SWIFT vs SEPA vs UPI: Global Payment Networks Compared

SWIFT vs SEPA vs UPI: Global Payment Networks Compared

If you've ever sent money abroad, you've encountered SWIFT. If you live in Europe, you've used SEPA without thinking about it. If you're in India, UPI is probably how you split lunch bills. These three systems — along with a growing list of national real-time networks — form the backbone of global money movement.

But what actually makes them different? When should you use each one? And why can't we just have one global payment system that works everywhere?

This guide explains how SWIFT, SEPA, and UPI work, compares them head to head, and covers the newer networks threatening to replace the old guard.

SWIFT: The World's Payment Messaging Network

Let's clear up the most common misconception right away: SWIFT does not move money. SWIFT is a messaging network — it carries instructions about money transfers between banks. The money itself moves through correspondent bank accounts and central bank systems.

What SWIFT Actually Is

SWIFT stands for the Society for Worldwide Interbank Financial Telecommunication. Founded in 1973, it's a cooperative owned by its member financial institutions. Today, over 11,000 financial institutions in 200+ countries use SWIFT to exchange payment messages.

Think of SWIFT like email for banks. When Deutsche Bank in Germany needs to send a wire transfer to Citibank in the US, it sends a SWIFT message: "Please credit account X with $Y on behalf of sender Z." Citibank receives that message and moves money in its own systems accordingly.

The actual flow of funds happens through correspondent banking — a chain of pre-existing relationships between banks that hold accounts with each other (more on this in our cross-border payments article).

How SWIFT Messages Work (MT vs MX)

SWIFT messages come in two standards:

MT (Message Type) format — The legacy standard, used since the 1970s. Structured but relatively rigid. MT103 is the standard single-customer credit transfer (the message format for most wire transfers). MT202 is for bank-to-bank transfers.

MX (ISO 20022) format — The modern standard, migrating globally through 2025. XML-based, richer data, machine-readable. ISO 20022 enables significantly more payment data (purpose of payment, invoice references, LEI codes for legal entities) and is the basis for all new payment system innovation.

The global migration from MT to MX is a major infrastructure project — trillions of dollars in daily flows moving to a new message format simultaneously.

SWIFT GPI (Global Payments Innovation)

Launched in 2017, SWIFT gpi (Global Payments Innovation) is the biggest improvement to the SWIFT network in decades. It added:

- End-to-end tracking: Like a parcel tracking number for wire transfers. Sending banks can see exactly where a payment is at every stage.

- Same-day availability: gpi payments are credited to the final beneficiary within 24 hours in most cases (previously, wires would sit in correspondent banks for days).

- Fee transparency: Banks must report fees deducted at each stage so the sender knows exactly what was charged.

- Data integrity: Payment data must be passed unaltered through the correspondent chain.

By 2024, over 50% of SWIFT cross-border payments are gpi-enabled, with more than $300 billion sent daily. The goal: making international wires as fast and traceable as a domestic bank transfer.

SWIFT's Weaknesses

- Speed: Even gpi payments can take 1-2 days for complex corridors. Non-gpi SWIFT transfers still take 2-5 days.

- Cost: Each hop in the correspondent bank chain adds fees. A $1,000 transfer can lose $20-50 in fees by the time it arrives.

- Opacity: Without gpi, recipients often don't know why a transfer is delayed or what fees were taken.

- Access: SWIFT requires a BIC (Bank Identifier Code) and is not accessible to individuals or small businesses directly.

SEPA: Europe's Unified Payment Area

SEPA — the Single Euro Payments Area — is not a company or a network in the SWIFT sense. It's a regulatory framework and a set of payment standards that makes bank transfers within Europe work as simply as domestic payments.

What SEPA Covers

SEPA covers 36 countries — the 27 EU member states plus Norway, Iceland, Liechtenstein, Switzerland, the UK (post-Brexit), Monaco, Andorra, San Marino, and Vatican City. Within this zone, any bank transfer in euros uses SEPA standards.

This means a French company paying a German supplier is treated the same as paying a domestic supplier — same forms, same bank account format (IBAN), same rules.

SEPA Payment Types

SEPA Credit Transfer (SCT) — Standard bank transfer between two IBAN accounts. Processes within one business day. Cost: €0.00 to €0.50 depending on bank. The backbone of B2B payments in Europe.

