mistake in treasury conversations about digital money is treating "stablecoins" as one category. Three distinct instruments are usually being discussed under that label, with materially different risk profiles, governance, and regulatory treatment.

Regulated fiat-backed stablecoins are the most familiar category. The dominant instruments are USDC (issued by Circle), PYUSD (issued by Paxos for PayPal), and EURC (issued by Circle in euro). USDT, issued by Tether, dominates global market share but is materially less attractive for corporate treasury use because of disclosure and counterparty considerations. These instruments are tokens on public blockchains (predominantly Ethereum and Solana, with a growing presence on Layer 2 networks) that represent a claim on a basket of cash and cash-equivalent reserves held by the issuer.

Bank-issued tokenized deposits are a different animal entirely. JPM Coin (JPMorgan), Citi Token Services, HSBC Tokenised Deposits, and similar instruments at major global banks are not stablecoins. They are commercial bank deposit money represented on a private distributed ledger, redeemable one-for-one against the issuing bank, and usable only within that bank's permissioned network. The benefit is 24/7 movement and programmability. The trade-off is that the network is the bank's network, not a public one.

Central bank digital currency pilots are the third category. As of 2026, the European Central Bank has progressed the digital euro through its preparation phase but not launched. The US position remains explicitly that no retail CBDC will be issued. The Federal Reserve has been clearer about pursuing a wholesale CBDC concept narrowly. Other central banks (Singapore, Hong Kong, the UAE) are running active pilots. For corporate treasury, CBDCs are a watch item, not a 2026 deployment option in most jurisdictions.

The three categories are not substitutes. A treasurer who is considering "stablecoins" is usually thinking about category one. A treasurer who is considering 24/7 movement of large balances within an existing banking relationship is usually thinking about category two. Conflating them produces incoherent risk assessments.

A Comparison Across the Real Instruments

| Instrument | Type | Issuer Type | Network | Reserve Backing | Redemption Pathway | Practical Use |

|---|---|---|---|---|---|---|

| USDC | Fiat-backed stablecoin | Regulated non-bank | Public (multi-chain) | Cash and short-duration Treasuries, monthly attestation | Through Circle Mint accounts, T+0 to T+1 to bank | Cross-border settlement, supplier payments |

| PYUSD | Fiat-backed stablecoin | Regulated trust (Paxos) | Public (Ethereum, Solana) | Cash and short-duration Treasuries, monthly attestation | Through Paxos, to bank | Consumer-adjacent flows, PayPal ecosystem |

| EURC | Fiat-backed stablecoin | Regulated under MiCA | Public (multi-chain) | Euro deposits and short-duration government securities | Through Circle Mint accounts, to bank | Intra-European settlement, euro-denominated supplier flows |

| USDT | Fiat-backed stablecoin | Offshore trust | Public (multi-chain) | Mixed reserves, weekly attestation | Through Tether direct relationship, restrictive | Generally unsuitable for corporate treasury in regulated jurisdictions |

| JPM Coin | Tokenized deposit | JPMorgan | Private permissioned | Commercial bank deposit at JPMorgan | One-for-one redemption against JPM account | Intra-group liquidity, JPM client-to-client settlement |

| Citi Token Services | Tokenized deposit | Citigroup | Private permissioned | Commercial bank deposit at Citi | One-for-one redemption against Citi account | 24/7 cross-border movement within Citi network |

| HSBC Tokenised Deposits | Tokenized deposit | HSBC | Private permissioned | Commercial bank deposit at HSBC | One-for-one redemption against HSBC account | Multi-currency settlement within HSBC corridors |

The table simplifies. Real treasury due diligence requires reading the issuer disclosures, the legal opinion on the instrument's status in the relevant jurisdiction, and the operational documentation for the network. The point of the table is the structural one. The instruments are not the same.

