How Central Bank Digital Currencies Will Change Finance

In October 2022, a man in Shenzhen, China, walked into a 7-Eleven, bought a bottle of water, and paid by tapping his phone. Nothing unusual — except the money wasn't in a bank account. It wasn't cryptocurrency. It wasn't even a payment app balance. The money was a digital yuan, issued directly by the People's Bank of China, stored in a government wallet app on his phone. No bank needed. No Alipay. No WeChat Pay.

By early 2026, over 260 million Chinese citizens have digital yuan wallets. The European Central Bank is building the digital euro for a 2027-2028 pilot. Brazil's Drex platform is in advanced testing. India's digital rupee is live in limited deployment. The Bank of England has published its design principles for a digital pound.

Central bank digital currencies — CBDCs — are the most consequential development in money since the creation of the Federal Reserve in 1913. They will reshape how payments work, how monetary policy is transmitted, how cross-border transfers settle, and what role commercial banks play in the financial system. Yet most business leaders have only a vague sense of what CBDCs are or why they matter.

This guide explains CBDCs in plain terms: what they are, how they work, which countries are building them, what changes for your business, and what you should be doing now to prepare.

What Is a CBDC?

A central bank digital currency is digital money issued directly by a country's central bank. It's legal tender — just like physical cash — but exists only in digital form.

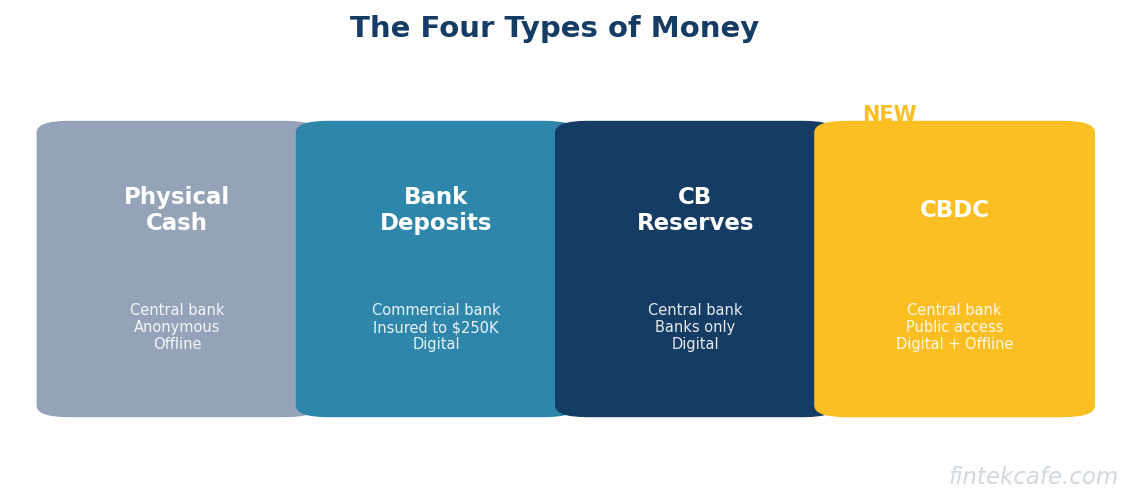

To understand why this matters, you need to understand the difference between the three types of money in circulation today:

1. Physical Cash

Banknotes and coins, issued by the central bank. When you hold a $20 bill, you hold a direct liability of the Federal Reserve. No bank sits between you and the central bank. Cash is anonymous, works offline, and settles instantly.

2. Commercial Bank Deposits

The money in your bank account. When you have $5,000 at JPMorgan Chase, you don't actually "have" $5,000 — you have a promise from JPMorgan to pay you $5,000 on demand. Your money is a liability of the commercial bank, not the central bank. It's protected by FDIC insurance (up to $250,000), but it's fundamentally a claim on a private institution.

