Fintech vs Traditional Banking: 7 Key Differences Every Executive Should Know

The "fintech vs banks" debate usually goes one of two ways. Fintech enthusiasts declare that banks are dinosaurs destined for extinction. Banking traditionalists argue that fintechs are unregulated toys that will collapse at the first sign of economic stress.

Both takes are wrong.

The reality in 2026 is more nuanced and more interesting. Fintechs and traditional banks have fundamentally different strengths, and those differences create specific advantages in specific contexts. Understanding where each model wins (and where it doesn't) matters whether you're running a bank, building a fintech, investing in either, or deciding which to trust with your company's money.

Here are the seven differences that actually matter.

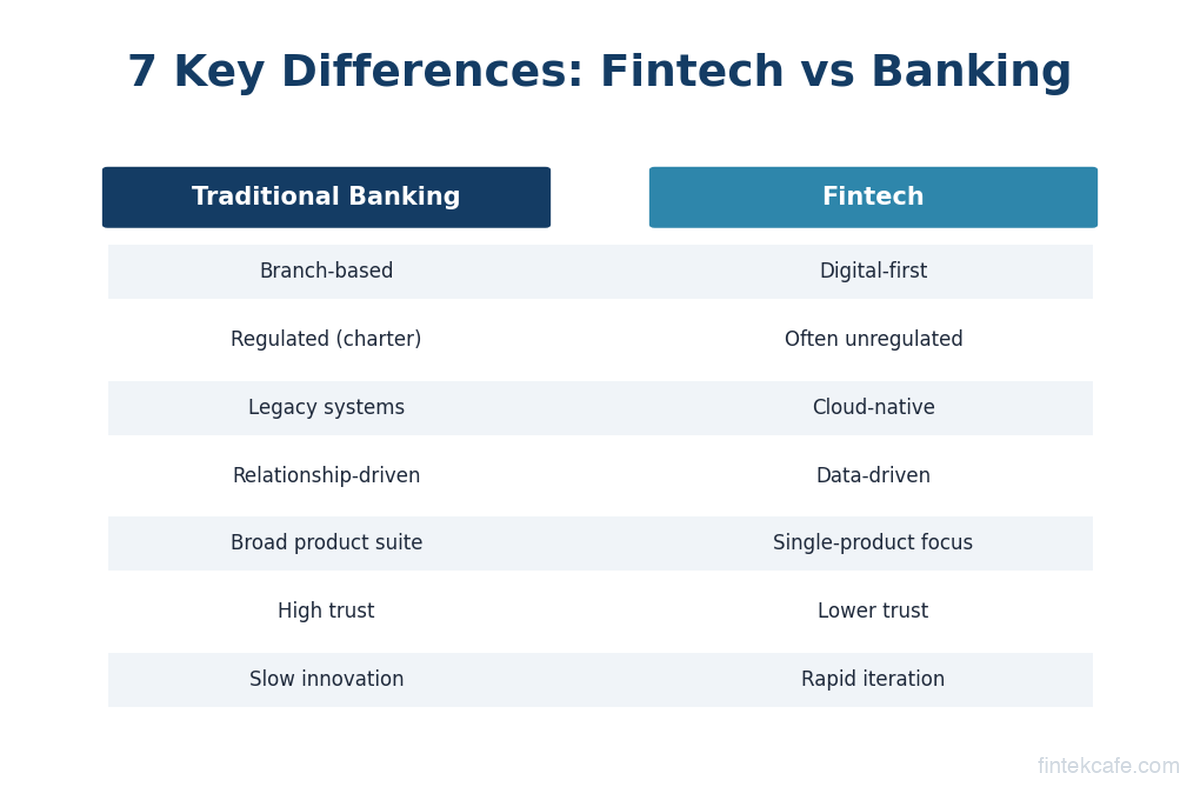

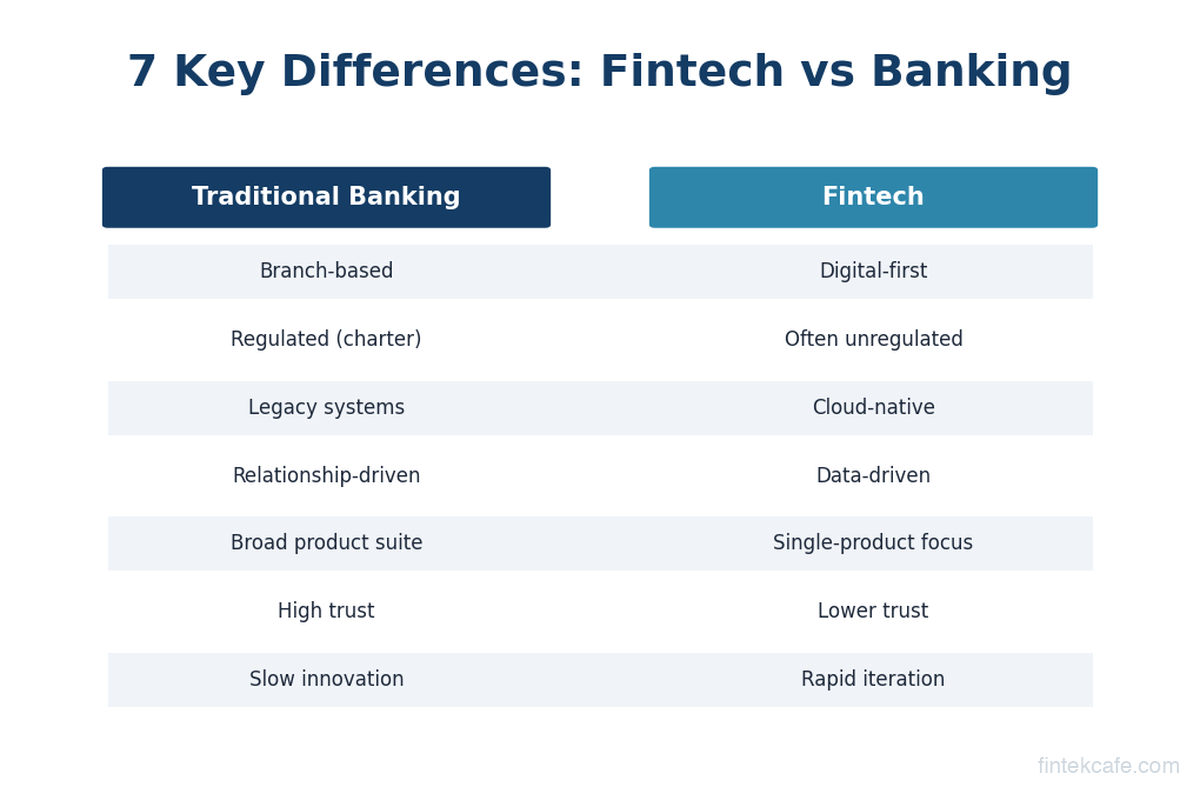

1. Technology Stack: Legacy Infrastructure vs. Cloud-Native

Traditional banks run on technology stacks that are, in many cases, 30-50 years old. JPMorgan Chase, Bank of America, and Wells Fargo all rely on core banking systems built on COBOL, a programming language from 1959. The Federal Reserve estimates that 95% of ATM transactions and 80% of in-person banking transactions still run through COBOL code.

This isn't because banks are stupid. It's because replacing a core banking system at a major bank is one of the hardest technology projects in existence. TSB's attempted migration in 2018 left 1.9 million customers locked out of their accounts for weeks and cost the bank over £330 million. Core banking systems process millions of transactions daily and interface with hundreds of downstream systems. Swapping one out is like replacing the engine of an airplane while it's flying.

The consequence: banks spend 70-80% of their technology budgets on maintaining existing systems (often called "keeping the lights on") and only 20-30% on innovation. JPMorgan spends over $15 billion annually on technology, but the majority goes toward maintaining and patching infrastructure that predates the internet.

Fintechs start with a blank slate. Chime's technology stack was built in the 2010s using modern cloud infrastructure (AWS), microservices architecture, and APIs. There's no legacy code to maintain. When Chime wants to launch a new feature, its engineers can build and deploy it in days or weeks. When a bank wants to launch a similar feature, it often takes months because the new code must integrate with decades-old systems without breaking anything.

Where banks win: Legacy systems, for all their limitations, are battle-tested. JPMorgan's core infrastructure has been processing transactions reliably for decades. It handles Black Friday volume spikes and market crashes without failing. Many fintech platforms haven't been tested through a full economic cycle or a sustained period of extreme volume.

Where fintechs win: Speed of development, cost efficiency (no legacy maintenance burden), and the ability to adopt new technologies (AI, real-time data processing) without integration constraints.

