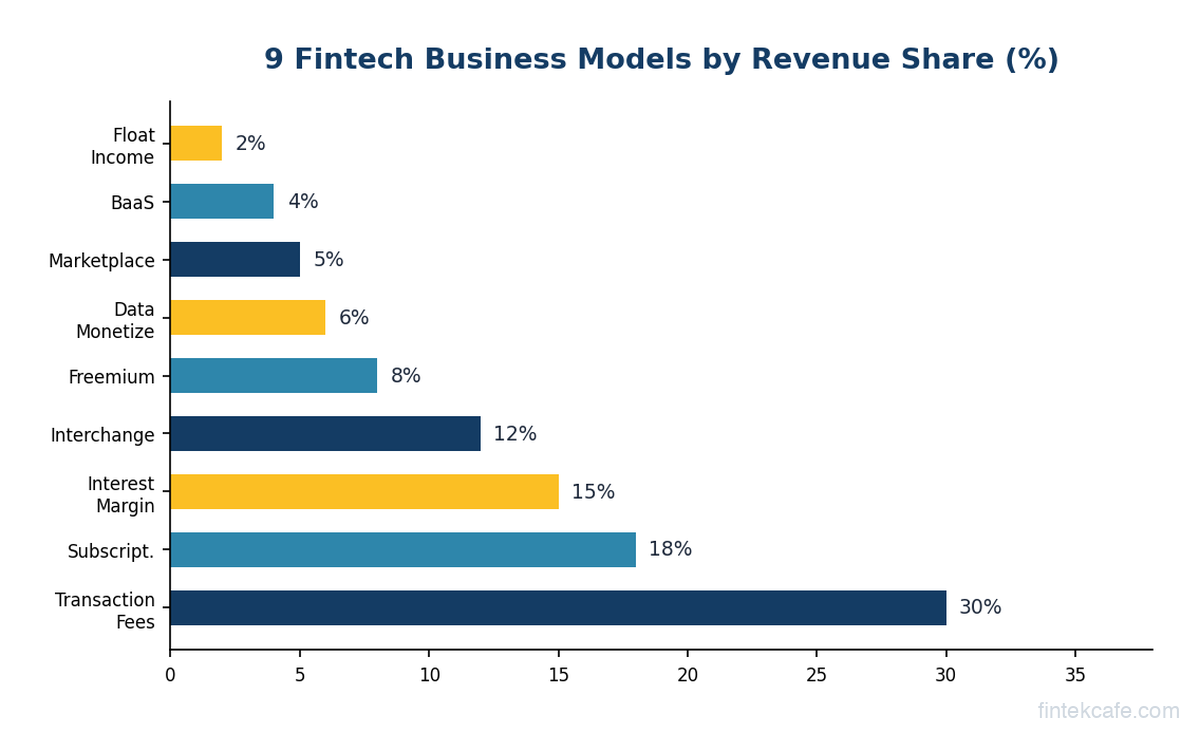

How Fintech Companies Make Money: 9 Business Models Explained

Robinhood offers "free" stock trading. Venmo lets you send money to friends at no cost. Chime doesn't charge monthly fees. Cash App gives you a debit card for nothing.

So how do these companies generate billions in revenue?

The answer is that "free" is never free. Every fintech company has a monetization engine, and most use several at once. The business model is just less visible than a traditional bank charging you $12/month for a checking account.

Understanding how fintechs make money matters whether you're evaluating a company as an investor, building a fintech product, or just trying to figure out what a company's real incentives are. The business model tells you what the company actually optimizes for, and that tells you everything about how it will behave.

Here are the nine models that power the fintech industry.

1. Transaction Fees and Interchange

How it works: Every time a customer uses a debit or credit card, the merchant pays a fee (typically 1.5-3.5% of the transaction). This fee gets split among several parties: the card network (Visa/Mastercard), the issuing bank, and the acquiring bank or processor. Fintechs insert themselves into this chain and take a cut.

Who does this: Stripe, Square (Block), Adyen, Toast, PayPal

Real numbers: Stripe charges merchants 2.9% + $0.30 per online transaction. On that 2.9%, Stripe keeps roughly 0.5-1.0% after paying interchange to the issuing bank and assessment fees to Visa/Mastercard. That sounds thin, but Stripe processed over $1 trillion in total payment volume in 2023. Even a small margin on a trillion dollars produces massive revenue.

Square takes a similar approach on the merchant side. Its standard rate of 2.6% + $0.10 per in-person transaction funds the entire Cash App and Square ecosystem.

