How Venture Capital Actually Works: A Guide for Founders and Operators

Venture capital is the most misunderstood asset class in finance. US VC firms manage roughly 1.3 trillion USD in committed capital across more than 3,400 active funds as of 2026, and they deployed an estimated 175 billion USD into startups in 2025 alone. Founders mythologize it. The press sensationalizes it. And most people who interact with VCs - including many founders raising money - do not understand the basic mechanics of how a fund works, how partners get paid, or why VCs behave the way they do.

That matters. VC behavior is not random. It is driven by fund structure, incentive alignment, and return math that, once understood, makes every interaction with a VC more predictable. Understanding the mechanics does not guarantee a successful raise, but it eliminates the most common mistakes founders make when they do not understand what is happening on the other side of the table.

This guide explains how venture capital actually works - fund structure, economics, decision-making, portfolio math, and the parts nobody explains until it is too late.

What a Venture Capital Fund Actually Is

A venture capital fund is a pool of money raised from institutional investors, managed by a small team (the "general partners"), and invested into early-stage private companies over a defined period.

The key players:

Limited Partners (LPs) are the investors who put money into the fund. LPs include university endowments (Yale, Harvard, Stanford), pension funds (CalPERS, Ontario Teachers'), sovereign wealth funds (GIC, Abu Dhabi Investment Authority), foundations, family offices, and fund-of-funds. LPs commit capital - they do not send all the money upfront. When the VC identifies an investment, it "calls" capital from LPs as needed.

General Partners (GPs) are the VC firm's partners who manage the fund - sourcing deals, making investment decisions, sitting on boards, and ultimately returning money to LPs. GPs also invest their own money into the fund, typically 1-5% of the total fund size. This "GP commit" aligns their interests with LPs.

Portfolio companies are the startups that receive the investments.

Fund Lifecycle

A typical VC fund has a 10-year life:

- Years 1-3 (Investment Period): The fund deploys capital into new investments. Most funds make 20-30 investments during this period.

- Years 3-7 (Value Creation): The fund supports portfolio companies, makes follow-on investments in winners, and writes off failures.

- Years 7-10 (Harvest Period): Portfolio companies exit through acquisitions or IPOs. The fund distributes proceeds to LPs.

- Extensions: Funds often extend 1-2 years beyond the initial 10-year term to allow remaining investments to mature.

This 10-year horizon is why VCs push for growth and exits. They are not running an endowment. They have a contractual obligation to return capital to LPs within a defined timeframe.

Fund Economics: How VCs Make Money

VC compensation has two components: management fees and carried interest ("carry").

