What are different Payment Networks?

In the previous post, we looked at how digital payments work through credit card networks. We also covered the different players involved in completing a digital payment between a buyer and a seller.

This post explores other ways money moves digitally. That includes transfers between two individuals (known as Peer to Peer, or P2P) and payments between consumers and businesses.

To achieve economies of scale and meet regulatory requirements, all money transactions flow through one network or another. The payment methods discussed below focus on the United States. The same general processes apply in other countries, with some variation based on local regulations.

Debit Cards

Debit card processing works much like credit card processing. The issuing bank provides a debit card to its customer and links that card to the customer's checking or savings account.

The key difference between credit and debit cards comes down to where the money comes from. With a credit card, the bank pays the merchant on the consumer's behalf. The consumer can make a purchase even with an empty bank account. They then pay the bank back when the monthly statement is due. If they don't pay in full, the bank charges interest.

With a debit card, the money comes directly from the consumer's bank account. The funds must already be there at the time of purchase.

For example, say a box of chocolates costs $100. With a debit card, the consumer must have $100 in their bank account. With a credit card, they just need a $100 credit line (the ability to borrow from the bank) and can buy the chocolates without having any cash in their account.

Like credit card transactions, debit transactions have three stages.

(a) Authorization

Debit cards can be used in two ways: as a debit card (withdrawing cash from a personal account) or as a credit card (using a credit line). The consumer makes this choice at the time of purchase, or the merchant may make it for them.

Most people have experienced this at the grocery store. When using a debit card, you either enter a PIN (similar to an ATM withdrawal) or sign on the P.O.S. (point of sale) device.

A "pin" based transaction is a debit transaction, and a "signature" based transaction is a credit transaction.

Here is how the authorization process works:

- The consumer presents their debit card at the merchant's P.O.S. and enters their PIN.

- By entering the PIN, they have chosen a debit transaction.

- The P.O.S. captures the transaction details and sends them to the processor.

- The processor forwards the information to the issuing bank.

- The issuing bank runs validations. These include verifying the account exists, checking that sufficient funds are available, and performing other security checks. It then sends back a success or failure response.

- The authorization response travels back to the P.O.S. through the processor.

If the issuing bank approves the authorization, the transaction is complete, and the buyer can finish their purchase.

(b) Clearing.

During clearing, the merchant (typically at the end of the day) sends all successful sale transactions to the processor. The processor then forwards this information to the respective issuing banks.

(c) Settlement.

In the settlement stage, the issuing bank transfers the funds to the acquiring bank through the appropriate networks.

Digital Wallets

Digital wallets are specialized software on mobile phones that facilitate mobile payments.

Plastic cards replaced cash; now the digital wallets are replacing plastics.

There are three main types of digital wallets.

(a) Pass through digital wallet (proxy wallet)

Instead of carrying physical debit or credit cards in your pocket, you store digital versions of those cards on your smartphone.

(b)Stored value wallet

This type of wallet holds actual digital currency. The customer has an account linked to the wallet and must add funds to the account before making any purchases. Think of it like a prepaid debit card or gift card.

(c) Staged digital wallet

This is an extension of the stored value wallet. It allows "live loading," meaning the wallet owner can add funds during an actual purchase in real time, even if the wallet balance is too low.

Let's look at how each wallet type works in a transaction:

- The consumer pulls up their phone and taps it against the POS.

Case a:

For a proxy wallet transaction, the process is the same as a standard credit card transaction. It follows the usual flow involving the P.O.S., processor, issuing bank, and acquiring bank. The proxy wallet simply replaces the physical credit card.

Case b:

For a stored-value wallet, the merchant P.O.S. interacts directly with the digital wallet. If the wallet doesn't have enough funds, the purchase is declined.

For a staged-value wallet, the process has two stages. In the first stage (funding), the wallet provider ensures the account has enough money to complete the transaction. In the second stage, the actual purchase takes place. Both stages happen in real time within the digital wallet.

