The Anatomy of a Wire Transfer: From Initiation to Settlement

The Anatomy of a Wire Transfer: From Initiation to Settlement

A wire transfer sounds simple: you tell your bank to move money to someone else, and it moves. But between that instruction and the funds actually landing in the recipient's account, a surprising amount of infrastructure is involved.

Understanding how wires work matters if you're in finance, accounting, or fintech — and it's essential if you want to understand why wire fraud is so devastatingly effective, why reversing a wire is nearly impossible, and why some wire transfers take seconds while others take days.

What Makes a Wire Transfer Different

A wire transfer is a push payment — you initiate it, funds move, and it's done. Two properties make wires distinct from other payment types:

Irrevocability: Once a wire clears, it cannot be recalled unilaterally. Unlike an ACH transfer (which can be reversed within a window) or a credit card payment (where chargebacks exist), a completed wire requires the recipient's voluntary cooperation to reverse. The sending bank cannot force a return.

Real-time gross settlement (RTGS): Domestic wire systems settle each transaction individually and immediately — gross (one at a time, not netted) and in real-time. There's no batch processing, no end-of-day netting. The money moves now.

These two properties make wires ideal for large, time-sensitive, high-trust transactions (real estate closings, securities settlements, business acquisitions) and terrible for anything where you might need to get the money back.

Domestic Wire Systems: Fedwire vs CHIPS

In the United States, two systems handle the vast majority of domestic wire transfers.

Fedwire Funds Service

Fedwire is operated by the Federal Reserve. It's the backbone of the US dollar financial system — the final settlement layer.

Key characteristics:

- Real-time gross settlement: Each payment settles immediately and is final. If it goes through, it's done.

- Operating hours: Monday–Friday, 9:00 PM ET (previous day) to 7:00 PM ET. As of 2024, extended hours are being phased in toward a 22-hour window.

- Who can use it: Only Federal Reserve account holders — US commercial banks, thrift institutions, credit unions, foreign bank branches in the US, and government agencies. Individuals and businesses access Fedwire through their banks.

- Volume: Approximately 900,000 transactions per day, averaging ~$5 trillion in daily value. The largest-value payment system in the world by dollar amount.

- Cost: The Fed charges participating banks ~$0.82 per transaction. Banks typically charge end customers $25-35 for outgoing wires, $10-20 for incoming.

Routing numbers: Fedwire uses ABA routing numbers (the 9-digit number at the bottom of a check) to identify financial institutions. When you send a domestic wire, the routing number tells Fedwire which Fed account to credit.

CHIPS (Clearing House Interbank Payments System)

CHIPS is privately operated by The Clearing House, owned by the largest US commercial banks (JPMorgan, Bank of America, Citibank, Wells Fargo, and others).

Key characteristics:

- Multilateral netting + RTGS hybrid: CHIPS doesn't settle every transaction immediately. It queues payments and finds offsetting transactions to net them — Bank A sends $10M to Bank B while Bank B sends $8M to Bank A; CHIPS settles the net $2M rather than two $10M gross flows. This dramatically reduces the amount of Fed reserve balances needed.

- Operating hours: 9:00 AM to 5:00 PM ET, Monday–Friday.

- Who uses it: Large commercial banks directly, primarily for interbank and large-value transactions.

- Volume: ~400,000 transactions per day, but around $1.8 trillion in daily value. Fewer transactions than Fedwire but often larger individually.

Fedwire vs CHIPS: Which Is Used When?

| Factor | Fedwire | CHIPS |

|---|---|---|

| Settlement type | Real-time gross | Net settlement + RTGS |

| Operator | Federal Reserve | The Clearing House (private) |

| Access | All Fed member institutions | Large commercial banks |

| Use cases | Time-sensitive, must-clear-immediately | Large interbank flows, securities |

| Daily volume | ~$5 trillion | ~$1.8 trillion |

In practice, most wire transfers you initiate as a business or individual go through Fedwire. CHIPS is more prevalent for interbank flows and wholesale financial markets.

International Wire Transfers: The SWIFT Layer

International wires add a messaging layer — SWIFT — on top of whatever domestic rail moves the money at each end.