3. Central Bank Reserves

Digital money that banks hold at the central bank. When JPMorgan settles a transaction with Bank of America, they move central bank reserves between their accounts at the Fed. Ordinary people and businesses can't access these accounts.

A CBDC creates a fourth category: digital money issued by the central bank that ordinary people and businesses can hold directly. It combines the direct central bank backing of physical cash with the digital convenience of bank deposits.

Think of it this way: a CBDC is a digital $20 bill. It's issued by the central bank, it's legal tender, it settles instantly — but it lives on your phone instead of in your wallet.

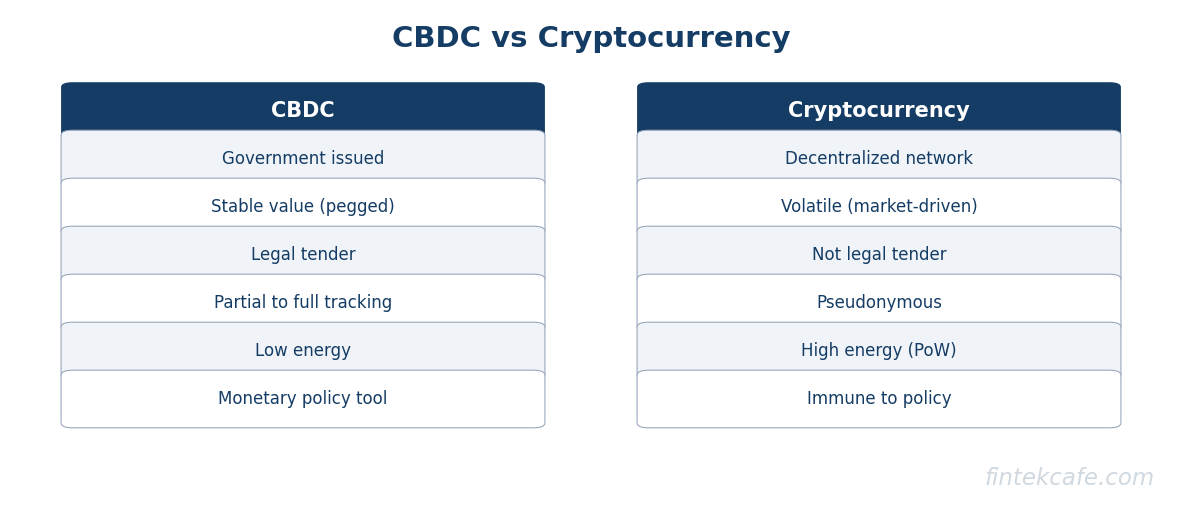

How CBDCs Differ from Cryptocurrency

CBDCs and cryptocurrencies are both digital money, but they have almost nothing else in common.

| Feature | CBDC | Cryptocurrency (Bitcoin, Ethereum) |

|---|---|---|

| Issuer | Central bank (government) | Decentralized network (no issuer) |

| Value stability | Stable (pegged to national currency) | Volatile (market-determined) |

| Legal tender | Yes | No (in most jurisdictions) |

| Privacy | Varies by design (partial to full tracking) | Pseudonymous to anonymous |

| Energy consumption | Low (centralized validation) | High for proof-of-work (Bitcoin) |

| Monetary policy | Tool for central bank policy | Immune to central bank policy |

| Governance | Government-controlled | Community/protocol-governed |

The simplest distinction: cryptocurrency was invented to bypass central banks. CBDCs are invented by central banks to maintain control in an increasingly digital economy.

CBDCs are not "government Bitcoin." They're digital cash — controlled, trackable, and designed to work within the existing financial system, not replace it.

Why Are Central Banks Building CBDCs Now?

Four forces are driving central banks to develop digital currencies simultaneously.

1. Cash Is Disappearing

In Sweden, cash transactions account for less than 8% of all payments, down from 40% a decade ago. In the UK, cash use dropped to 14% of transactions in 2025. South Korea, Norway, and the Netherlands are following the same trajectory.