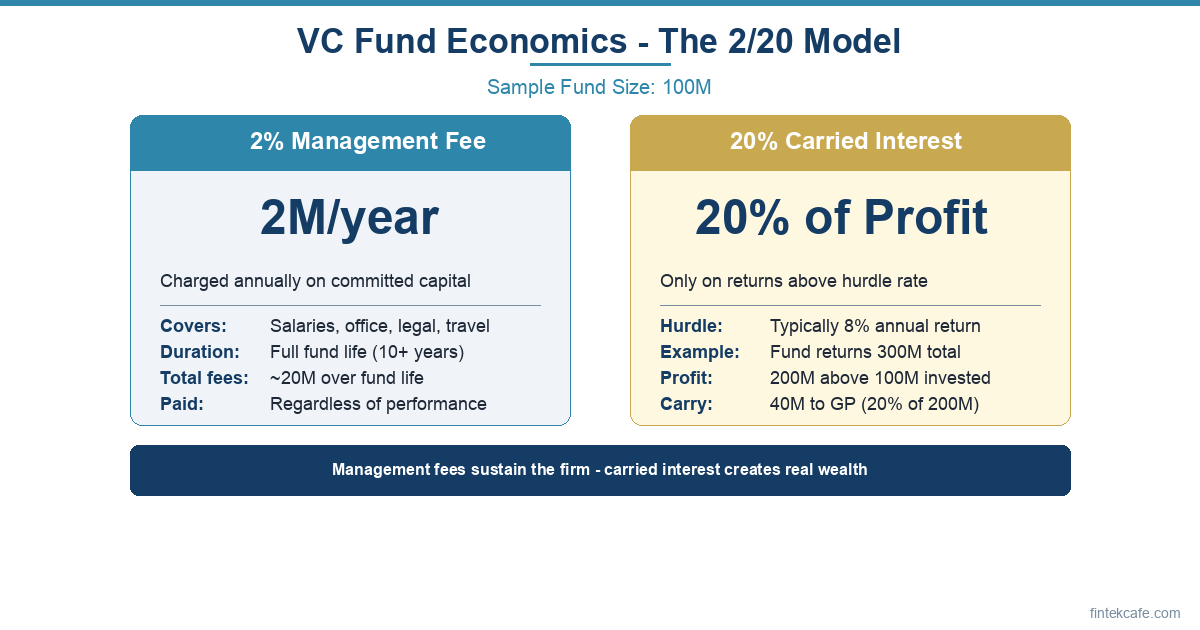

Management Fees

The fund charges an annual management fee, typically 2% of committed capital during the investment period and 2% of invested capital (lower) during the harvest period. On a 200 million dollar fund, that is 4 million dollars per year in management fees.

Management fees cover salaries, office rent, travel, legal costs, and operations. For large funds, management fees are substantial. A billion-dollar fund generates 20 million dollars per year in management fees - enough to run a sizable organization regardless of investment performance.

This creates a structural incentive that founders should understand: VCs are incentivized to raise larger funds, because management fees scale with fund size. A GP who raises a 500 million dollar fund earns 2.5x the management fees of a 200 million dollar fund. This incentive is separate from investment performance and is one reason VC fund sizes have inflated dramatically over the past decade.

Carried Interest

Carry is where the real money is. Carried interest is the GP's share of fund profits, typically 20% (though top-tier firms charge 25-30%). But carry only kicks in after LPs receive their money back plus a preferred return (the "hurdle rate," typically 8% annually).

Here is how the math works on a 200 million dollar fund:

- The fund returns 600 million dollars total (3x return)

- LPs first receive their 200 million dollars back

- Of the 400 million dollars in profit, GPs take 20% (80 million dollars)

- LPs receive the remaining 320 million dollars

That 80 million dollars in carry is split among the GP team, which might be 3-6 partners. Individual partner carry on a successful fund can be 10-30 million dollars. On a breakout fund (5-10x return), it can be much more.

The critical implication: carry is binary for most investments. A company that returns 2x the fund's investment is nice but does not move the needle. VCs need 10x, 50x, or 100x outcomes on individual investments to generate meaningful carry. This is why VCs push portfolio companies toward massive outcomes even when a smaller, profitable exit would serve the founders well.

The J-Curve

New funds initially show negative returns. Management fees are charged from day one, but investments take years to generate returns. Plotting fund performance over time creates a "J-curve" - a dip into negative territory followed by an upward swing as exits materialize.

This means LP investors in VC are committing to years of negative interim returns before seeing profits. The willingness to accept this J-curve is why VC capital comes from institutional investors with long time horizons, not retail investors seeking quarterly returns.

How VCs Decide What to Invest In

The decision-making process varies by firm, but the typical pattern follows a funnel.

Deal Flow

A partner at a top-tier firm might see 1,000-2,000 companies per year. Of those, roughly 100 will get a meeting. Of those, 20-30 will go through due diligence. Of those, 10-15 will receive a term sheet. Of those, 5-8 will result in an investment (some founders choose other investors).

Deal flow comes from:

- Founder referrals from existing portfolio company founders

- Co-investor networks sharing deals with other VCs

- Conferences and demo days (Y Combinator, Techstars, sector-specific events)

- Inbound applications (low conversion rate - under 1% at top firms)

- Proactive outreach by partners who identify promising companies through market research

The most important source is founder referrals. When a successful portfolio company founder recommends a deal, it carries more weight than any pitch deck. This is why the VC industry is so network-driven and why founders who lack existing VC connections face structural disadvantages.

Investment Criteria

At the early stage (seed and Series A), VCs evaluate:

Team. At pre-product or early-product stages, the team is the investment. VCs assess founder-market fit (does this founder have a unique advantage in this market?), technical capability, ability to recruit, and resilience. The "would you work for this person?" test is real.

Market size. VCs need markets large enough to support a multi-billion dollar company. A market with a total addressable market (TAM) of 500 million dollars is too small for a VC-backed company because even capturing 20% of it only produces 100 million dollars in revenue - not enough for a venture-scale outcome. VCs look for TAMs in the tens of billions.

Product and traction. At Series A, VCs expect evidence of product-market fit - retention curves, revenue growth, user engagement metrics. At seed, the bar is lower but some evidence of customer demand (waitlists, letters of intent, early revenue) matters.

Competitive dynamics. VCs assess the defensibility of the business. Network effects, switching costs, proprietary data, and regulatory advantages create moats that make an investment more attractive.