How International Wires Actually Work

An international wire is not a single transaction. It's a chain of SWIFT messages and corresponding ledger adjustments across a correspondent bank network.

Key concept — correspondent banking: Banks that don't have direct relationships with each other route payments through intermediary ("correspondent") banks that maintain accounts with both parties. Your bank holds a pre-funded account (nostro account) at a foreign correspondent bank in the destination country's currency.

Step-by-step — sending $10,000 USD to a UK business:

- You initiate: You provide your bank with the recipient's IBAN, the UK bank's SWIFT BIC, recipient name, and address. Your bank debits your account $10,000 + fee.

- Your US bank → US correspondent (if needed): If your regional bank doesn't have a direct SWIFT relationship with the UK, it routes through a major US bank (JPMorgan, Citi, etc.) that does.

- SWIFT MT103 message sent: The US correspondent sends an MT103 payment message to the UK bank (or UK correspondent): "Please credit £X to IBAN GB12345 at recipient's request from [sender]."

- FX conversion: Somewhere in this chain, USD converts to GBP. The rate used is typically the bank's mid-market rate minus a spread (0.5–3% markup). This is a major source of hidden cost.

- UK bank credits recipient: The final UK bank credits the recipient's account in GBP. A receiving fee may be deducted (£5-15).

Total elapsed time: same-day on gpi corridors, 1-5 days on traditional SWIFT. Total fees: $20-80+ depending on corridor and banks involved.

What Information Is Required

Sending a wire transfer requires more information than other payment types. Missing or incorrect data is the most common cause of delays and failed wires.

For domestic US wires (required):

- Recipient's full legal name (exactly as it appears at their bank)

- Recipient's bank name

- ABA routing number (9 digits)

- Recipient's account number

- Wire amount and currency

For international wires (required):

- Recipient's full legal name

- Recipient's full address

- Recipient's bank name and address

- SWIFT/BIC code (8 or 11 characters, e.g., HBUKGB4B for HSBC UK)

- IBAN (for European and many other countries — typically 15-34 characters)

- Account number or IBAN (depending on country)

- Purpose/reason for transfer (required in many jurisdictions for compliance)

- Currency and amount

Optional but often required for international:

- Intermediary bank details (SWIFT BIC, account number) if the correspondent bank is different from the receiving bank

- Sender's reference or invoice number (required by some receiving banks)

A single character error in an account number or SWIFT code can cause the wire to fail, be returned, or — worst case — credit the wrong account. Most banks validate SWIFT codes but not account numbers.

Fee Breakdown

Wire transfer fees are not always transparent. Here's every possible fee:

| Fee Type | Who Charges | Typical Range |

|---|---|---|

| Outgoing wire fee | Your bank | $25-45 domestic; $40-60 international |

| FX conversion spread | Your bank or correspondent | 0.5–3% of amount |

| Intermediary/correspondent fee | Middle banks in chain | $10-20 (deducted from wire) |

| Incoming wire fee | Recipient's bank | $10-20 |

| Tracing fee (if wire goes missing) | Your bank | $15-50 |

For small transfers ($1,000 or less), fees can exceed 5% of the amount. For large transfers ($100,000+), the percentage cost drops but total fees can still be $50-150.

Shared/OUR/BEN charge options: International wires often ask how fees should be handled:

- OUR: Sender pays all fees; recipient receives the full amount

- SHA (Shared): Each party pays their own bank's fees; intermediary fees deducted from wire amount

- BEN: Recipient pays all fees (rare, often confusing)

For B2B transactions where exact amounts matter, use OUR — you pay your bank's disclosed fee plus a fixed amount to cover intermediary and receiving fees.