As cash disappears, citizens lose access to the only form of money that is a direct claim on the central bank. If all money becomes commercial bank deposits, the entire monetary system depends on the health of private banks. CBDCs restore a public option — digital cash that works even if every commercial bank in the country fails.

2. China Is Ahead

China's digital yuan (e-CNY) is the world's most advanced CBDC. With over 260 million wallets and $250 billion in cumulative transactions, China has demonstrated that CBDCs work at scale. This has created geopolitical urgency: if cross-border trade increasingly settles in digital yuan, the dollar's reserve currency status could face a new kind of competitor.

The mBridge project — a joint CBDC platform between China, Hong Kong, Thailand, the UAE, and Saudi Arabia — is specifically designed for cross-border settlement that bypasses the US dollar and the SWIFT network. This is not theoretical. Pilot transactions have already settled.

3. Stablecoins Proved the Demand

Tether (USDT) and USDC together have a combined circulation exceeding $200 billion. These private-sector stablecoins — digital tokens pegged to the US dollar — proved that there is massive demand for programmable digital money. Central banks watched private companies create a parallel monetary system and decided they should offer the official version.

4. Financial Inclusion

Globally, 1.4 billion adults lack a bank account. Many have mobile phones. CBDCs could provide access to digital payments without requiring a bank relationship — you just need a phone and a government-issued wallet. India's digital rupee and Nigeria's eNaira were explicitly designed with financial inclusion as a primary goal.

Where CBDCs Stand Around the World

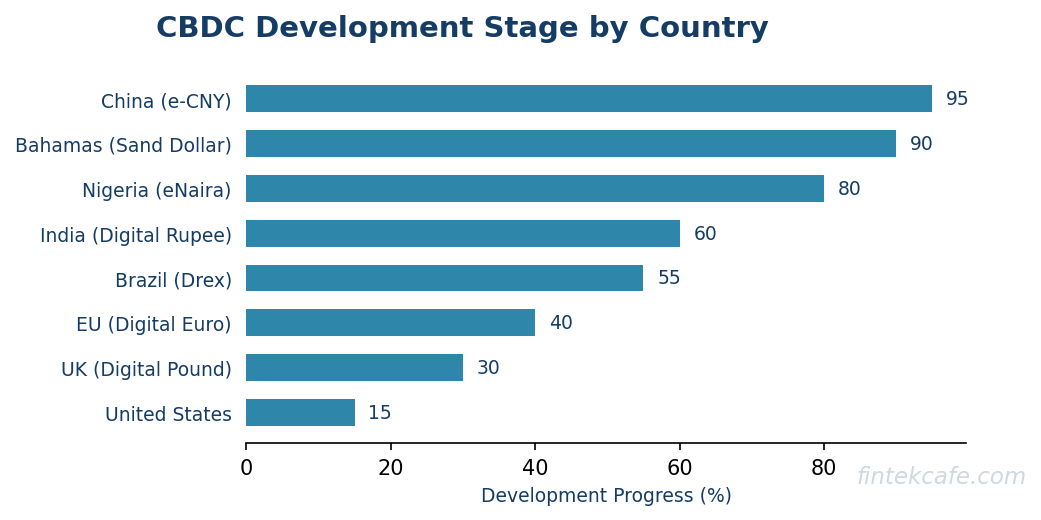

China — Digital Yuan (e-CNY): Live and Scaling

China is 3-5 years ahead of every other major economy. The digital yuan is live in 26 cities, accepted at millions of merchants, and integrated into major platforms (JD.com, Meituan, DiDi). China has distributed digital yuan through lottery-style giveaways to drive adoption — dropping ¥200 ($28) into randomly selected citizens' wallets.

Key features: dual offline payments (transactions without internet), tiered wallet anonymity (small wallets are anonymous, large wallets require ID), and programmable money (government stimulus that expires if not spent within 60 days).

The expiring stimulus is a preview of what programmable money makes possible — and what makes privacy advocates nervous.