The key insight: Transaction fee businesses are volume games. Margins per transaction are razor-thin (often under 1%), but the model scales beautifully because the cost of processing each additional transaction is negligible. The challenge is that you need enormous volume to build a big business, which is why payment companies aggressively pursue growth.

On the other side, Chime and Cash App earn interchange revenue from the card-issuing side. When a Chime customer swipes their debit card, the merchant's payment goes through the card network, and Chime (as the card issuer's program manager) earns a portion of the interchange fee. Chime's entire business model is built on this: offer free banking, get customers to use the Chime debit card for everyday purchases, collect interchange on every swipe. This reportedly generates over $1 billion in annual revenue.

2. Net Interest Margin (The Bank Model)

How it works: Take deposits (paying customers a low interest rate or nothing), lend that money out (charging borrowers a higher rate), and keep the difference. This is the oldest business model in finance, and fintechs have adopted it enthusiastically.

Who does this: SoFi, LendingClub, Marcus (Goldman Sachs), Monzo, Revolut

Real numbers: SoFi has been aggressively building its banking business since receiving its national bank charter in 2022. The company takes deposits (offering competitive APYs to attract customers) and lends that money as personal loans and student loan refinancing. In Q3 2024, SoFi's lending segment generated $396 million in revenue, with net interest margin around 5.6%. That's the spread between what they pay depositors and what they charge borrowers.

LendingClub, which acquired Radius Bank in 2021, made a similar pivot. Instead of just connecting borrowers with investors (its original marketplace model), LendingClub now holds loans on its own balance sheet, funded by deposits. This dramatically improved margins.

The key insight: Net interest margin is the most predictable and durable revenue model in finance. It's also capital-intensive: you need deposits to fund loans, and you need robust credit underwriting to avoid losses. Fintechs that obtain bank charters (SoFi, LendingClub, Varo) gain a massive advantage because they can use FDIC-insured deposits as cheap funding. Those without charters must borrow at higher rates from capital markets, compressing their margins.

3. SaaS Subscriptions

How it works: Charge businesses a monthly or annual fee for software tools. Unlike transaction fees, SaaS revenue is predictable and isn't tied to payment volume.

Who does this: Bill.com, nCino, Blend, Plaid (partially), Bloomberg Terminal

Real numbers: Bill.com charges businesses $45-65/month per user for its accounts payable and receivable automation platform. The company also earns transaction fees when customers pay bills through the platform. This dual model (subscription + transaction fees) produced over $1.2 billion in revenue for fiscal year 2024.

nCino provides cloud banking software to financial institutions. Banks pay annual subscription fees for nCino's loan origination, account opening, and compliance tools. Revenue in FY2024 was approximately $490 million, almost entirely subscription-based.

The Bloomberg Terminal is the granddaddy of fintech SaaS. At roughly $24,000 per user per year, with an estimated 325,000+ subscribers, Bloomberg's terminal business generates approximately $8 billion in annual revenue. It's one of the most profitable products in financial technology history.

![]()

The key insight: SaaS models have the highest margins in fintech (70-85% gross margins), which is why public market investors value them more highly per dollar of revenue. The trade-off is that SaaS businesses in finance require deep domain expertise and long sales cycles to enterprise customers. You can't growth-hack your way into a bank's software stack.

4. Marketplace and Platform Fees

How it works: Build a platform that connects two sides of a market (borrowers and lenders, buyers and sellers, companies and service providers) and take a percentage of each transaction.

Who does this: Robinhood, Coinbase, LendingClub (originally), Funding Circle, Upstart

Real numbers: Coinbase charges trading fees ranging from 0.5% to 4.5% depending on the transaction type and size. In a good crypto market, this produces enormous revenue: Coinbase generated $3.1 billion in transaction revenue in 2021 during the crypto boom. In a down market, revenue collapses: transaction revenue dropped to $1.4 billion in 2023. The volatility of marketplace models tied to speculative assets is extreme.

Upstart operates a lending marketplace that connects borrowers with banks and credit unions. Upstart uses AI to assess creditworthiness, and banks pay Upstart a fee (typically 3-5% of the loan amount) for each loan originated through the platform. The model is capital-light (Upstart doesn't fund the loans), but revenue depends on loan volume, which is sensitive to interest rates and credit conditions.

The key insight: Marketplace models are capital-light and can scale rapidly, but they're vulnerable to volume fluctuations. When transaction volumes drop (as they did for crypto exchanges in 2022), revenue falls proportionally. Successful marketplace fintechs diversify into adjacent revenue streams: Coinbase has expanded into staking, custody, and its Base blockchain. Robinhood now earns more from net interest on customer cash than from trading.