Wire vs ACH vs RTP: Comparison Table

| Feature | Wire (Fedwire) | ACH | RTP (Real-Time Payments) |

|---|

| Speed | Immediate (RTGS) | 1-3 days (same-day ACH available) | < 30 seconds |

| Reversibility | No (irrevocable) | Yes (ACH return window) | No |

|---|---|---|---|

| Amount limit | No limit (Fedwire) | No standard limit (varies by bank) | $1M per transaction |

| Cost | $25-45 to send | $0.20-1.00 | Typically $0.25-1.00 |

| Availability | Business hours (Fedwire) | Business days | 24/7/365 |

| Use cases | Large, urgent, irrevocable | Payroll, recurring payments | Urgent mid-size transfers |

When to use each:

- Wire: Real estate closings, securities purchases, large B2B invoices, any transaction where immediate finality matters and amount is large

- ACH: Payroll, supplier payments, recurring subscriptions, rent — anything where a 1-3 day delay is fine

- RTP: When you need ACH's low cost but can't wait 3 days — business payments under $1M that need same-day settlement

Wire Fraud: Why It's So Effective and How It Works

Wire fraud is one of the most costly financial crimes because of the fundamental property we've discussed: wires are irrevocable. Once sent, recovery requires the recipient to voluntarily return the funds — and criminals don't do that.

Business Email Compromise (BEC)

The most common wire fraud targeting businesses. The pattern:

- Criminal compromises (or spoofs) an email account of a company's CEO, CFO, or vendor

- Sends an urgent email to the person who controls wire payments ("Accounts Payable")

- Instructs them to send a wire to a new account for a time-sensitive purpose (pending acquisition, urgent supplier payment)

- Employee, believing it's legitimate, initiates the wire

- Funds land in criminal's mule account, are immediately transferred internationally

- Discovery happens too late to recall

The FBI reports BEC caused over $2.9 billion in losses in the US in 2023 alone. The average loss per incident is over $100,000.

Why it's so hard to recover from: By the time the fraud is discovered (often hours or days later), the wire has settled and funds have moved to a second or third account in another jurisdiction. Bank recalls are possible but only succeed if the receiving bank can freeze funds before they're moved — a small window.

Real Estate Wire Fraud

Similar mechanism targeting real estate transactions. At closing, buyers wire large sums (down payments, full purchase prices). Criminals intercept email communications between buyer and title company or attorney, then substitute fraudulent wire instructions when the legitimate wiring instructions are expected.

The amount involved — often $200K-500K+ — and the timing (wired just before closing, discovered at closing when funds don't arrive) makes this particularly devastating.

Prevention: Verify wire instructions by phone call to a known number (not a number from email), not by email or text. Title companies and attorneys should have a stated policy of never sending wiring instructions by email alone.

What Happens When a Wire Goes Wrong

Despite RTGS finality, wires do occasionally fail, get delayed, or credit the wrong account. Here's how each scenario plays out.

Wire Sent to Wrong Account

If you enter the wrong account number, several outcomes are possible:

The account doesn't exist: The receiving bank rejects the wire and returns it, typically within 1-2 business days. You get your money back minus any fees.

The account exists but belongs to a stranger: The receiving bank credits the wrong account. Recovery requires the receiving bank to voluntarily debit the wrong account holder (who may not cooperate) and return funds. Your bank can send a "recall request" but has no legal authority to force the return. If the wrong recipient refuses, you may have to sue them.

Prevention: Double-check every wire instruction. Many banks now offer "payee confirmation" matching account name to account number — similar to the UK's Confirmation of Payee system. This is still not universal in the US.

Wire Is Delayed or "Missing"

Wires can appear to "go missing" — sent but not received. Common causes:

- Compliance hold: AML or sanctions screening flagged the transaction for manual review at an intermediary bank

- Missing information: Incorrect beneficiary address, missing reference, or incomplete intermediary bank details caused a hold

- Cut-off times: Wire was initiated after the receiving bank's daily cut-off

Your bank can initiate a SWIFT gpi trace to see exactly where in the chain the payment is sitting. If the wire has moved beyond your bank, your bank submits a trace request; SWIFT gpi requires all participating banks to provide status within a set timeframe.

Typical resolution: 1-3 business days for most trace issues. For truly missing wires (non-gpi corridors), 5-10 business days is not unusual.

Wire Returned

When a wire is returned, the SWIFT MT103 message is reversed with a SWIFT MT103 RETURN. The originating bank receives the funds back and credits your account — minus any fees charged along the way. Return reasons include: incorrect account details, account closed, account restricted, compliance hold, beneficiary refusal.