Check

After cash, the check is the oldest form of exchanging money between individuals or businesses.

The United States passed a law called "Check 21" after the 9/11 attacks. This act transformed how checks are handled in the country. The most important change was that banks could now use a digital image of a check instead of the physical paper to complete transactions.

Before this law, $6 billion worth of checks were literally in the air on planes on any given day. During a crisis that grounds flights (like 9/11), the nation's economy could grind to a halt due to a liquidity crisis.

"Nearly all the checks the Federal Reserve Banks process for collection are now received as electronic check images. -" U.S. Federal Reserve Bank.

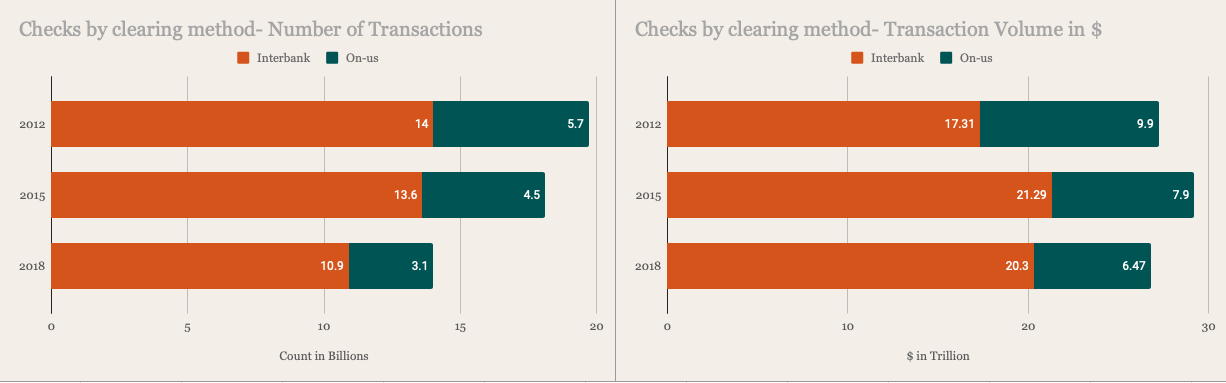

There are two types of check processing: (a) "inter-bank check" -- where the check is deposited at one bank but drawn on a different bank; and (b) "on-us checks" -- where the check is deposited and drawn at the same bank.

Around 78% of checks were processed in the U.S. in 2018, where "interbank checks" accounting for approximately 76% of the dollar amount transacted through checks in the year 2018.

On-us Checks

With on-us checks, both the "payer" (the person sending money) and the "payee" (the person receiving money) have accounts at the same bank. The payer writes a check and gives it to the payee. The payee deposits the check. Since both accounts are at the same bank, the bank simply debits the payer's account and credits the payee's account.

Interbank Checks

With interbank checks, the payer and payee have accounts at different banks. The payee deposits the check at their bank. We call this the "depositing bank." The depositing bank then needs to collect the money from the payer's bank, which we call the "issuing bank."

The depositing bank has several options for processing these checks.

(a) Reserve Bank

The bank can send the check image to the Federal Reserve Bank. The Reserve Bank then debits the issuing bank and credits the depositing bank.

(b)Check clearinghouse

Both the issuing bank and depositing bank may be members of a check clearinghouse. Member banks make direct transactions with each other through a "settlement bank." The main advantage is that clearinghouse rules govern all member banks, so they don't need separate settlement agreements with each other.

(c) Correspondent financial institution

The depositing bank can send the check image to a "correspondent." Think of correspondents as "banks for banks." The correspondent credits the depositing bank and then collects the money from the issuing bank.

(d) Direct contact with the "issuing bank"

The depositing bank can send the check image directly to the issuing bank. For this to work, the two banks must already have settlement agreements in place.