5. Payment for Order Flow (PFOF)

How it works: When a customer places a stock trade on a platform like Robinhood, the order isn't sent directly to a stock exchange. Instead, it's routed to a market maker (like Citadel Securities or Virtu Financial) who executes the trade. The market maker pays the platform for the right to fill those orders, because having a large flow of orders allows the market maker to profit from tiny price differences.

Who does this: Robinhood, Webull, many zero-commission brokers

Real numbers: Robinhood earned $246 million in PFOF revenue in Q3 2024. This made up a meaningful portion of total revenue, though the company has been diversifying. PFOF from options trading is significantly more lucrative per contract than equity trading, which is one reason Robinhood actively promotes options trading on its platform.

The key insight: PFOF is controversial. Critics argue it creates a conflict of interest: the platform is incentivized to encourage more trading (especially options trading) rather than what's best for the customer. The SEC considered banning PFOF in 2022-2023 but ultimately implemented new rules around execution quality instead. For now, PFOF remains legal in the US but is banned in the UK, Canada, and Australia. Regulatory risk is the biggest threat to this model.

6. Data Monetization and API Access

How it works: Aggregate financial data and sell access to it, either as raw data feeds, analytics, or API connections.

Who does this: Plaid, Envestnet Yodlee, MX, Experian, Equifax, TransUnion

Real numbers: Plaid connects fintech applications to users' bank accounts. When you link your bank account to Venmo, Robinhood, or Coinbase, Plaid is likely the connection layer. Plaid charges fintech companies per API call or per connected account: estimates suggest $0.15-$1.50 per bank account verification and ongoing fees for maintained connections. With connections to roughly 12,000 financial institutions and integration with thousands of fintech apps, Plaid reportedly generates over $500 million in annual revenue.

The credit bureaus (Experian, Equifax, TransUnion) are the original fintech data businesses. Experian's revenue exceeds $7 billion annually, with a significant portion coming from selling credit data to lenders, insurers, and other businesses that need to assess consumer risk.

The key insight: Data businesses in finance are extremely sticky. Once a fintech integrates Plaid's API, switching to a competitor means re-authenticating millions of user connections. Once a lender builds credit models on Experian data, switching bureaus requires rebuilding those models. This stickiness creates durable competitive advantages and supports premium pricing. The risk is regulatory: as open banking regulations expand (PSD2 in Europe, CFPB Section 1033 in the US), some data aggregation that companies currently charge for may become free or commoditized.

7. Freemium and Premium Tiers

How it works: Offer a basic product for free to attract users, then charge for premium features. The free tier serves as a customer acquisition channel for the paid product.

Who does this: Revolut, Cash App, Venmo, Monzo, N26

Real numbers: Revolut offers a free account with basic features (currency exchange up to a limit, basic card, budgeting). Premium tiers range from £7/month (Plus) to £13/month (Premium) to £34/month (Metal). Premium perks include higher exchange limits, travel insurance, airport lounge access, crypto cashback, and priority support. Revolut reportedly has over 40 million customers, with a meaningful percentage on paid plans. The paid subscription revenue, combined with interchange and other fees, helped Revolut reach profitability in 2024.

Cash App follows a different version of freemium. The basic peer-to-peer transfer is free, but Cash App charges for instant transfers to a bank account (1.5% fee), Bitcoin trading (spread markup), and Cash App Borrow (lending). The "free" P2P transfer hooks users into the ecosystem, and the premium services monetize them.

The key insight: Freemium works in fintech because financial products have high switching costs once a customer is active. If your paycheck goes into your Chime account or your friends all use Venmo, you're unlikely to switch just to save a few dollars. The challenge is conversion rate: most freemium fintechs convert only 3-8% of free users to paying customers. You need an enormous free base to generate meaningful premium revenue.

8. Foreign Exchange Spread

How it works: When a customer converts one currency to another (sending money abroad, spending in a foreign currency, receiving international payments), the fintech applies a markup to the mid-market exchange rate. The difference between the rate the customer gets and the actual market rate is the FX spread, and it's pure revenue.

Who does this: Wise (TransferWise), Revolut, OFX, Remitly, Western Union, PayPal

Real numbers: Wise is the most transparent company in this space. It charges 0.35-1.5% depending on the currency corridor (USD to EUR is cheap; USD to Nigerian Naira is more expensive because the underlying market is less liquid). Even at these relatively low rates, Wise generated over £1 billion in revenue in fiscal year 2024. The company processes over $100 billion in annual volume.

Compare that to a traditional bank, which might charge 2-4% on international transfers (often buried in an opaque exchange rate rather than shown as a fee). PayPal's FX markup is typically 3-4% on top of its transaction fees. The gap between Wise's 0.5% and a bank's 3% on a $10,000 transfer is $250. For businesses moving millions, the savings are transformative.