How Banks Detect Wire Fraud

Given the stakes, banks invest heavily in wire fraud detection — primarily through behavioral analytics and rule-based systems.

Transaction monitoring rules: Wires to new recipients, wires in excess of normal patterns, wires to high-risk jurisdictions, and wires with urgent/unusual justifications all trigger alerts.

Beneficiary warm-up requirements: Many banks require new beneficiaries to be added 24-72 hours before a wire can be sent — specifically to interrupt BEC scams where urgency is the social engineering lever.

Dual-authorization controls: For commercial accounts, banks often require two employees to approve wire transfers above a threshold. This is a key control businesses should enable.

Callback verification: Banks are increasingly required to call back customers to verify large wire instructions, particularly if the request came through digital channels. A live phone call to a known number is the single most effective BEC prevention measure.

IP and device fingerprinting: Online banking platforms monitor whether the device and network location initiating a wire matches the customer's historical patterns. An unusual IP address, especially one geolocated to a different country, triggers additional friction.

Key Takeaways

- Wire transfers are irrevocable RTGS payments — they settle immediately and cannot be recalled unilaterally once complete, making them fundamentally different from ACH or card payments.

- Two US domestic wire systems: Fedwire (Fed-operated, true RTGS, ~$5T/day) and CHIPS (private, netting + RTGS hybrid, ~$1.8T/day).

- International wires are a chain of SWIFT messages plus correspondent bank ledger adjustments — the money doesn't actually teleport, it flows through pre-funded nostro accounts.

- Full fee visibility requires knowing all four fee types: originating bank fee, FX spread, intermediary fees (deducted from wire), and receiving bank fee.

- Wire is right for: large amounts, time-sensitive transactions, situations requiring finality. ACH is better for payroll and recurring payments. RTP fills the middle ground.

- Wire fraud succeeds because wires are irrevocable — always verify wire instructions out-of-band by calling a known, pre-verified phone number before sending.

- When wires go wrong, trace requests via SWIFT gpi locate the payment in the correspondent chain; most delays resolve within 1-3 business days on gpi corridors.

Related Reading

- How Cross-Border Payments Work (And Why They're So Slow)

- SWIFT vs SEPA vs UPI: Global Payment Networks Compared

- Payment Gateway vs Payment Processor: What's the Difference?

- How Payment Networks Work: Visa, Mastercard, and the Four-Party Model (Pro)

Free Weekly Fintech Insights

FinTekCafe publishes weekly explainers on payments, banking infrastructure, and digital finance — written for people who need to actually understand how the financial system works, not just the surface-level version.

Related Articles

Open Banking Failed Its Promise — Here's What Actually Works

Open Banking promised a revolution. Adoption is low and APIs are fragmented. But the real winners are emerging in unexpected places.

How Central Bank Digital Currencies Will Change Finance

What are CBDCs and how will they change banking? A complete guide to central bank digital currencies, from China's digital yuan to the EU's digital euro.

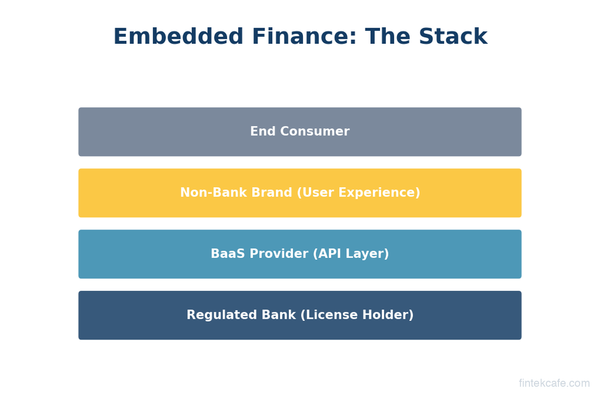

What Is Embedded Finance? How Non-Banks Are Becoming Banks

What is embedded finance and why are non-banks offering financial services? A complete guide to embedded payments, lending, insurance, and banking as a service.