The trend: Banks are slowly modernizing. Goldman Sachs built Marcus on a modern stack. JPMorgan has invested heavily in cloud migration. But the full transition will take decades, not years. In the meantime, fintechs have a structural speed advantage.

2. Customer Acquisition: Branches and Brand vs. Digital and Viral

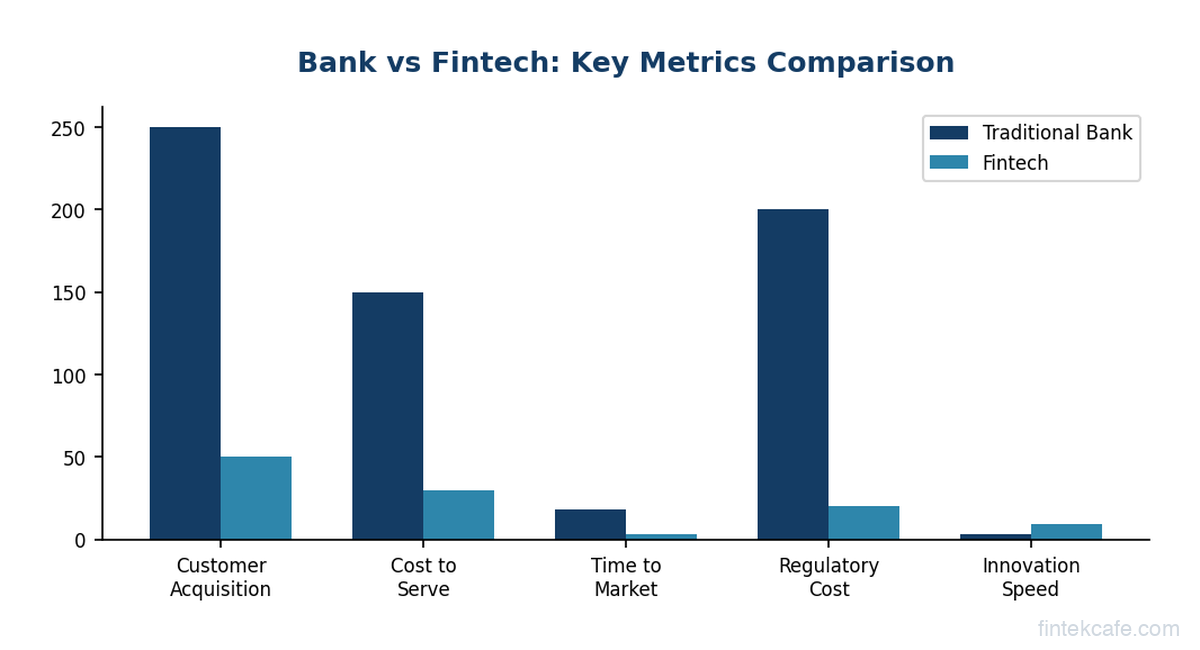

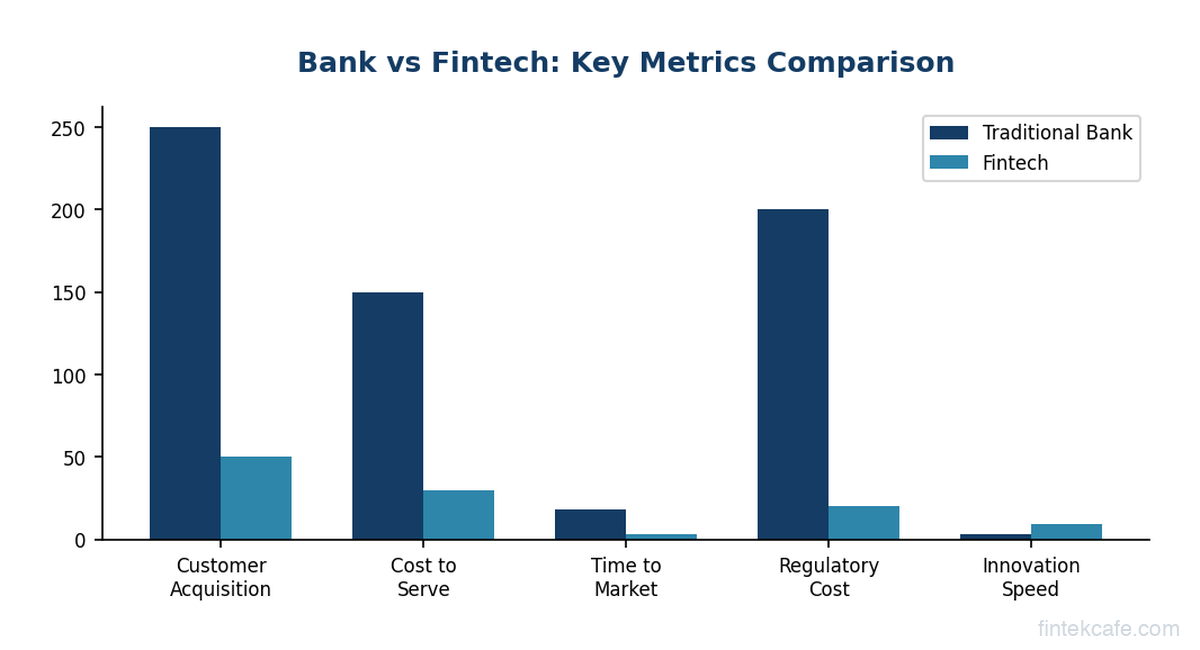

Traditional banks acquire customers primarily through physical presence and brand trust. JPMorgan Chase has approximately 4,700 branches and 16,000 ATMs across the United States. When someone moves to a new city, they often open an account at a bank with a branch near their home or office. This is expensive (a single bank branch costs $2-4 million to open and $1-1.5 million per year to operate) but creates deep local relationships and a physical manifestation of trust.

Banks also benefit from employer relationships. If your company uses Chase for payroll, your direct deposit automatically lands in a Chase account, which creates enormous inertia. Employers direct-deposit into the existing bank, not into the latest fintech app.

Customer acquisition cost (CAC) for a traditional bank is typically $300-500 per new checking account, though the lifetime value is also high because bank customers rarely switch. The average American keeps their primary bank account for approximately 17 years.

Fintechs acquire customers digitally, often through referral programs, social media, and product-led growth. Chime built its user base largely through two strategies: paying users a bonus for direct deposit setup, and referral bonuses. Cash App grew through peer-to-peer virality (to receive money from a Cash App user, you need Cash App). Robinhood grew through waitlists and the novelty of free stock trading.

Fintech CAC varies widely but can be significantly lower than traditional banks: $30-100 per customer for direct-to-consumer apps at scale. The trade-off is that fintech customers tend to be less sticky. Someone who opened a Chime account for the $100 direct deposit bonus may not keep it as their primary account.