The Use Cases That Actually Survive Scrutiny

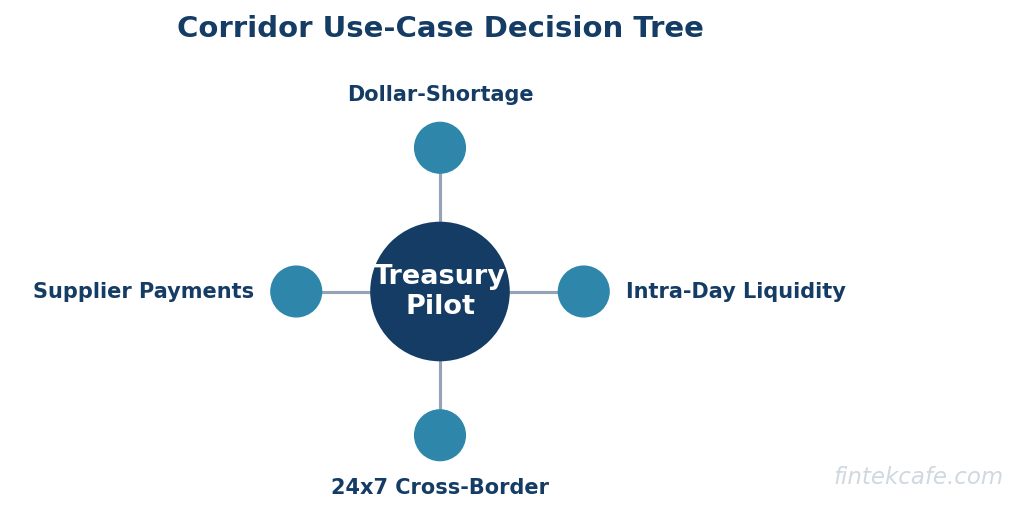

A treasury team that approaches stablecoin pilots seriously will encounter a long list of suggested use cases. Most of them fail under stress testing. A short list survives. The short list is where the pilots concentrate.

24/7 cross-border settlement in dollar corridors. Wire transfers in major currencies still close on banking days, with practical cut-offs that mean a Friday afternoon US-to-Asia wire effectively settles Monday. Stablecoins settle on chain in minutes, every day. For corporates with operations in time zones that systematically miss the cut-offs, the value is real. The relevant question is whether the corporate has counterparties that can receive stablecoins and convert them locally, which is increasingly the case for large suppliers in major hubs.

Intra-group liquidity inside a multinational. A group treasurer with operating entities in fifteen countries spends meaningful effort moving cash across entities, often through correspondent banking arrangements that take days. Tokenized deposits at a single bank (JPM Coin, Citi Token Services) collapse that movement to seconds. The value is operational, not financial: it is the elimination of float and reconciliation cost, not yield pickup.

Supplier payments in dollar-shortage corridors. Suppliers in countries with restricted dollar access (parts of Africa, Latin America, and South Asia) increasingly prefer stablecoin settlement to wire transfer, because the wire transfer either does not arrive, arrives at a punitive exchange rate, or arrives late. For corporates with supply chains running through these corridors, stablecoin payments are not a treasury optimization; they are a supplier retention tool.

Twenty-four-seven liquidity for trading desks. Corporate treasuries that hedge commodity exposure or operate FX programs around the clock have a natural use for instant settlement instruments. The use case is real but narrow, and is more relevant to commodity traders and large airlines than to the typical multinational.

The use cases that do not survive scrutiny are equally instructive.

Yield on idle cash. Some early pitches suggested holding treasury cash in stablecoins to earn DeFi yield. The risk profile is not consistent with corporate treasury policy in any jurisdiction. The yield is not free; it compensates lenders for counterparty and smart-contract risk that a treasurer cannot meaningfully diligence.

Replacing the banking relationship. Stablecoins do not replace the bank. They add an instrument that flows through the existing banking relationship at the on-ramp and off-ramp. A corporate that thinks of stablecoins as bank-disintermediation has misunderstood the operational reality.