European Union — Digital Euro: In Development

The European Central Bank is in the "preparation phase" for the digital euro, with a planned pilot in 2027-2028 and potential launch by 2028-2029. The design prioritizes privacy — the ECB has proposed that low-value transactions (under €150) would be anonymous, similar to cash.

Key design decisions: the digital euro will have holding limits (likely €3,000 per person initially) to prevent bank runs, and it will be distributed through commercial banks and payment service providers, not directly by the ECB.

The holding limit reveals the core tension: if citizens can hold money directly at the central bank, why would they keep deposits at commercial banks? The ECB is deliberately limiting the digital euro to prevent destabilizing the banking system it's built on.

United States — Researching, Not Committing

The Federal Reserve has studied CBDC through Project Hamilton (with MIT) and published research papers, but has not committed to building one. The political landscape is divided: some policymakers see a US CBDC as essential for maintaining dollar dominance; others view it as government surveillance of financial transactions.

In 2024, the House passed the "CBDC Anti-Surveillance State Act," explicitly prohibiting the Fed from issuing a retail CBDC. The Senate has not passed equivalent legislation, and the executive branch's position continues to evolve.

The US is likely to be a fast follower rather than a leader — watching how other CBDCs perform before committing. But the dollar's reserve currency status means a US CBDC, if built, would immediately become the most consequential digital currency in the world.

Other Notable Programs

- India (Digital Rupee): Live pilot with 5 million users, focused on wholesale interbank settlement and retail payments.

- Brazil (Drex): Advanced pilot focused on tokenized assets and DeFi-like programmable finance on a government-controlled platform.

- United Kingdom (Digital Pound): Design phase complete, with the Bank of England and HM Treasury targeting a "mid-to-late 2020s" launch.

- Nigeria (eNaira): Launched in 2021, but adoption has been slow — less than 1% of the population uses it, despite aggressive promotion.

- Bahamas (Sand Dollar): The world's first launched CBDC (2020). Demonstrates that small, cash-dependent economies can deploy quickly.

According to the Atlantic Council's CBDC tracker, 134 countries representing 98% of global GDP are exploring a CBDC. Over 60 are in advanced development, pilot, or launch stages.

How CBDCs Will Change Commercial Banking

This is where the stakes get highest for business leaders. CBDCs have the potential to restructure the banking system that has operated for centuries.

The Disintermediation Risk

Today, commercial banks play an essential role: they take deposits and lend them out. Your savings fund someone else's mortgage. The spread between what the bank pays you in interest (low) and charges borrowers (higher) is the fundamental business model of banking.

If citizens can hold money directly at the central bank via a CBDC, they might move deposits out of commercial banks — especially during financial crises, when the safety of a central bank is most appealing. A modern bank run wouldn't require queuing outside a branch. It would be a tap on a phone.

This is why every CBDC design includes safeguards:

- Holding limits (€3,000 for the digital euro) prevent large-scale deposit flight.

- No interest on CBDCs makes them less attractive for savings compared to interest-bearing bank deposits.

- Distribution through banks keeps commercial banks in the loop — they provide the wallets and customer interface, even though the money is a central bank liability.

The Payments Revenue Threat

CBDCs settle instantly, with zero or near-zero transaction fees, on central bank infrastructure. If businesses can accept CBDC payments without paying the 1.5-3% card processing fees they pay today, the $100+ billion payment processing industry faces a structural challenge.

Card networks (Visa, Mastercard), payment processors (Stripe, Adyen), and acquiring banks all earn revenue from the friction in today's payment system. CBDCs reduce that friction to near zero for domestic payments.

This doesn't mean Visa disappears overnight — credit (buy now, pay later) and cross-border payments still add value. But the basic domestic debit transaction, which generates enormous aggregate revenue, could be disrupted.

For a deeper look at how payment systems work and who earns what, see the Digital Payments Masterclass.