Timing. Why now? What has changed in the market, technology, or regulatory environment that makes this company viable today when it would not have been five years ago? The "why now" question is often the most important one.

The Partner Champion Model

Most VC firms require a single partner to "champion" a deal internally. That partner does the work - meeting the founders, conducting diligence, writing the investment memo - and then presents to the partnership for approval.

This means your pitch is really two pitches: one to convince the partner, and a second (delivered by the partner) to convince the other partners who have never met you. The investment memo the partner writes is often the deciding document. Founders who help their champion partner tell a compelling internal story have an advantage.

Term Sheets and Deal Structure

When a VC decides to invest, the terms are documented in a term sheet - a non-binding agreement that outlines the key economic and governance terms.

Valuation

Pre-money valuation is the company's value before the investment. Post-money valuation is pre-money plus the investment amount. If a company raises 10 million dollars at a 40 million dollar pre-money valuation, the post-money valuation is 50 million dollars, and the investor owns 20% (10/50).

Valuation gets the most attention but is often less important than other terms.

Liquidation Preference

This is the term that matters most in practice. A 1x liquidation preference means the investor gets their money back before common shareholders (founders and employees) receive anything. On a 10 million dollar investment with 1x preference, the investor receives the first 10 million dollars of any exit proceeds.

In a large exit (500 million dollars+), liquidation preference barely matters - everyone does well. In a moderate exit (50-100 million dollars), it can dramatically reduce what founders and employees receive. In a small exit (under the total amount raised), founders may receive nothing.

Participating preferred is the aggressive version: investors get their money back first AND share in the remaining proceeds pro-rata. Non-participating preferred (more founder-friendly) forces investors to choose between their liquidation preference or converting to common stock and sharing pro-rata.

Anti-Dilution Protection

If the company raises a future round at a lower valuation (a "down round"), anti-dilution provisions adjust the investor's ownership upward. Broad-based weighted average is standard and relatively fair. Full ratchet (rare) is extremely investor-friendly and can devastate founder ownership.

Board Seats and Governance

Lead investors typically receive a board seat. At Series A, a typical board is 3 seats: 1 founder, 1 investor, 1 independent. By Series C, the board may have 5-7 seats with multiple investor representatives.

Board composition matters enormously in practice. Board members approve budgets, executive hires, and major strategic decisions. In downside scenarios (running out of cash, forced acquisition), the board - not the founders - controls the outcome.

Portfolio Math: Why VCs Behave the Way They Do

The single most important concept for understanding VC behavior is the power law distribution of returns.

In a typical VC fund:

- 40-50% of investments return less than the capital invested (partial or total losses)

- 20-30% return 1-3x (modest returns)

- 10-20% return 3-10x (solid performers)

- 1-3 investments return 10-100x+ (fund returners)

The entire fund's performance depends on the top 1-3 investments. A single company returning 50x can turn a mediocre fund into a top-quartile performer. This is why VC is structurally different from other forms of investing.

What This Means for Founders

VCs will push for maximum growth. A company growing 30% per year toward a 200 million dollar exit is a good business but not a fund returner. VCs need 100% or higher annual growth toward billion-dollar outcomes. If your ambition is a 50-100 million dollar exit, you and your VC are misaligned.

VCs will push against early exits. A 100 million dollar acquisition offer on a 10 million dollar investment (10x) is a life-changing outcome for founders. For the VC, it returns 20 million dollars to a 200 million dollar fund - meaningful but not transformative. The VC's incentive is to hold and push for a larger outcome, even if the risk-adjusted expected value is lower.

VCs will double down on winners and write off losers. Follow-on investment goes to the portfolio companies showing the strongest growth, not the ones that need the most help. This feels unfair but is rational portfolio management. The winner takes most of the fund's attention.

VCs are optimizing for the fund, not your company. A VC sitting on 5 boards is allocating time and attention based on which companies are most likely to be fund returners. If your company is in the middle of the pack, you will get less support than the breakout performer. This is not personal; it is structural.

What Founders Get Wrong About Fundraising

Overvaluing Valuation

Founders fixate on getting the highest valuation. But a 50 million dollar valuation with aggressive terms (participating preferred, multiple liquidation preferences, full ratchet anti-dilution) can be worse than a 35 million dollar valuation with clean terms. The headline number matters less than the economic reality in exit scenarios.