Payroll. With narrow exceptions (some contractor populations in specific corridors), payroll is not a stablecoin use case in 2026. The regulatory and tax complexity overwhelms any operational benefit.

Where Settlement Risk Actually Lives

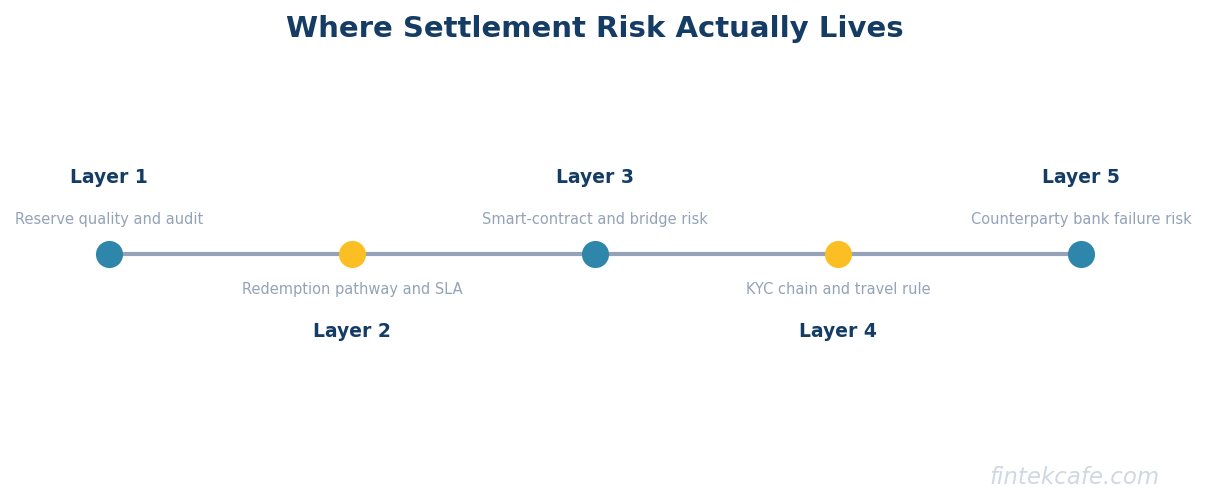

The marketing for digital money tends to focus on the wrong risks. The actual risk surfaces that treasury and risk teams should diligence look like this.

Reserve quality and segregation. A fiat-backed stablecoin is a claim on a reserve. The relevant questions are what the reserve holds, whether it is segregated from the issuer's operating funds, how often it is attested, and by whom. USDC's reserves are held in cash and short-duration US Treasuries with monthly attestations by a major audit firm. PYUSD operates under the New York Department of Financial Services framework with similar disclosures. USDT's disclosure has improved but is materially less granular and more concentrated. The treasury team should be reading the actual attestation, not the marketing summary.

Redemption pathway integrity. The token is only as good as the redemption path. Under normal market conditions, every major fiat-backed stablecoin can be redeemed by an institutional holder through a direct relationship with the issuer. Under stressed conditions, redemption gates can appear. The Silicon Valley Bank weekend in March 2023, during which USDC temporarily traded below parity because a portion of its reserves was at SVB, is the canonical example. The lesson is that a treasury holding stablecoins inherits the issuer's banking relationships and any concentration risk those relationships carry.

Smart-contract risk. Public-blockchain stablecoins move through smart contracts on public networks. A bug, exploit, or governance attack on the underlying network or on the token contract itself can freeze or compromise balances. The major regulated issuers have shown the ability to freeze tokens at specific addresses, which is reassuring against illicit use but is itself a power that a treasurer needs to be comfortable with. The decision to operate on Ethereum, Solana, or a Layer 2 should be made deliberately, with awareness of the trade-offs each network carries.