SEPA Direct Debit (SDD) — Pulls money from a payer's account with prior authorization (mandate). Used for subscriptions, utility bills, loan repayments. The European equivalent of ACH debit.

SEPA Instant Credit Transfer (SCT Inst) — Real-time (within 10 seconds), 24/7/365. Maximum amount: €100,000 per transaction (limits being increased). As of 2024, EU regulation requires all banks to offer instant payments at the same price as standard SEPA transfers.

SEPA vs SWIFT for European Payments

Here's the key distinction: if you're moving euros between two European bank accounts, SEPA is almost always used — it's cheaper, more standardized, and increasingly instant. SWIFT is typically used when you need to move non-euro currencies, or when the counterparty is outside the SEPA zone.

A UK company sending euros to France will use SEPA. A US company sending euros to France will use SWIFT to send from the US bank to a European correspondent, which then completes the final leg via SEPA.

UPI: India's Payments Revolution

India's Unified Payments Interface (UPI) is arguably the most impressive payments infrastructure built anywhere in the last decade. It went from zero to over 14 billion transactions per month in about 8 years.

What UPI Is

UPI is a real-time payment system built by the National Payments Corporation of India (NPCI) — a non-profit entity promoted by the Reserve Bank of India. Launched in 2016, it enables instant bank-to-bank transfers via mobile, 24/7, using simple identifiers like a mobile number or VPA (Virtual Payment Address, e.g., name@bank).

How UPI Works

Unlike SWIFT (which routes messages) or SEPA (which is a transfer standard), UPI is a full payment infrastructure layer:

- Payer opens any UPI-enabled app (PhonePe, Google Pay, Paytm, BHIM, or their own bank app)

- Enters recipient's UPI ID or scans a QR code

- Authorizes with PIN

- NPCI routes the request through the payer's bank and recipient's bank simultaneously

- Debit and credit happen in real-time, typically within 5-30 seconds

Every bank in India is mandated to support UPI. This is why a PhonePe user can pay a Google Pay user — interoperability is built into the system at the infrastructure level, not bolted on.

Why UPI Is Significant

Volume: 14B+ transactions per month (as of 2025). Total volume processed exceeds $2 trillion annually. More transactions happen on UPI each day than in many countries' entire banking systems per year.

Cost: Zero to near-zero transaction fees for consumers. Merchants pay up to 0.5% for certain categories, nothing for person-to-person.

Access: Any Indian with a bank account and a smartphone can use UPI. This was transformational for financial inclusion — 80% of India's adult population is now digitally transacting.

Infrastructure: UPI runs on IMPS (Immediate Payment Service), the underlying RBI-managed rails, with NPCI as the switch. It's entirely domestic but increasingly being extended cross-border.

International expansion: UPI has launched or piloted in Singapore, UAE, Bhutan, Nepal, France, Sri Lanka, Mauritius, and others. The goal is to let Indian travelers and diaspora use UPI abroad without currency conversion friction.

Head-to-Head Comparison

| Feature | SWIFT | SEPA | UPI |

|---|---|---|---|

| Primary use | International cross-border | Intra-European EUR transfers | Domestic India (+ expanding) |

| Speed | 1-5 days (gpi: same-day) | Same-day (instant: 10 sec) | Seconds (< 30 sec) |

| Cost | $20-50 (full chain) | €0-0.50 | ₹0 (consumer) |

|---|---|---|---|

| Coverage | 200+ countries, 11,000+ banks | 36 European countries | India (+ pilots abroad) |

| Settlement | Net batch (mostly) | Gross, real-time (Instant) | Real-time gross |

| Reversible? | Yes, with effort | Yes, limited | Limited |

| Who uses it | Banks, corporates, large transfers | Anyone in SEPA zone | Anyone with Indian bank account |

| Technology | MT/MX messages over secure network | ISO 20022 over EBA/ECB networks | API-first, mobile-native |

Other Notable Payment Networks

The SWIFT/SEPA/UPI trio doesn't cover everything. Here are the other networks shaping the global landscape:

FedNow (US, launched 2023) — The US Federal Reserve's real-time payment network. Banks participating can send and receive instant payments 24/7. Competes with the existing RTP network from The Clearing House. Adoption is growing but still limited compared to ACH dominance.

PIX (Brazil, launched 2020) — Managed by the Banco Central do Brasil. Like UPI, it's an instant, 24/7 system with zero-fee person-to-person transfers. Reached 700M+ monthly transactions within 3 years. Required all large Brazilian financial institutions to participate.