Ignoring the Fundraising Timeline

VCs make decisions slowly. From first meeting to term sheet typically takes 4-8 weeks. Due diligence adds 2-4 weeks. Legal and closing adds 2-4 weeks. A raise that a founder expects to take 2 months often takes 4-6 months. Running out of cash during a raise is the most common way startups die.

The standard advice is to begin fundraising with at least 6-9 months of runway remaining. Starting with 3 months of runway puts founders in a position of desperation, which VCs can detect and which leads to worse terms.

Misunderstanding VC Incentives

When a VC says "we want to help you build a great company," that statement is true but incomplete. They want to help build a great company that generates a venture-scale return within the fund's timeline. Those objectives sometimes conflict with what is best for the founders, the employees, or the company's long-term health.

Understanding this does not mean viewing VCs as adversaries. It means understanding their constraints so that conversations are productive rather than frustrating.

Raising Too Much or Too Little

Raising too little means returning to fundraise sooner, which is distracting and dilutive. Raising too much at too high a valuation creates a "valuation trap" - the company must grow into the valuation or face a punishing down round.

The general guidance: raise enough for 18-24 months of runway at planned burn rate, with a buffer for things taking longer than expected. That typically means 12-18 months of "planned" spending plus 6 months of cushion.

Alternatives to Venture Capital

VC is not the only funding option and is not appropriate for every company. The major alternatives differ on dilution, growth ceiling, and the kind of company they suit:

| Funding source | Dilution | Best for | Trade-off |

|---|---|---|---|

| Traditional venture capital | High (15-25% per priced round) | Software, marketplaces, deep-tech with credible path to a billion-dollar outcome | Power-law expectations; high pressure for ten-x-plus returns |

| Revenue-based financing | None | SaaS and DTC with steady recurring revenue | Capped repayment but expensive on an APR basis |

| Bootstrapping | None | Profit-first software, services, and niche brands | Slower growth; founder concentration risk |

| Private equity growth | Medium | Profitable companies past 10 million USD ARR | Mature-business expectations, board control concentrated with PE |

| Government grants (SBIR/STTR, EU Horizon) | None | Biotech, cleantech, defense, scientific R&D | Long application cycles; sector-specific |

| Strategic / corporate VC | Medium | Companies whose distribution overlaps the strategic partner | Channel dependency on the strategic; misaligned-incentive risk |

VC is one row in this table, not the entire matrix.

Revenue-based financing (Clearco, Pipe) provides capital in exchange for a percentage of future revenue. No dilution, no board seats. Works for companies with predictable recurring revenue.

Bootstrapping means funding growth from revenue. Companies like Mailchimp (before its 12 billion dollar acquisition), Basecamp, and Zoho built large businesses without VC. Bootstrapping preserves full ownership but limits growth speed.

Private equity growth capital (distinct from VC) invests in established, profitable companies. PE firms expect consistent returns, not moonshots. Appropriate for companies with 10 million dollars or more in annual revenue and positive margins.

Government grants and R&D tax credits provide non-dilutive funding for specific sectors (biotech, cleantech, defense tech). The SBIR/STTR programs in the US distribute billions annually.

Strategic investors (corporate venture capital from companies like Google Ventures, Salesforce Ventures, Intel Capital) invest for both financial returns and strategic value. They can provide distribution and partnership advantages that financial VCs cannot.

The State of VC in 2026

The VC industry is in a period of recalibration after the 2021-2022 bubble. Several structural shifts are worth noting.

Fundraising has slowed. LP commitments to VC declined significantly in 2023-2024 as interest rates rose and public market exits dried up. Smaller and newer funds are finding it harder to raise. Established franchises (a16z, Sequoia, Benchmark) continue raising easily.

AI is absorbing most new investment. AI-related companies are receiving a disproportionate share of available VC funding - by some estimates, over 50% of Series A+ rounds in 2025-2026. This creates opportunity for AI companies but means non-AI startups face a tighter funding environment.

Valuations have partially corrected. After the 2021 peak, early-stage valuations fell 30-50% and have partially recovered. Late-stage valuations remain compressed because public market comparables have not recovered to 2021 levels.

Secondary markets are growing. Platforms like Forge, Carta, and EquityZen allow early investors and employees to sell shares before an IPO. This provides liquidity earlier in the fund lifecycle but complicates cap table management.

Key Takeaways

- VC funds are 10-year vehicles funded by institutional LPs, and the contractual obligation to return capital within that timeframe drives every VC decision about growth, exits, and follow-on investment.

- The 2-and-20 fee structure creates dual incentives - management fees reward larger funds regardless of performance, while carry rewards big winners. Understanding this explains VC behavior.