KYC chain integrity. When a corporate sends stablecoins to a counterparty, the regulatory expectation is that the counterparty has been onboarded somewhere in the chain. If the counterparty is a regulated business holding accounts at a regulated exchange or with a regulated stablecoin issuer, the chain is intact. If the counterparty receives the tokens to a self-custodied wallet and the chain breaks there, the corporate's compliance team carries the risk. Diligence on the KYC chain is a precondition for any production flow.

Custody. The corporate has to hold the tokens somewhere. Self-custody requires operational maturity that most corporate treasuries do not have. Institutional custody (through firms such as Anchorage, Fireblocks, BitGo, BNY Mellon's digital asset custody, or the digital asset arms of the major custodian banks) is the standard answer. The custody arrangement is the single most important operational decision, more consequential than the token choice.

The Regulatory State in 2026

The regulatory state is the variable that most affects pilot design. As of 2026, four regimes matter.

The European Union under MiCA. The Markets in Crypto-Assets regulation is fully in force, with the e-money token and asset-referenced token classifications providing a workable framework for fiat-backed stablecoins. Issuers must hold reserves with specific quality and segregation requirements, redemption is a legal right, and disclosure is standardized. EURC and other MiCA-compliant euro stablecoins exist within this framework. USDC has navigated the framework. USDT has not, and is not freely available to European corporates through compliant venues, which has changed the EU competitive landscape materially.

The United States under the GENIUS Act and related framework. Federal legislation enacted in 2025 brought payment stablecoins under a defined federal framework with a path for both federally chartered and state-supervised issuers. The result is workable certainty in the US for the major regulated issuers, with state-level supervision (notably NYDFS) continuing to play a significant role. The framework does not authorize a US retail CBDC, but it does formalize the role of payment stablecoins in the financial system.

The United Kingdom. The Financial Conduct Authority has progressed the stablecoin regulatory perimeter under the Financial Services and Markets Act 2023, with implementation continuing through 2026. The UK regime is recognizable to a US treasury team but with different reserve and authorization requirements.

Asia and the Middle East. Singapore (under the Monetary Authority of Singapore's payment services framework), Hong Kong (under the HKMA's stablecoin regime), and the UAE (under the Central Bank of the UAE's payment token framework) have each established workable regimes. Japan operates a distinct regime in which only banks, trust banks, and registered money transfer agents can issue stablecoins.

The practical implication for a multinational CFO is that a stablecoin treasury program is jurisdiction-specific in a way that wire transfer programs are not. The same instrument can be permissible in one country, restricted in another, and require local registration in a third. Pretending it is one global framework is the fastest way to a compliance finding.

A Treasury Readiness Checklist

Before authorizing a first stablecoin pilot, a CFO should be able to answer the following questions affirmatively.

Governance is in place. Treasury policy has been amended to reference digital assets. The board or audit committee has been briefed. Counsel has produced a written opinion on the instruments and jurisdictions in scope. The risk function has signed off on the framework.

The use case is bounded. The pilot has a defined corridor or counterparty population, a defined notional cap, a defined time window, and defined success criteria that are operational, not financial.

The instruments are short-listed. The pilot uses one or two named instruments, with documented diligence on reserve quality, redemption pathway, network choice, and regulatory status in the relevant jurisdictions.

Custody is decided. A qualified custodian has been selected, contracted, and integrated. Self-custody is not the answer for a first pilot.

On-ramp and off-ramp partners are contracted. The path from operating cash to tokens and back is documented, with named providers and committed pricing.

KYC chain has been mapped. Every counterparty in the pilot has been onboarded by a regulated provider. Compliance has reviewed the chain.

Accounting and tax treatment is agreed. The accounting firm has confirmed the balance sheet and income statement treatment. The tax function has reviewed transaction-level implications.

Operational runbooks exist. Treasury operations has documented payment instructions, reconciliation procedures, exception handling, and incident response. The runbooks have been walked through with treasury operations and internal audit.

The exit is planned. The pilot can be wound down in a defined window with all tokens redeemed to cash and all custody relationships terminated. No pilot should run without a defined exit.