Where banks win: Customer retention. Banks have deep relationships reinforced by physical presence, decades of trust, and the sheer friction of switching (moving direct deposits, automatic bill payments, and linked accounts is painful). Older and wealthier demographics still overwhelmingly prefer traditional banks.

Where fintechs win: Acquisition speed and cost. Fintechs can reach millions of customers in months rather than years, without the overhead of physical branches. They dominate younger demographics: roughly 76% of millennials and Gen Z have used at least one fintech service.

The nuance: The best fintechs are learning from banks (building trust, deepening relationships), and the best banks are learning from fintechs (digital onboarding, app-first experiences). The gap is narrowing, but structural differences remain.

3. Regulatory Approach: Licensed and Supervised vs. Chartered and Compliance

Traditional banks hold bank charters granted by federal or state regulators. A charter comes with enormous privileges: the ability to take FDIC-insured deposits, access to the Federal Reserve's payment systems, and the right to lend. It also comes with enormous obligations: capital requirements (banks must hold a minimum ratio of capital to assets), regular examinations by regulators (OCC, FDIC, Fed), and compliance with hundreds of regulations from the Bank Secrecy Act to the Community Reinvestment Act.

A large bank like JPMorgan employs approximately 50,000 people in compliance and regulatory functions. That's more than the total headcount of most fintech companies. Compliance costs for major banks run into the billions of dollars annually.

Fintechs historically operated through partnerships with chartered banks rather than holding charters themselves. Chime is not a bank. It partners with Stride Bank and Bancorp Bank, which hold the charters and provide the regulatory infrastructure. This allows Chime to offer bank-like services without the full weight of banking regulation.

This is changing. SoFi obtained a national bank charter in 2022. LendingClub acquired Radius Bank. Varo became the first consumer fintech to receive a national bank charter from the OCC in 2020. These companies decided that the benefits of a charter (cheaper funding through deposits, regulatory credibility, reduced dependence on bank partners) outweighed the costs (compliance, capital requirements, examinations).