The key insight: FX spread is one of the highest-margin revenue streams in fintech. Currency conversion costs virtually nothing at scale (the actual cost of executing an FX trade on wholesale markets is tiny), so most of the spread is gross profit. The business risk is competition: as more companies enter international payments and open banking makes cross-border transfers easier, FX spreads are compressing. Wise has been proactively lowering its fees to maintain competitive advantage, accepting lower margins per transaction in exchange for higher volume.

9. Lending Spread and Origination Fees

How it works: Lend money at a higher rate than your cost of capital and keep the difference. Alternatively (or additionally), charge an upfront origination fee when a loan is issued.

Who does this: Affirm, Klarna, SoFi, LendingClub, Upstart, Kabbage (now part of Amex)

Real numbers: Affirm, the buy-now-pay-later (BNPL) company, generates revenue from two sources: merchants pay Affirm a fee (typically 5-8% of the transaction) for offering installment options at checkout, and consumers who choose longer-term financing pay interest. In fiscal Q1 2025, Affirm generated $698 million in revenue. The merchant fee portion is particularly interesting because the merchant is essentially paying Affirm to increase conversion rates at checkout, with the consumer paying nothing extra on short-term plans.

Klarna operates similarly but has expanded into advertising (Klarna shows targeted ads to its users), subscription services, and even a price comparison shopping tool. The BNPL model alone wasn't enough; diversification was necessary to reach profitability.

The key insight: Lending is the most profitable fintech business model when things go well and the most dangerous when they don't. A 1% increase in default rates can wipe out an entire year of margin. The 2022-2023 interest rate cycle proved this: several BNPL and lending fintechs saw losses spike as consumers faced higher costs across the economy. The companies that survived (Affirm, Klarna) did so by tightening underwriting and reducing approval rates, trading growth for credit quality. Lending fintechs that don't have strong risk management are ticking time bombs.

How Most Fintechs Actually Work: The Revenue Stack

In practice, no major fintech relies on a single revenue model. The most successful companies stack multiple models together.

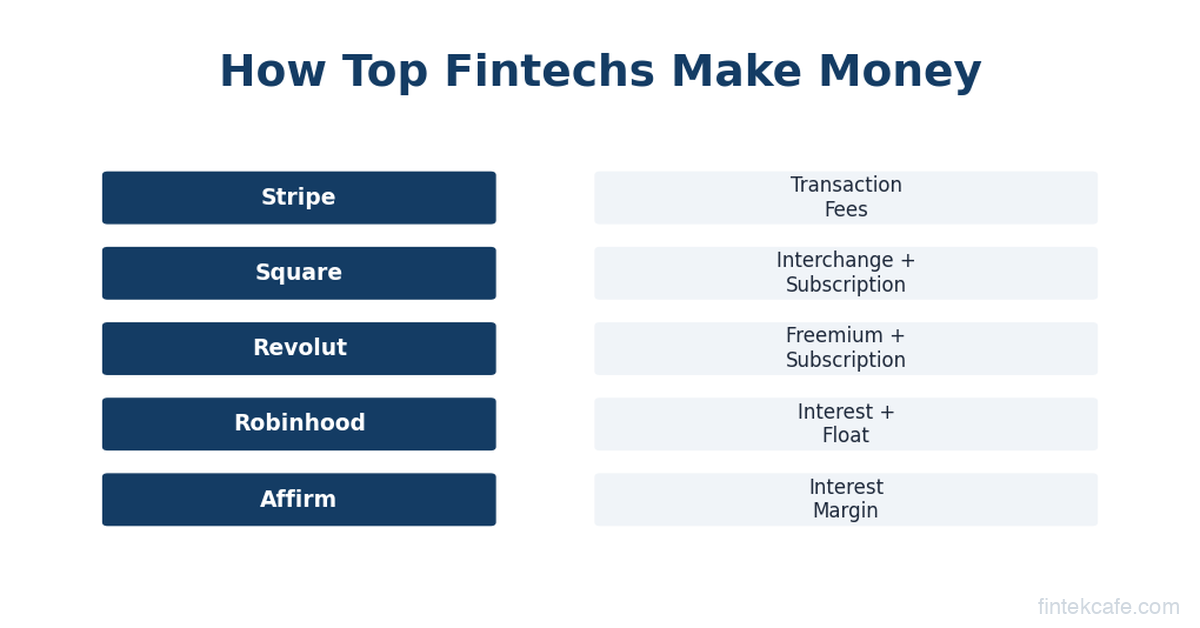

Robinhood's stack: PFOF + net interest on cash + Gold subscription ($5/month) + margin lending + crypto spread. Net interest has quietly become Robinhood's largest revenue source, surpassing PFOF.

