How Cross-Border Payments Work (And Why They're So Slow)

How Cross-Border Payments Work (And Why They're So Slow)

You want to send $1,000 from your US bank account to a friend in India. You walk into your bank branch (or log in online), fill out the form, pay a $35 fee, and wait. Three days later, the money arrives — minus another $10 taken by a bank somewhere in the middle, and minus the FX markup your bank charged without telling you.

Why? The technology to move money internationally should be simple. We can send emails in milliseconds. We can video-call across the world for free. Why does international money movement still resemble the 1970s?

The answer is structural — and understanding it explains everything about why fintech companies like Wise and Remitly are worth billions.

The Correspondent Banking Model

Domestic payments are simple: if you bank at Chase and your landlord banks at Wells Fargo, Chase and Wells Fargo both have accounts at the Federal Reserve. A transfer between them is just two ledger entries at the Fed.

International payments don't have a global "Federal Reserve" that all banks share. Instead, they rely on correspondent banking: a network of bilateral relationships where banks hold accounts with each other in foreign countries.

Nostro and Vostro Accounts

The jargon you'll encounter here:

Nostro account ("ours" in Latin): Your bank's account held at a foreign bank, denominated in that foreign currency. "Our money, held by them."

Vostro account ("yours" in Latin): A foreign bank's account held at your bank. "Their money, held by us."

These are the same account — just described from opposite perspectives. If US Bank A holds an account at Indian Bank B denominated in Indian rupees, Bank A calls it a nostro account; Bank B calls it a vostro account.

Why this matters: Banks don't actually move money internationally — they just adjust balances in these pre-funded accounts. When your US bank sends money to India, it instructs its partner bank in India (via SWIFT message) to credit the recipient's account, debiting the nostro account balance.

This system works, but it requires banks to pre-fund accounts in dozens of currencies, in dozens of countries, to service their customers. That pre-funded liquidity is capital that earns minimal return — and that cost gets passed to customers as fees.

Step-by-Step: Sending $1,000 from the US to India

Let's trace exactly what happens when you initiate a $1,000 wire transfer from your US bank to a recipient at an Indian bank.

The Players

Assume:

- You: Account at US Bank A (e.g., a regional bank)

- Your bank doesn't have a direct correspondent relationship with Indian Bank D

- Recipient: Account at Indian Bank D

The Actual Path

Step 1 — Initiation (You → US Bank A)

You fill out the wire form: recipient name, IBAN/SWIFT BIC, beneficiary bank details, amount. Your bank debits your account $1,000 + its transfer fee ($30-40). It initiates a SWIFT MT103 message.

Step 2 — US Correspondent Chain (US Bank A → US Bank B)

Your regional US bank may not have a direct SWIFT connection to India. It routes through a large US correspondent bank (e.g., JPMorgan, Citibank, Wells Fargo) that does. US Bank A instructs US Bank B via SWIFT: "Transfer $1,000 to Indian Bank D for account holder." US Bank B debits US Bank A's nostro account held at US Bank B.

Step 3 — International Leg (US Bank B → Indian Bank C)

US Bank B has a direct correspondent relationship with a major Indian bank (e.g., SBI, HDFC). It sends a SWIFT message with payment instructions. The money "moves" by reducing the USD balance US Bank B holds at Indian Bank C (or by crediting Indian Bank C's nostro at US Bank B — it depends on the arrangement). Indian Bank C may deduct an intermediary fee here ($5-15). This is the "lifting charge."

Step 4 — Currency Conversion (Indian Bank C)

At some point in the chain, USD must be converted to INR. Depending on the arrangement, this might happen at US Bank B, Indian Bank C, or both. The FX conversion involves a spread — the bank quotes you an exchange rate worse than the mid-market rate. If the real rate is ₹83/USD, you might receive ₹81/USD. On $1,000, that's an extra ~$24 in hidden fees.