Automated Clearing House (ACH)

ACH payments are electronic transfers from one bank account to another. They are extremely common and used for things like salary deposits and bill payments from a checking account. ACH was invented in the 1970s to reduce the mountain of paper generated by checks.

There are two types of ACH payments.

(a) ACH Debit - known as "Direct Payment"

This is a "pull" transaction. An institution pulls money from your bank account. The most common example is when consumers pay bills through their bank, such as utility or subscription payments.

(b) ACH Credit - know as "Direct Deposit"

This is a "push" transaction. An institution pushes money into your bank account. The most common example is when your employer deposits your salary into your account.

Who are the different players involved in ACH?

(a)Nacha(National Automated Clearing House Association)

Nacha is the central governing body of the ACH network. It develops rules and standards, provides industry solutions, and delivers education, accreditation, and advisory services.

(d) Originating Depository Financial Institution (ODFI)

The ODFI is the bank that processes transactions on behalf of the originator (the entity initiating the payment).

(e)Receiving Depository Financial Institution (RDFI)

The RDFI is the bank that processes transactions on behalf of the receiver (the entity receiving the payment).

(f) ACH operator

Operators act as intermediaries between the ODFI and RDFI. They facilitate settlement operations between member banks. The two main operators in the U.S. are the Federal Reserve Bank and The Clearing House (TCH), which owns the Electronic Payments Network (EPN). Settlement between operators is handled by the Reserve Bank.

(g)Receiver

The Receiver is the person or entity on the receiving end of an ACH transaction. In a direct deposit, the receiver is credited with the amount. For example, an employee receiving their salary via direct deposit is the receiver. In a direct payment, the receiver is debited. For example, a consumer paying their utility bill is the receiver in ACH terminology.

(h)Originator

The Originator is the company that initiates the ACH transaction. It is responsible for the transaction on the ACH network and either credits or debits the receiver's bank account. Using the examples above, the employer and the utility company are the originators.

Wire

Wire transfers have been around since the late 1800s. People originally used telegraph networks to "wire" transfer instructions and passcodes between banks. The technology has evolved significantly since then.

A wire transfer involves several parties: (a) a "payer" -- the person or entity starting the transfer; (b) a "payee" -- the person or entity receiving the money; (c) a sending bank -- the bank holding the payer's account; (d) a receiving bank -- the bank holding the payee's account; and (f) the wire transfer network.

There are three main wire transfer networks.

(a) FedWire.

With FedWire, participating banks hold accounts at the Federal Reserve. When money is wired between two banks, the Federal Reserve debits the sending bank and credits the receiving bank.

Wire transfers are irrevocable -- they cannot be reversed. Because of this, the sending bank bears most of the liability. It must ensure enough funds are available before initiating the transfer. This may mean collecting from the payer upfront or providing a short-term loan if a deposit is pending.

(b) Clearing House Interbank Payments System(CHIPS)

CHIPS is the second major wire transfer network in the U.S. The key difference between CHIPS and FedWire is ownership: CHIPS is privately owned, while the U.S. Government owns FedWire. CHIPS has around fifty participating member banks and handles most international wire transfers. It is both a customer of and a competitor to FedWire.

(c)Society for Worldwide Interbank Financial Telecommunications (Swift)

SWIFT is not a traditional payment system. It does not manage any accounts or move any funds. Instead, it is a messaging service. Each participating organization is identified by a unique eight- or eleven-digit code.

Here is how it works: the payer goes to the sending bank and provides the payee's account number and the receiving bank's SWIFT code. The sending bank sends a SWIFT message with the account details to the receiving bank. The receiving bank then credits the payee's account.

ATM

The interbank ATM network is another common payment network that banking consumers use regularly.

Here are a few scenarios. A bank customer withdraws money from their own bank's ATM. This transaction is typically free as part of the checking or savings account. A customer uses an ATM at a different bank. If both banks belong to the same ATM network, the network may charge a fee that is deducted from the customer's account. If the other bank is not part of the same network, the fees are usually higher.