SoFi's stack: Net interest margin on loans + interchange from debit cards + SaaS fees (Galileo/Technisys platforms) + referral fees on investment products.

PayPal's stack: Transaction fees (merchant processing) + FX spread (international payments) + Venmo monetization (debit card interchange, Pay with Venmo) + lending (PayPal Working Capital, Pay Later).

Block's (Square) stack: Seller transaction fees + Cash App interchange + Bitcoin trading spread + Afterpay BNPL merchant fees + Square Loans.

The multi-model approach is both a strength and a necessity. Transaction fees alone produce thin margins. Lending alone is too cyclical. SaaS alone grows too slowly. By combining models, fintechs can diversify revenue, improve unit economics per customer, and build more defensible businesses.

The Hidden Revenue: Float and Interest on Customer Funds

There's one more revenue source that deserves attention because it's rarely discussed openly: interest earned on customer funds.

When customers hold money in a fintech account (Venmo balance, Cash App balance, Robinhood uninvested cash), the fintech can invest those funds in low-risk, interest-bearing assets. In a high-interest-rate environment, this produces significant revenue.

Robinhood earned over $800 million in net interest revenue in the first three quarters of 2024, much of it from interest on customer cash and margin balances. PayPal holds roughly $35 billion in customer funds at any given time. Even at a conservative 4% yield, that's $1.4 billion in annual interest income.

This revenue is essentially free money. It costs nothing to earn, requires no additional product development, and scales automatically with customer balances. It's also rate-sensitive: when interest rates drop, this revenue stream shrinks.

Key Takeaways

- No fintech offers anything "for free." Every company has a monetization engine, whether it's interchange fees (Chime), PFOF (Robinhood), FX spreads (Wise), or merchant fees (Affirm).

- Transaction fees and interchange are the most common fintech business model, but they require enormous volume to produce meaningful revenue because per-transaction margins are thin (often under 1%).

- Net interest margin (the bank model) is the most durable and predictable revenue stream. Fintechs with bank charters (SoFi, LendingClub) have a structural cost-of-capital advantage.

- The most successful fintechs stack multiple revenue models. Robinhood combines PFOF, net interest, subscriptions, and crypto spread. SoFi combines lending, interchange, and SaaS.

- Understanding a fintech's business model tells you what it actually optimizes for. If a company earns most of its revenue from options PFOF, it will promote options trading. If it earns from interchange, it will push debit card usage. Follow the money.

Frequently Asked Questions

How does Robinhood make money if trading is free?

Robinhood earns revenue from payment for order flow (routing trades to market makers who pay for the order flow), net interest on customer cash balances and margin loans, its Gold subscription ($5/month for premium features), and spreads on cryptocurrency trading. Net interest has become its largest revenue source, generating over $800 million in the first three quarters of 2024.

What's the most profitable fintech business model?

SaaS subscriptions have the highest gross margins (70-85%), followed by data monetization and FX spread. Lending produces the highest absolute revenue per customer but carries credit risk. Net interest margin is the most consistent model for large-scale fintechs. The "best" model depends on your market, scale, and risk appetite.

Why do fintechs offer free accounts?

Free accounts are a customer acquisition strategy. The fintech makes money through other means: interchange fees when you use the debit card, interest on your account balance, premium subscription upsells, and cross-selling lending or investment products. The free account gets you in the door; the ancillary products generate the revenue.

How do BNPL companies like Affirm and Klarna make money?

BNPL companies earn merchant fees (5-8% of the transaction, paid by the retailer for offering installment options) and interest on longer-term consumer financing. Merchants pay because BNPL increases conversion rates and average order values. Consumers pay nothing on short-term "Pay in 4" plans but pay interest on longer-term loans.

For a deeper analysis of fintech unit economics and competitive dynamics, check out our Pro articles with exclusive research and executive-level analysis.

Related Articles

Open Banking Failed Its Promise — Here's What Actually Works

Open Banking promised a revolution. Adoption is low and APIs are fragmented. But the real winners are emerging in unexpected places.

How Central Bank Digital Currencies Will Change Finance

What are CBDCs and how will they change banking? A complete guide to central bank digital currencies, from China's digital yuan to the EU's digital euro.

What Is Embedded Finance? How Non-Banks Are Becoming Banks

What is embedded finance and why are non-banks offering financial services? A complete guide to embedded payments, lending, insurance, and banking as a service.