The Data Shift

Banks today have detailed transaction data — what you buy, where, how often, how much. This data powers credit scoring, fraud detection, product personalization, and revenue through data analytics.

If payments move to CBDC rails, the central bank — not commercial banks — holds the transaction data. How that data is shared, protected, and used becomes a critical policy question with enormous commercial implications.

Cross-Border Payments: The Biggest Opportunity

If domestic CBDCs are evolutionary, cross-border CBDCs are revolutionary.

Today, sending $10,000 from New York to Lagos takes 2-5 business days, passes through 3-5 intermediary banks (correspondent banking), and costs $60-105 in fees. The sender doesn't know the final exchange rate until the money arrives. The system runs on SWIFT messages and decades-old infrastructure.

CBDCs could enable cross-border transfers that settle in seconds at near-zero cost — if central banks agree to interoperate.

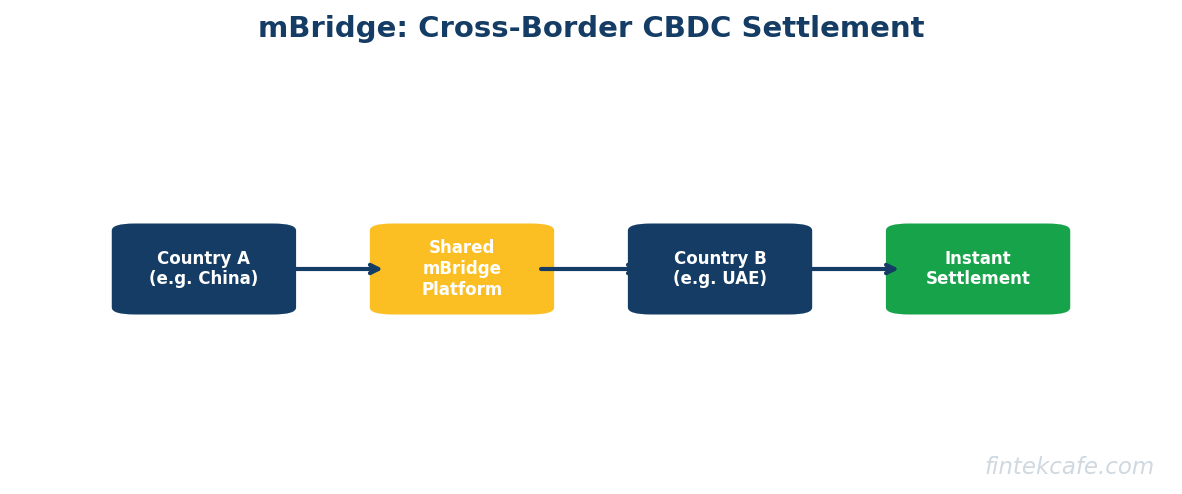

mBridge and the Challenge to Dollar Dominance

The mBridge project connects the central banks of China, Hong Kong, Thailand, the UAE, and Saudi Arabia on a shared CBDC platform. Pilot transactions have settled in seconds — China paying Thailand in digital yuan-baht, UAE paying China in digital dirham-yuan — without using the US dollar as an intermediary and without routing through SWIFT.

This is significant. The US dollar's power as a reserve currency depends partly on its role in cross-border trade settlement. If major commodity exporters (Saudi Arabia, UAE) can settle trade in CBDCs without touching dollars, the structural demand for dollars decreases.

Project Nexus (BIS)

The Bank for International Settlements' Project Nexus takes a different approach: connecting existing domestic fast payment systems (India's UPI, Brazil's PIX, Malaysia's DuitNow, etc.) rather than creating a new CBDC-specific network. This is more pragmatic and can work with or without CBDCs.

What This Means for Businesses

If you operate across borders, CBDC interoperability could dramatically reduce your payment costs and settlement times. But the timeline is uncertain — full interoperability requires central bank agreements, technical standards, and regulatory frameworks that don't yet exist. Plan for 2028-2032 for meaningful cross-border CBDC infrastructure.