Faster Payments (UK, 2008) — The UK's real-time payment network. Processes payments in seconds, 24/7. Max limit £1M per transaction. The model that inspired much of what UPI and PIX became.

CIPS (China) — Cross-border Interbank Payment System, operated by the People's Bank of China. Handles RMB cross-border transactions. Positions as a SWIFT alternative for CNY settlements, primarily used in Belt and Road Initiative transactions.

TIPS (EU) — Target Instant Payment Settlement. The ECB's settlement mechanism for SEPA Instant payments. Provides 24/7 central bank money settlement in euros.

Why Interoperability Is the Next Big Problem

Each of these networks solves payments within its own domain brilliantly. UPI is extraordinary inside India. SEPA makes Europe simple. The problem is the handoffs — what happens when a UPI user needs to pay a SEPA account holder?

Currently, you need SWIFT. Which is slow and expensive. This is the gap that's driving several initiatives:

Project Nexus (BIS) — A framework from the Bank for International Settlements to link national instant payment systems. SEPA Instant ↔ PIX ↔ UPI ↔ FPS without using SWIFT. Pilots underway with ASEAN countries.

mBridge — A multi-CBDC platform for cross-border transactions. Built on distributed ledger technology, involving the central banks of China, Hong Kong, UAE, Thailand, and Saudi Arabia. If successful, it would enable instant, cheap cross-border settlement without correspondent banks.

SWIFT ISO 20022 migration — Upgrading SWIFT's messaging format to ISO 20022 by 2025 enables richer data and better interoperability with modern domestic payment systems.

The long-term vision: instant, low-cost cross-border payments using the same infrastructure as domestic transfers. We're probably 5-10 years away from this being mainstream.

Compliance and Sanctions: What SWIFT, SEPA, and UPI All Have in Common

For all their differences, these three networks share one critical constraint: they are all subject to sanctions enforcement.

SWIFT and sanctions: SWIFT operates under Belgian law and has historically been used as a sanctions enforcement tool. In 2012, Iran was cut off from SWIFT by EU regulation, effectively freezing its access to international banking. In 2022, a subset of Russian banks were disconnected from SWIFT following the invasion of Ukraine. Disconnection from SWIFT is so economically devastating that it's now considered a significant geopolitical tool.

SEPA sanctions: SEPA transfers go through AML/sanctions screening at the originating and receiving banks, and at the national level in some jurisdictions. A payment to a sanctioned individual or entity will be blocked or frozen regardless of which SEPA payment type is used.

UPI and compliance: NPCI requires all banks connected to UPI to perform AML and sanctions screening on transaction participants. India maintains its own sanctions lists (Unlawful Activities Prevention Act, PMLA) and observes UN Security Council sanctions.

This compliance layer is invisible to most users but represents billions of dollars in technology investment by the financial institutions that operate these networks. Failed payments due to sanctions matches, PEP (Politically Exposed Person) screening, and AML flagging are a significant operational cost for banks.

What "ISO 20022" Means and Why It Matters for All Three

ISO 20022 is the international standard for financial messaging — think of it as the common language that payment networks speak. You'll see this term more and more in fintech news, and understanding why it matters requires understanding the problem it solves.

The old way (MT format in SWIFT): SWIFT's legacy MT message format carries limited, rigid data fields. An MT103 wire transfer can contain the amount, sender, recipient, and a short reference field. That's roughly it. AML systems work with limited context and must make fraud decisions on sparse data.

The new way (ISO 20022): Far richer structured data. A payment message can include: purpose code (salary payment, tax payment, goods purchase), creditor/debtor legal entity identifiers (LEIs), full remittance information (invoice numbers, line items), structured addresses, and more. This enables automated reconciliation, better AML scoring, and faster straight-through processing.

Where each network stands:

- SWIFT: Mandatory ISO 20022 migration completed for cross-border payments by end of 2025. A multi-year, industry-wide project.

- SEPA: Adopted ISO 20022 from the start — all SEPA payment types run on ISO 20022 natively.

- UPI: Built on modern XML standards, effectively ISO 20022-aligned in spirit even if not technically certified.

For businesses, the practical impact of ISO 20022 migration is better automatic reconciliation between payment data and invoices/ERPs. For financial institutions, it's a major infrastructure upgrade.