Where banks win: Regulatory credibility and stability. In a crisis, customers trust that their FDIC-insured bank deposits are safe. When Silicon Valley Bank failed in 2023, the flight of deposits went overwhelmingly to JPMorgan, Bank of America, and other large traditional banks, not to fintechs. Regulation, for all its costs, provides a trust framework that fintechs struggle to replicate.

Where fintechs win: Agility. Banking regulation is designed for the traditional banking model and can be slow to adapt to new products. Fintechs operating through partnerships can launch products faster because they're not waiting for regulatory approval for every change. They can also test new markets and products with less regulatory friction.

The risk: The "partner bank" model has shown cracks. The collapse of Synapse (a middleware company connecting fintechs to partner banks) in 2024 left millions in customer deposits in limbo. Regulators, particularly the FDIC and OCC, have responded by increasing scrutiny of bank-fintech partnerships. The regulatory advantage that fintechs enjoyed by avoiding direct regulation is shrinking.

4. Cost Structure: Branch Networks vs. Code

Traditional banks carry enormous fixed costs. Real estate (thousands of branches), personnel (hundreds of thousands of employees), legacy technology maintenance, and compliance infrastructure create a cost base that's difficult to reduce. The average cost-to-income ratio for a US bank is approximately 55-65%, meaning 55-65 cents of every dollar of revenue goes to operating costs.

The branch network is the most visible cost difference. The US banking industry operates approximately 72,000 branches (down from a peak of 99,000 in 2009). Each branch requires real estate, staff, security, and maintenance. The decline in branch count reflects both digital adoption and economic pressure, but branches remain central to most banks' strategies because they drive deposit gathering and relationship building.

Fintechs are structurally leaner. Chime reportedly operates with around 1,500 employees to serve over 20 million customers. A traditional bank serving 20 million customers would employ 30,000-50,000 people. The cost-to-income ratio for well-run fintechs is typically 30-45%, significantly lower than traditional banks.

This cost advantage shows up directly in what customers pay. Chime offers no monthly fees and no overdraft fees. Traditional banks charge $5-15/month for basic checking and $35 per overdraft (though many have recently reduced or eliminated overdraft fees under competitive pressure from fintechs). Wise offers international transfers at 0.35-1.5% versus banks' 2-4% because its cost base is a fraction of a traditional bank's.

Where banks win: Scale and diversification. A large bank's cost structure, while heavy, supports a diversified business model (retail banking, commercial banking, investment banking, wealth management, treasury services) that generates revenue from many sources. Fintechs are typically concentrated in one or two product areas, making them more vulnerable to disruption in those specific categories.

Where fintechs win: Unit economics in their target market. For basic consumer banking (checking, savings, payments), fintechs can deliver a comparable product at 30-50% lower cost. This advantage narrows or disappears for more complex products (commercial lending, treasury management, investment banking) where banks' expertise and relationships justify higher costs.

5. Speed of Innovation: Ship Fast vs. Ship Safe

Traditional banks move slowly by design. Every product change must go through compliance review, risk assessment, legal review, and often regulatory approval. A new feature that a fintech could build and ship in two weeks might take a bank six months, not because the bank's engineers are slower, but because the approval process is longer.

Banks also face the "innovator's dilemma." Launching a new digital product that cannibalizes an existing profitable product (like a free checking account that competes with a $12/month checking account) faces internal resistance. Business unit leaders protect their revenue lines, and the incentive structure often punishes cannibalization even when it's strategically correct.

Fintechs ship fast. Stripe deploys code to production hundreds of times per day. Revolut has launched over a dozen product categories (banking, crypto, stock trading, travel insurance, phone insurance) in under a decade. The combination of modern technology, no legacy constraints, and startup culture enables a pace of innovation that banks can't match.

Where banks win: Risk management in innovation. Banks move slowly, but they're less likely to launch a product that blows up. When fintechs move fast, they sometimes break things that shouldn't be broken. Robinhood's 2020 outage during a historic market rally, Cash App's fraud problems, and various BNPL companies' credit losses all stemmed partly from prioritizing speed over robustness.

Where fintechs win: Time-to-market and iteration speed. In a market where customer expectations are shaped by consumer technology (why can't my bank be as easy as Amazon?), the ability to ship improvements quickly is a significant advantage. Fintechs can also test and kill products faster. A bank that launches a new product usually sticks with it for years; a fintech might test, iterate, or shut down a product in months.