Privacy: The Central Concern

Every CBDC discussion eventually confronts the same question: how much should the government know about what you buy?

The Surveillance Argument

Physical cash is anonymous. A CBDC, by design, runs on digital infrastructure that can record every transaction. A government with access to CBDC transaction data would know: what every citizen buys, where they shop, who they send money to, and when. This is the most comprehensive financial surveillance capability ever created.

China's digital yuan already demonstrates this capability. The People's Bank of China has described the system as providing "controllable anonymity" — small transactions are anonymous, but the central bank can see everything if it chooses to investigate.

The Privacy Safeguards

Some CBDC designs attempt to preserve cash-like privacy:

- Tiered anonymity: The ECB's digital euro proposal allows anonymous transactions below €150, with identity verification required for larger amounts.

- Zero-knowledge proofs: Cryptographic techniques that let the system verify a transaction is valid without revealing the transaction details. Switzerland's Project Helvetia has explored this approach.

- Offline transactions: Transactions between two devices without internet connectivity — similar to handing someone cash — are technically possible and harder to surveil.

The Realistic Assessment

No major CBDC will offer full anonymity equivalent to cash. Central banks need some level of visibility for anti-money laundering (AML), counter-terrorism financing (CTF), and sanctions enforcement. The question is where on the spectrum between "full anonymity" and "complete surveillance" each country lands.

The US political resistance to CBDCs is driven primarily by privacy concerns — and this is a legitimate debate, not a fringe position. How a society balances monetary innovation with financial privacy will define the character of its CBDC.

What Businesses Should Do Now

CBDCs are not here yet for most countries (outside China), but they're coming within 3-5 years for major economies. Here's what to do now.

1. Understand Your Payment Cost Structure

Map how much you pay in payment processing fees today — interchange, processing, gateway fees — and for which transaction types. CBDC's zero-fee model will have the biggest impact on businesses with high transaction volumes and thin margins (retail, groceries, quick-service restaurants).

2. Monitor Your Key Markets

If you operate in the EU, the digital euro timeline (2027-2028 pilot, 2028-2029 launch) is your planning horizon. If you do business with China, digital yuan acceptance may already be relevant for suppliers or customers. Track the CBDC programs in every market where you have significant revenue.

3. Talk to Your Treasury Team

CBDCs will add a new asset type to corporate treasury management — digital central bank money that is neither a bank deposit nor cash. Your treasury team should understand the implications for cash management, liquidity, and counterparty risk. Money held as CBDC has zero credit risk (it's a central bank liability), which changes the calculus for overnight cash positioning.

4. Assess Your Technology Readiness

CBDC acceptance will likely require point-of-sale updates, payment gateway integration, and accounting system modifications. Start conversations with your payment providers (Stripe, Adyen, Square) about their CBDC roadmaps. The top fintech companies are already building CBDC capabilities into their platforms.

5. Engage in the Policy Conversation

CBDC design decisions — holding limits, privacy levels, interest rates, bank intermediation — will have real business consequences. Industry associations, regulatory comment periods, and public consultations are your opportunity to influence these designs before they're locked in.

Key Takeaways

- A CBDC is digital money issued directly by the central bank — combining the safety of cash with the convenience of digital payments. It's not cryptocurrency; it's digital cash controlled by the government.

- 134 countries are exploring CBDCs. China is live with 260 million wallets. The EU targets 2027-2028 for a pilot. The US is studying but has not committed.

- CBDCs threaten commercial bank business models by enabling citizens to hold money directly at the central bank, bypassing deposit-taking banks. Holding limits and zero-interest designs are safeguards against bank runs.

- Cross-border CBDCs (mBridge) could restructure global trade settlement, reducing the dollar's intermediary role and cutting transfer times from days to seconds.

- Privacy is the defining tension. Every CBDC design balances financial surveillance capability against citizen privacy. No major CBDC will match cash's anonymity.