A CFO who can answer all nine questions is ready to authorize a pilot. A CFO who cannot is ready to start the work that comes before authorization, which is the more useful place to be.

What This Means for the CFO Office

The thesis worth carrying out of this analysis is narrow but important. Stablecoins are not transforming corporate treasury. They are adding a useful instrument for a narrow set of problems. The CFOs who get value from them in 2026 will treat them like any other treasury instrument: with a defined use case, a documented risk framework, named counterparties, and a clear governance posture.

The CFOs who lose money on them will either over-rotate (treating them as a strategic platform shift) or under-rotate (ignoring them and discovering in three years that competitors have quietly built supplier programs that depend on rails the laggard cannot operate). The work to avoid both errors is the same: a serious pilot, scoped narrowly, run by the existing treasury team with real risk and compliance involvement, and reviewed honestly.

The category is past its hype cycle. The work is treasury work now.

FAQ

Are stablecoins legal for corporate treasury use in 2026? In the major jurisdictions (the US under the GENIUS Act framework, the EU under MiCA, the UK, Singapore, Hong Kong, the UAE, Japan), regulated fiat-backed stablecoins issued by authorized issuers are legal for corporate use, with jurisdiction-specific constraints. The work is in matching the specific instrument, custodian, and counterparty to the specific jurisdictional rules. Treating it as one global framework is the mistake.

What is the difference between USDC and a tokenized deposit? USDC is a token on a public blockchain representing a claim on a reserve held by Circle. A tokenized deposit (such as JPM Coin) is commercial bank deposit money represented on a bank's private ledger. USDC is interoperable across counterparties on public networks. A tokenized deposit only works inside its issuing bank's network. The risk profiles are different and the use cases are different.

Can a corporate hold stablecoins on its balance sheet? Yes, with appropriate accounting treatment. Most corporates classify regulated fiat-backed stablecoins as digital assets under the relevant accounting standard. The accounting firm should be consulted before any pilot starts, since classification affects the income statement and balance sheet presentation.

What is the smallest credible pilot for stablecoin treasury? A bounded corridor program (one supplier population, one currency pair, one custodian, low single-digit millions in notional, sixty to ninety days). Smaller than that and the learnings are not credible. Larger than that and the governance work has to be in place before the pilot starts.

Is the SVB-USDC depeg a reason to avoid stablecoins? It is a reason to diligence the issuer's banking relationships, not a reason to avoid the category. The depeg was a function of reserve concentration at a single failing bank. Reserve diversification disclosures have improved materially since. The takeaway is that the issuer's banking and reserve management is the actual diligence target.

Will CBDCs replace stablecoins for corporate use? Not in 2026 and not in any near-term horizon visible from 2026. Most major central banks have either declined retail CBDC issuance (notably the US) or are pursuing limited wholesale concepts that do not address the corporate treasury use cases that fiat-backed stablecoins and tokenized deposits already serve. The instruments will coexist, not substitute.

Related reading on FinTekCafe

- Stablecoins Explained: What They Are and Why They Matter

- CBDCs: Central Bank Digital Currencies and the Future of Money

- Cross-Border Payments Explained: The Real Plumbing of Global Money

- What Is FedNow? Real-Time Payments in the US

- ISO 20022: The Payments Message Standard That Changes Everything

- Smart Contracts Explained: Beyond the Crypto Hype

Related Articles

The Consortium Stablecoin: Why the Card Networks Are Funding Their Own Disruption

Visa, Mastercard, and Stripe are backing an open stablecoin consortium. The playbook is older than it looks: own the new rail's governance before it owns you.

Merchant of Record vs Payment Facilitator: Who Holds the Risk in Your Payment Stack

The four payment models compared: who holds tax, chargeback, and compliance liability as merchant of record, payfac, marketplace, or processor, and which fits.

Interchange Fees Explained: Who Really Pays for Card Payments

What interchange fees are, who pays whom in the four-party model, why rates vary, what regulation changed, and how merchants realistically cut card costs.