The convergence: Banks are trying to innovate faster by creating separate digital units (Goldman's Marcus, JPMorgan's Chase Mobile-first features) that operate with more fintech-like speed. Fintechs are learning to be more disciplined about risk as they mature. Both are meeting somewhere in the middle.

6. Data Usage: Compliance-Constrained vs. Data-Native

Traditional banks sit on some of the richest customer data in the world: transaction histories, income levels, spending patterns, credit behavior, and life event signals (buying a house, having a baby, retiring). A bank that can see your direct deposits, mortgage payments, and credit card transactions knows more about your financial life than almost any other institution.

But banks underutilize this data dramatically. Partly because of regulatory constraints (privacy laws, fair lending regulations), partly because of organizational silos (the credit card division can't easily access the mortgage division's data), and partly because of legacy technology that makes data analysis difficult. Many banks still run analytics on batch data that's 24-48 hours old rather than real-time.

Fintechs are data-native. Every product decision, every feature design, and every marketing campaign is driven by data. Stripe analyzes billions of transactions to train its Radar fraud detection model. Plaid aggregates financial data across thousands of institutions. Robinhood tracks every user interaction to optimize its app.

Fintechs also have fewer organizational barriers to using data. A startup with 500 employees and a unified data infrastructure can move data across product lines freely. A bank with 250,000 employees, dozens of legacy systems, and a maze of regulatory constraints cannot.

Where banks win: Data breadth. A full-service bank sees a customer's entire financial life: income, spending, borrowing, saving, investing. Most fintechs see only a narrow slice (just your spending, or just your investments). This breadth of data gives banks a theoretical advantage in understanding customer needs and creditworthiness.

Where fintechs win: Data utilization. Having data is useless if you can't act on it quickly. Fintechs use machine learning and real-time analytics to personalize experiences, detect fraud, and make lending decisions in milliseconds. A bank might have richer data but extract less value from it due to organizational and technological constraints.

The future: Open banking regulations (PSD2 in Europe, Section 1033 in the US) are breaking down banks' data monopoly by requiring them to share customer data with authorized third parties. This benefits fintechs, which can now access bank-quality data without being banks. Long term, the advantage shifts from who has the data to who can use it most effectively.

7. Customer Experience: Digital-First vs. Full-Service

Traditional banks offer breadth. Walk into a Chase branch, and you can open a checking account, apply for a mortgage, set up a trust, meet with a financial advisor, notarize a document, get a cashier's check, and access a safe deposit box. No fintech offers anything close to this range of services.

Banks also provide human relationships. For complex financial needs (business banking, estate planning, commercial lending), having a banker who knows your situation is genuinely valuable. A chatbot cannot replace a relationship manager who has worked with your business for a decade.

The downside: the everyday digital experience at most banks ranges from acceptable to frustrating. Opening an account often still requires a branch visit or a cumbersome online application. Sending an international wire requires calling the bank or visiting a branch at many institutions. Basic features like real-time transaction notifications, which every fintech has offered for years, only became standard at major banks in the last few years.

Fintechs offer depth in their specific product area. Wise offers the best international transfer experience available. Robinhood offers the smoothest stock-trading interface. Chime offers the most frictionless basic banking experience. In their narrow focus areas, fintechs provide experiences that are dramatically better than what banks offer.

The downside: narrow focus means customers need multiple apps. Your checking might be at Chime, your investing at Robinhood, your international transfers at Wise, your BNPL at Affirm, and your budgeting at Mint (rest in peace) or YNAB. Managing financial life across five apps is fragmented and can make it harder to see the complete picture.

Where banks win: Complexity and breadth. If you need a mortgage, a business line of credit, and estate planning, a bank is your one-stop shop. Fintechs that have tried to become full-service financial platforms (the "super-app" approach) have struggled to match the breadth of a traditional bank.

Where fintechs win: Simplicity and focus. For any single financial task (sending money, investing, expense tracking, payments), the fintech version is almost always faster, cheaper, and more pleasant to use. Younger consumers increasingly prefer the fintech experience for everyday finance.

The trajectory: Both sides are expanding. Banks are pouring billions into improving their digital experiences (Chase Mobile, Capital One's digital-first approach). Fintechs are broadening their product suites (SoFi now offers banking, lending, investing, and insurance). The question isn't "who wins" but where each model has a durable advantage.