Some popular ATM networks in the U.S. include Star Network (owned by First Data), MoneyPass (owned by Fiserv), and the New York Currency Exchange or NYCE (owned by Fidelity National Information Services). Settlement for these networks flows through FedWire and CHIPS, the wire transfer systems discussed earlier.

Current State of Payment System.

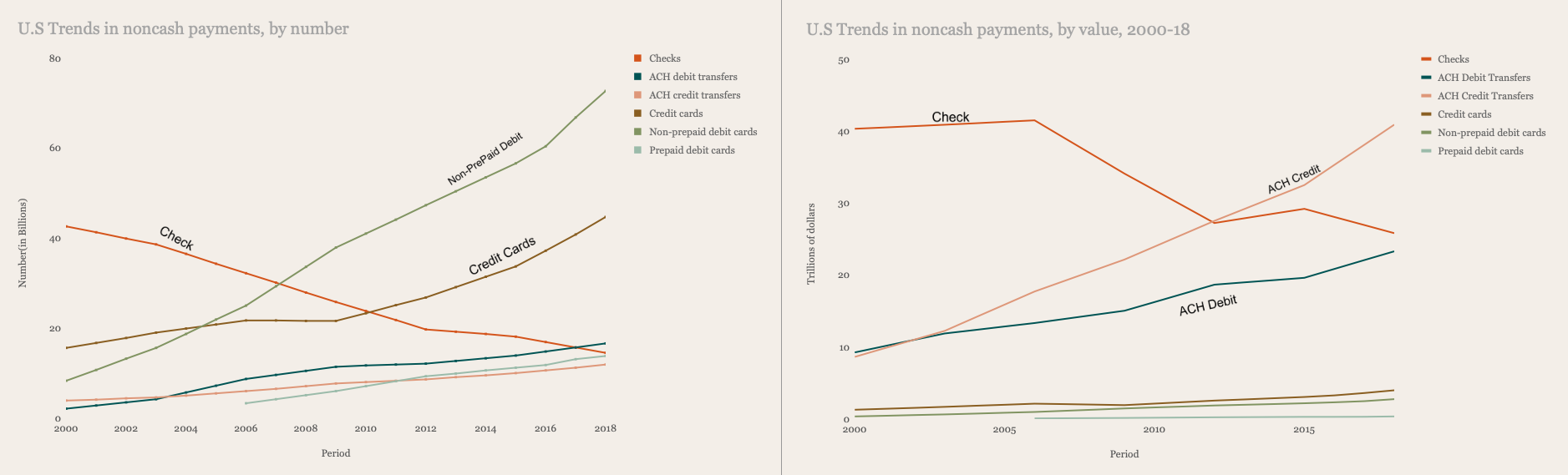

Data from the Federal Reserve Payments Study (FRPS) paints a clear picture. Credit and debit card transactions are growing in volume year over year. Check-based transactions, on the other hand, are declining. ACH debit and ACH credit payments are also increasing in dollar value year over year, more than making up for the drop in check usage.

The 2019 Federal Reserve Payments Study (FRPS), seventh in a series of triennial studies, found accelerating growth overall in core noncash payments from 2015 to 2018 compared to the previous three years. Automated clearinghouse (ACH) and card payments accelerated, while Checks continued to decline over the same period.

The fintech revolution is currently underway, and we can expect to see a shift toward decentralized payment systems in the years ahead.

Related Articles

Open Banking Failed Its Promise - Here's What Actually Works

Open Banking promised a revolution. Adoption is low and APIs are fragmented. But the real winners are emerging in unexpected places.

How Central Bank Digital Currencies Will Change Finance

What are CBDCs and how will they change banking? A complete guide to central bank digital currencies, from China's digital yuan to the EU's digital euro.

What Is Embedded Finance? How Non-Banks Are Becoming Banks

What is embedded finance and why are non-banks offering financial services? A complete guide to embedded payments, lending, insurance, and banking as a service.