Step 5 — Final Delivery (Indian Bank C → Indian Bank D → Recipient)

Indian Bank C may need to route through another Indian bank to reach the specific recipient bank. Eventually, Indian Bank D receives the payment and credits the recipient's account. Indian Bank D may also deduct a receipt fee (₹500-1,000 in some cases).

The Total Cost (What You Actually Pay)

| Fee Type | Approximate Cost |

|---|---|

| Originating bank wire fee | $30-40 |

| Intermediary bank fee(s) | $10-20 |

| FX markup (spread) | $15-30 |

| Receiving bank fee | $5-15 |

| Total | $60-105 |

On a $1,000 transfer, the recipient might receive $895-940. Nearly 10% gone. The World Bank estimates the global average cost of sending $200 is 6.4% — a figure that disproportionately hurts migrant workers sending remittances home.

Why It Takes 1-5 Days

Each step above requires:

- Human review in some banks for compliance/AML checks

- Batch processing (many banks don't process in real-time)

- Cut-off times (miss the 4pm cut-off, wait until tomorrow)

- Time zone differences between countries

- Correspondent bank settlement windows

SWIFT gpi (launched 2017) now requires participating banks to process gpi payments within a specific window — most go same-day or next-day on gpi corridors. But non-gpi transfers still sit in the old system, and not all banks or corridors are gpi-enabled.

The Hidden Fees You Never See

FX markup: The single biggest hidden cost. Banks buy USD and sell INR at worse rates than the interbank (mid-market) rate. This "spread" is their profit. Banks are not required to disclose the markup separately in most jurisdictions — it's buried in the exchange rate quoted.

Lifting charges: Intermediary banks in the chain deduct fees when processing the payment. These are debited from the transfer amount itself. The sending bank's fee disclosure often says "fees may be deducted by receiving and intermediary banks" — which means the recipient gets less than you sent.

Receiving bank fees: Some banks charge the recipient just to receive an international wire. A $10-15 "incoming wire fee" on the Indian end further reduces what actually lands.

Correspondent fee: Your bank charges for using its correspondent network. This is sometimes included in the stated wire fee, sometimes separate.

The total opacity of these costs is why the European Union's PSD2 regulations now require full pre-payment fee disclosure on international transfers — and why regulators globally are pushing for more transparency.

Who's Disrupting Cross-Border Payments

The correspondent banking model's inefficiency created the opportunity for a generation of fintech companies that take a fundamentally different approach.

Wise (formerly TransferWise)

Wise's insight was simple: instead of actually sending money across borders, match people sending money in opposite directions and settle locally.

How Wise actually works: If 1,000 people are sending money from the US to the UK on a given day, and 800 people are sending money from the UK to the US, Wise can net most of these flows. US senders' money goes into Wise's US bank account; UK recipients get paid from Wise's UK bank account. The international movement of funds is minimized — only the net difference actually crosses borders.

This eliminates most correspondent fees. Wise charges 0.4-1.5% depending on the currency corridor, uses the mid-market FX rate (no spread), and shows you exactly what the recipient will receive before you confirm. It's typically 3-8x cheaper than a bank wire.

Wise holds banking licenses or payment institution licenses in all major markets, maintaining local bank accounts in 50+ currencies.

Remitly

Remitly focuses specifically on remittances — migrant workers sending money home. It uses a combination of local payout networks (mobile money, cash pickup, direct bank deposit) and a lighter-weight approach than traditional bank wires.

Speed varies from minutes (mobile money payout in Kenya or Philippines) to 3-5 days (bank deposit in less-connected corridors). Pricing is often a flat fee ($2-5) plus a small FX margin.

Western Union (Digital)

The legacy giant has pivoted significantly to digital. westernunion.com now competes directly with Wise and Remitly on many corridors, with transparent pricing and same-day delivery to mobile wallets in many countries. Still more expensive than Wise on most corridors, but the cash pickup network (500,000 agent locations) remains a unique advantage for recipients without bank accounts.