- Power law returns mean 1-3 investments drive fund performance, which is why VCs push for massive outcomes even when smaller exits would serve founders well.

- Term sheet economics matter more than headline valuation - liquidation preferences, anti-dilution provisions, and board composition determine who gets what in realistic exit scenarios.

- VC is appropriate for a narrow set of companies pursuing very large markets with capital-intensive growth strategies. Most businesses are better served by alternative funding models.

Frequently Asked Questions

How much equity do founders typically give up per funding round?

At seed stage, founders typically sell 10-20% of the company. At Series A, another 15-25%. By Series C, founders have typically sold 50-60% of the company in aggregate. However, dilution depends on valuation, the amount raised, and the terms. A founder who raises efficiently at higher valuations can retain more ownership. The key metric is not the percentage sold in any single round but the total dilution across all rounds relative to the exit value.

What is the difference between a seed round and a Series A?

A seed round typically raises 1-5 million dollars at a pre-money valuation of 5-20 million dollars, used to build an initial product and find early customers. A Series A typically raises 8-25 million dollars at a pre-money valuation of 30-80 million dollars, used to scale a product that has demonstrated product-market fit. The key difference is the evidence required - seed investors bet on the team and market, while Series A investors want measurable traction (revenue growth, retention, unit economics).

Can a startup return VC money if the partnership is not working?

Legally, the invested capital belongs to the company, not the founder. Returning it requires board approval and is extremely rare. The practical reality is that if the investor-founder relationship breaks down, the most common resolution is replacing the board member (if contractually possible), finding a secondary buyer for the investor's shares, or in extreme cases, restructuring the company. The best prevention is thorough diligence on investors before accepting their money - talk to founders they have backed before, especially founders of companies that did not succeed.

How do VCs evaluate companies they cannot yet value with traditional metrics?

At the earliest stages, VCs use heuristic frameworks rather than financial models. They assess team quality (relevant experience, technical depth, ability to recruit), market timing (why this opportunity exists now), and early signals of demand (waitlists, letters of intent, organic user growth). Comparable transactions (what similar companies raised at similar stages) provide valuation anchors. As companies mature, VCs shift to revenue-based metrics: annual recurring revenue (ARR), growth rate, net revenue retention, and unit economics.

What happens to my VC investment if the startup goes bankrupt?

In a liquidation, assets are distributed in order of seniority: secured creditors first, then unsecured creditors, then preferred shareholders (VCs), then common shareholders (founders and employees). In practice, most failed startups have few assets remaining. VCs typically write the investment down to zero. Founders lose their equity but are not personally liable for the company's debts (unless they have signed personal guarantees, which is rare in VC-backed companies). The remaining cash, if any, goes to pay off obligations in order of priority.

Is venture capital appropriate for fintech companies specifically?

Fintech is one of the most VC-funded sectors, but the capital requirements and regulatory complexity of fintech create unique dynamics. Fintech companies often need more capital than typical software startups because of regulatory compliance costs, banking partner fees, and capital reserves for lending products. The regulatory moat also creates defensibility that VCs value. However, the extended timeline to profitability in fintech (many companies spend 3-5 years before reaching breakeven) means VCs need to be comfortable with longer J-curves on individual investments.

Internal Link Suggestions

- How Banks Actually Make Money: The Business Model Explained - Understanding bank economics provides context for why fintech companies raise VC to compete with institutions that have structural advantages.

- How Interest Rates Actually Affect Fintech Companies - Interest rate cycles directly impact VC fundraising, startup valuations, and the availability of capital.

- How Fintech Startups Get Licensed: A Country-by-Country Guide - The licensing costs and timelines discussed here are a major factor in fintech capital requirements.

- Top 50 Fintech Companies to Work For in 2026 - Many of the companies on this list are VC-backed, and understanding fund dynamics helps evaluate their stability and trajectory.

Related Articles

The Consortium Stablecoin: Why the Card Networks Are Funding Their Own Disruption

Visa, Mastercard, and Stripe are backing an open stablecoin consortium. The playbook is older than it looks: own the new rail's governance before it owns you.

Merchant of Record vs Payment Facilitator: Who Holds the Risk in Your Payment Stack

The four payment models compared: who holds tax, chargeback, and compliance liability as merchant of record, payfac, marketplace, or processor, and which fits.

Interchange Fees Explained: Who Really Pays for Card Payments

What interchange fees are, who pays whom in the four-party model, why rates vary, what regulation changed, and how merchants realistically cut card costs.