- Businesses should prepare now by understanding payment cost structures, monitoring CBDC timelines in key markets, and assessing technology readiness for CBDC acceptance.

FAQ

Will CBDCs replace cash?

Not immediately, and probably not completely. Every central bank developing a CBDC has stated explicitly that it will complement, not replace, physical cash. Sweden's Riksbank and the ECB have both proposed legislation guaranteeing the right to use cash alongside digital currencies. In practice, however, CBDCs will accelerate cash's decline. If digital central bank money is as safe as cash but more convenient, rational consumers will prefer it. Within a decade of launch, CBDCs will likely handle the majority of transactions that cash handles today — but physical cash will remain available for those who prefer it, especially in rural areas and for populations without smartphones.

How will CBDCs affect my business's payment costs?

If CBDCs settle on central bank rails at zero or near-zero transaction fees, the 1.5-3% you currently pay for card transactions could drop significantly for CBDC-denominated payments. The biggest savings would come from debit-equivalent transactions (everyday purchases) rather than credit transactions (where the lender's margin justifies a fee). However, payment processors will likely evolve their fee structures — charging for value-added services (fraud detection, analytics, reconciliation, cross-border conversion) rather than basic transaction processing. The net impact on your costs depends on your transaction mix, average ticket size, and how quickly CBDC adoption reaches critical mass in your markets.

Are CBDCs a threat to Bitcoin and cryptocurrency?

They serve different purposes and appeal to different users. Bitcoin's value proposition is decentralization — no government can inflate, freeze, or surveil Bitcoin transactions (in theory). A CBDC is the opposite: centralized, government-controlled, and potentially surveilled. People who hold Bitcoin because they distrust central banks will not switch to a CBDC. However, CBDCs could reduce demand for stablecoins (USDT, USDC), which are used primarily for digital payments and trading rather than as an ideological statement. If you can hold digital dollars issued by the Fed, the case for holding digital dollars issued by Tether weakens. The stablecoin market — currently over $200 billion — is the most directly threatened by CBDCs.

What happens to my money if the central bank's CBDC system goes down?

This is a legitimate concern, and it's why every CBDC design includes offline capabilities. China's digital yuan can process transactions between two devices without internet connectivity using NFC (near-field communication) — similar to tapping a contactless card. The ECB has specified offline functionality as a requirement for the digital euro. Additionally, CBDCs will coexist with existing payment systems (cards, bank transfers, cash), so a CBDC outage wouldn't paralyze the economy — you'd simply use alternative payment methods. That said, as CBDC adoption grows and cash declines, the resilience of CBDC infrastructure becomes increasingly critical. Expect central banks to invest heavily in redundancy, similar to how they protect existing payment systems like Fedwire and TARGET2.

Should I accept digital yuan if I have Chinese customers or suppliers?

If you have significant business with China, yes — at least begin exploring it. The digital yuan is accepted at millions of merchants in China, and China is actively promoting its use in cross-border trade. Accepting digital yuan can reduce your foreign exchange costs and settlement times for China-related transactions. The practical step is to ask your payment processor about digital yuan support. Major processors (Stripe, Adyen) are monitoring CBDC developments, though full integration for cross-border digital yuan is still early. For now, if you have a Chinese subsidiary or local banking relationship, discuss digital yuan acceptance with your local bank — several Chinese banks offer merchant wallet integration. For more on cross-border payment mechanics and how different rails compare, see the Digital Payments Masterclass.

Related Articles

The CFO's Guide to AI: What Finance Leaders Actually Need to Know

A practical AI guide for CFOs. ROI frameworks, budget allocation, vendor evaluation, and why finance leaders who ignore AI will be replaced by those who don't.

What Is Embedded Finance? How Non-Banks Are Becoming Banks

What is embedded finance and why are non-banks offering financial services? A complete guide to embedded payments, lending, insurance, and banking as a service.