Crypto as a Cross-Border Rail

Stablecoins — particularly USDT on the Tron network — are now used as practical cross-border payment rails, particularly in:

- US/Europe → Latin America and Southeast Asia

- B2B settlement between crypto-native companies

- Markets where banking infrastructure is weak

A $10,000 USDT transfer on Tron takes ~30 seconds and costs $0.20. The challenge is the on/off ramp: converting USD to USDT and USDT back to local currency at both ends. These conversions involve their own fees and friction, but in many corridors the total cost is still below Wise.

The Future: CBDCs, SWIFT gpi, and Project mBridge

The industry knows the current system is broken. Several initiatives are working to fix it at the infrastructure level.

SWIFT gpi — Already improving speed and transparency significantly. The next phase (gpi Instant) is connecting SWIFT to domestic real-time networks, enabling end-to-end instant settlement for international wires through the existing SWIFT network.

ISO 20022 migration — SWIFT's full migration to the richer ISO 20022 message format by 2025 enables much better data, automated compliance processing, and interoperability with domestic real-time systems.

Project mBridge — A multi-CBDC (Central Bank Digital Currency) platform being developed by the BIS Innovation Hub with central banks of China, Hong Kong, UAE, Thailand, and Saudi Arabia. Enables direct central bank-to-central bank settlement without correspondent banks. If successful, this would be the most radical infrastructure change since SWIFT's founding.

Project Nexus (BIS) — Connects national instant payment systems (India's UPI, Singapore's PayNow, etc.) so cross-border transfers can move at domestic payment speeds. Pilot launched between India, Singapore, Malaysia, Thailand, and the Philippines.

G20 Roadmap — The G20 has a formal roadmap to make cross-border payments cheaper, faster, and more transparent by 2027, with specific targets: international payments to cost under 3%, 75% to complete within an hour.

None of these fully solve the problem today, but the direction is clear: the slow, expensive, opaque system of 2024 will look very different by 2030.

The Compliance Problem: Why Cross-Border Payments Are Slow by Design

Speed is only part of the problem. The other reason international payments are slow is compliance — and this is largely intentional.

Every cross-border payment is subject to:

Sanctions screening: Every bank in the correspondent chain is legally required to check whether the sender, recipient, or any intermediary party is on a sanctions list (OFAC in the US, EU sanctions lists, UN Security Council lists). This happens at every hop. Automated matching takes milliseconds, but false positives require human review.

AML (Anti-Money Laundering) monitoring: Payments that trigger AML rules — unusual amounts, unusual corridors, new counterparties — get flagged for review. Banks are legally liable for facilitating money laundering. A missed flag can result in multi-billion dollar fines (see: HSBC's $1.9B fine in 2012, Deutsche Bank's $630M fine in 2017). Banks are conservative with AML flags.

KYC (Know Your Customer): Your bank must verify your identity and that of your counterparties. If the beneficiary bank in the recipient country doesn't have adequate KYC on file for the recipient, it may delay or reject the payment.

Correspondent bank de-risking: In recent years, large correspondent banks have been quietly closing correspondent relationships with smaller banks in higher-risk jurisdictions (parts of Africa, the Caribbean, Central Asia). This "de-risking" — driven by fear of regulatory penalties — has left some countries with fewer correspondent banking options, which actually makes cross-border payments slower and more expensive for those regions.

The core tension: The financial system wants fast payments AND rigorous compliance. These are fundamentally in conflict. Every speed improvement must be negotiated against compliance requirements. SWIFT gpi improved speed partly by making compliance data richer and more standardized (ISO 20022), so automated screening is faster and more accurate — fewer false positives, less human review.

Remittances: The Human Cost of Slow, Expensive Wires

Cross-border payments aren't just a B2B problem. Approximately 281 million international migrants send money home regularly. These remittances — $800 billion annually by World Bank estimates — are a lifeline for families in developing countries.