So Who Wins?

Neither. That's the honest answer, and anyone who tells you otherwise is selling something.

Banks will dominate complex financial services (commercial banking, investment banking, wealth management, treasury) for the foreseeable future. The expertise, relationships, balance sheets, and regulatory infrastructure required for these services create moats that fintechs cannot easily cross.

Fintechs will dominate simple, high-frequency financial tasks (payments, basic banking, transfers, BNPL) where technology advantage and lower costs translate directly into better customer experiences.

The middle ground (consumer lending, insurance, investment management) is where the real battle is happening, and it's genuinely unclear who will win. Both banks and fintechs have legitimate advantages, and the outcome likely varies by product and customer segment.

The smartest executives in both camps have stopped thinking about "fintech vs. banks" as a competition. The best banks are partnering with fintechs (JPMorgan embedded into numerous platforms, Goldman's Transaction Banking products). The best fintechs are partnering with banks (Stripe Treasury uses Goldman Sachs, Chime partners with Stride Bank and Bancorp). The future isn't one replacing the other. It's a financial system where traditional and digital institutions play complementary roles, each doing what they do best.

Key Takeaways

- Traditional banks and fintechs have fundamentally different strengths. Banks win on breadth, trust, regulatory credibility, and complex financial products. Fintechs win on speed, cost, user experience, and simple financial tasks.

- The technology gap is real but narrowing. Banks spend 70-80% of tech budgets on maintenance. Fintechs build on modern infrastructure with no legacy burden. Banks are modernizing, but it will take decades.

- Cost structure is the fintech's biggest advantage. No branches, fewer employees, and lower compliance overhead allow fintechs to offer comparable products at 30-50% lower cost for basic financial services.

- Regulation is the bank's biggest moat. Bank charters, FDIC insurance, and deep compliance infrastructure create trust that fintechs can't easily replicate, especially in a crisis (SVB's deposits didn't flee to Chime).

- The future is partnership, not replacement. The smartest companies on both sides are finding ways to combine fintech speed and innovation with banking infrastructure and trust.

Frequently Asked Questions

Will fintechs replace traditional banks?

Not entirely. Fintechs are replacing banks for certain tasks (basic payments, simple transfers, stock trading for retail investors) but cannot match banks' capabilities in complex financial services like commercial lending, treasury management, investment banking, and wealth advisory. The more likely outcome is a financial system where fintechs handle everyday consumer finance while banks focus on complex and relationship-intensive services.

Are fintechs safer than banks?

It depends on what you mean by "safe." Banks offer FDIC insurance (up to $250,000 per depositor), regular regulatory examinations, and capital requirements. Fintechs that partner with banks may offer FDIC pass-through insurance, but the structure is more complex (as the Synapse collapse demonstrated). For pure deposit safety, a chartered bank is generally safer. For data security and fraud protection, many fintechs invest heavily in modern security infrastructure that can exceed what older bank systems provide.

Why do banks charge higher fees than fintechs?

Banks carry significantly higher operating costs: physical branches ($1-1.5M/year each), large compliance teams (JPMorgan employs ~50,000 in compliance), and legacy technology maintenance. These costs are passed to customers through account fees, wire transfer charges, and FX markups. Fintechs avoid most of these costs by operating digitally, which allows them to offer lower fees or no fees for comparable services.

Should my company use a bank or a fintech for business finances?

Most businesses benefit from both. Use a traditional bank for primary business banking (the stability, FDIC insurance, and lending relationships are valuable), and use fintechs for specific functions where they excel: international payments (Wise), expense management (Ramp or Brex), payroll (Gusto), and invoicing (Bill.com). This "best of both" approach gives you banking stability with fintech efficiency.

Explore our courses to understand both sides of this transformation, from payment infrastructure to AI in financial services.

Related Articles

Open Banking Failed Its Promise — Here's What Actually Works

Open Banking promised a revolution. Adoption is low and APIs are fragmented. But the real winners are emerging in unexpected places.

How Central Bank Digital Currencies Will Change Finance

What are CBDCs and how will they change banking? A complete guide to central bank digital currencies, from China's digital yuan to the EU's digital euro.

What Is Embedded Finance? How Non-Banks Are Becoming Banks

What is embedded finance and why are non-banks offering financial services? A complete guide to embedded payments, lending, insurance, and banking as a service.