How Banks Actually Connect to These Networks

Understanding the access model of each network clarifies why costs and speeds vary so much.

SWIFT access model: Banks apply for membership, get a SWIFT BIC (Business Identifier Code), and connect to the SWIFT network via licensed software (Alliance Gateway or bureau services). Smaller banks often connect via a "service bureau" — a third party that handles the SWIFT connection on their behalf. This is why your small regional bank can still send international wires: it uses a larger bank as its SWIFT bureau, which adds a hop and a fee.

SEPA access model: Any payment institution or bank authorized in a SEPA country must adhere to SEPA payment scheme rules as a condition of their license. Access to the infrastructure comes via CSMs (Clearing and Settlement Mechanisms) — the EBA Clearing STEP2 system and the ECB's TIPS system are the two main CSMs for SEPA. Banks connect to CSMs either directly or via a correspondent bank that provides SEPA access as a service.

UPI access model: All banks licensed by the RBI that offer savings/current accounts are mandated to be part of UPI. They connect via NPCI's dedicated network. Third-party app providers (TPAPs) like PhonePe and Google Pay get access through a partner bank (called a "Payment Service Provider" in UPI terminology), not directly from NPCI. This is why you can use Google Pay to access your HDFC Bank account — Google Pay partners with Axis Bank and HDFC as PSPs.

Key Takeaways

- SWIFT is a messaging network, not a money mover — it carries payment instructions; actual funds move through correspondent bank relationships. SWIFT gpi has dramatically improved speed and transparency.

- SEPA is Europe's unified payment standard — it makes euro transfers between any of 36 countries as simple and cheap as domestic transfers. SEPA Instant is now mandatory for EU banks.

- UPI is the world's most successful retail payment system by volume — 14B+ transactions/month, near-zero fees, fully interoperable across all Indian banks and apps.

- The real challenge is between-network interoperability — crossing from UPI to SEPA still requires SWIFT and correspondent banking, which is slow and expensive.

- All three networks enforce sanctions and AML compliance — disconnection from SWIFT is now a geopolitical tool; all networks block sanctioned entities.

- ISO 20022 is the common language driving convergence — SEPA was native; SWIFT is migrating; new networks are being built around it from the start.

- New networks (PIX, FedNow, TIPS) are making domestic payments instant everywhere — the remaining gap is cross-border, where projects like Nexus and mBridge are working toward a solution.

Related Reading

- How Cross-Border Payments Work (And Why They're So Slow)

- The Anatomy of a Wire Transfer: From Initiation to Settlement

- Crypto Payment Rails: How Bitcoin/USDT Actually Move Money (Pro)

- How Payment Networks Work: Visa, Mastercard, and the Four-Party Model (Pro)

Stay Ahead of Fintech

This article is free. For deeper dives — including how payment processors make money, how to build a neobank, and our full Digital Payments Masterclass — join FinTekCafe Pro.

Free newsletter: Get weekly fintech insights delivered to your inbox. No spam.

Related Articles

Open Banking Failed Its Promise — Here's What Actually Works

Open Banking promised a revolution. Adoption is low and APIs are fragmented. But the real winners are emerging in unexpected places.

How Central Bank Digital Currencies Will Change Finance

What are CBDCs and how will they change banking? A complete guide to central bank digital currencies, from China's digital yuan to the EU's digital euro.

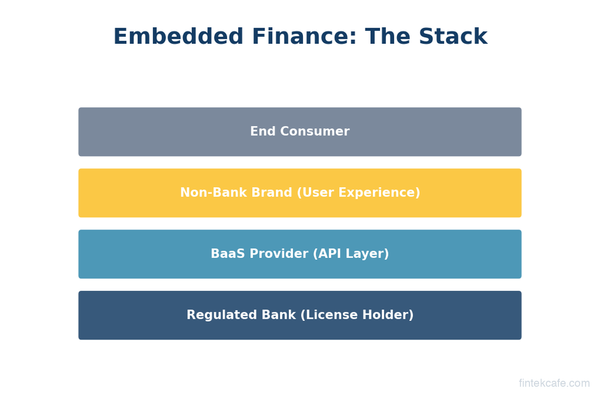

What Is Embedded Finance? How Non-Banks Are Becoming Banks

What is embedded finance and why are non-banks offering financial services? A complete guide to embedded payments, lending, insurance, and banking as a service.