The global average cost of sending $200 is 6.4% (World Bank, 2024). For some corridors (sending from South Africa to Zambia, or the US to Mexico via small operators), costs exceed 10%.

The impact: A Filipino nurse in the US earning $50,000/year sending 30% of her income home to her family — $15,000/year — loses $960/year in fees at 6.4%. Over a career, that's $30,000+ in fees. This is not an abstract finance problem.

The G20 target: In 2020, G20 leaders committed to reducing the global average remittance cost to 3% by 2030. Progress has been made — average costs have fallen from 9% in 2009 — but the 3% target remains elusive for many corridors.

Who's serving this market:

- Wise: Strongest for tech-savvy users sending large amounts to developed market bank accounts

- Remitly: Focused on high-volume corridors (US-Philippines, US-India, UK-Nigeria) with speed tiers

- WorldRemit: Strong in Africa and Southeast Asia with mobile money delivery

- Western Union / MoneyGram: Still dominant for cash pickup in regions with low banking penetration

Key Takeaways

- Banks don't actually move money internationally — they adjust balances in pre-funded nostro/vostro accounts via SWIFT messages, creating a chain of intermediary settlements.

- A $1,000 US-to-India wire loses $60-105 in fees — originating bank fee, FX markup, intermediary "lifting charges," and receiving bank fees compound across the correspondent chain.

- Speed is limited by batch processing, cut-off times, and compliance reviews at each bank in the chain — not a technology limitation.

- Compliance is a deliberate speed constraint — sanctions screening, AML monitoring, and de-risking all add processing time, and this is partly by design.

- Wise and Remitly are cheaper because they net flows locally — less actual cross-border money movement means fewer fees and no FX spread markup.

- Remittances cost migrants 6.4% on average — a real economic burden with a G20 target of <3% by 2030.

- CBDC projects (mBridge) and instant payment network linking (Nexus) are the most promising long-term fixes to the correspondent banking system's fundamental inefficiency.

Related Reading

- SWIFT vs SEPA vs UPI: Global Payment Networks Compared

- The Anatomy of a Wire Transfer: From Initiation to Settlement

- Crypto Payment Rails: How Bitcoin/USDT Actually Move Money (Pro)

- How Payment Networks Work: Visa, Mastercard, and the Four-Party Model (Pro)

Free Weekly Fintech Insights

FinTekCafe publishes weekly explainers on payments, fintech infrastructure, and digital banking for professionals who need to understand how the financial system actually works.

Related Articles

Open Banking Failed Its Promise — Here's What Actually Works

Open Banking promised a revolution. Adoption is low and APIs are fragmented. But the real winners are emerging in unexpected places.

How Central Bank Digital Currencies Will Change Finance

What are CBDCs and how will they change banking? A complete guide to central bank digital currencies, from China's digital yuan to the EU's digital euro.

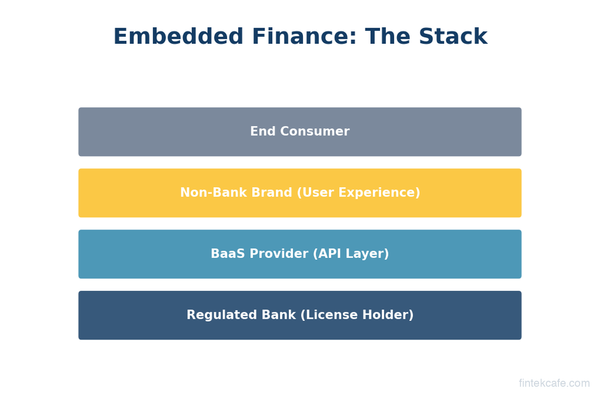

What Is Embedded Finance? How Non-Banks Are Becoming Banks

What is embedded finance and why are non-banks offering financial services? A complete guide to embedded payments, lending, insurance, and banking as a service.