Embedded Finance Explained: Why Every Company Wants to Be a Bank

The Premise Is Simple. The Implications Are Not.

Shopify lends money to its merchants. Uber issues debit cards to its drivers. Amazon extends credit to its sellers. Apple launched a savings account that pulled in $10 billion in deposits in four days.

None of these companies are banks. None of them want to be banks. What they want is to capture the financial margin that sits between their product and their customer's wallet — without absorbing the regulatory overhead of a banking license. That is the core proposition of embedded finance: financial services delivered by non-financial companies at the exact moment of need, invisible to the user, seamless in the experience.

This is not a small thing. Bain Capital and Bain & Company estimated in 2022 that embedded finance would facilitate $7 trillion in total transaction value by 2026, more than double the $2.6 trillion recorded in 2021. Lightyear Capital projected the revenue pool for embedded financial services at $230 billion by 2025. Whether those numbers land precisely is beside the point. The directional signal is unambiguous: financial services are migrating from standalone institutions to contextual features within existing software platforms.

The question worth asking is not whether this shift is happening. It is: who captures the value? The platform embedding the financial product? The infrastructure provider enabling it? Or the regulated bank whose charter makes it all legal?

What Embedded Finance Actually Means

Strip away the marketing and embedded finance is three things happening simultaneously.

First, non-financial companies are integrating financial products — payments, lending, insurance, bank accounts — directly into their existing platforms. The customer never leaves the platform. The financial product appears as a native feature, not a redirect to a bank's website.

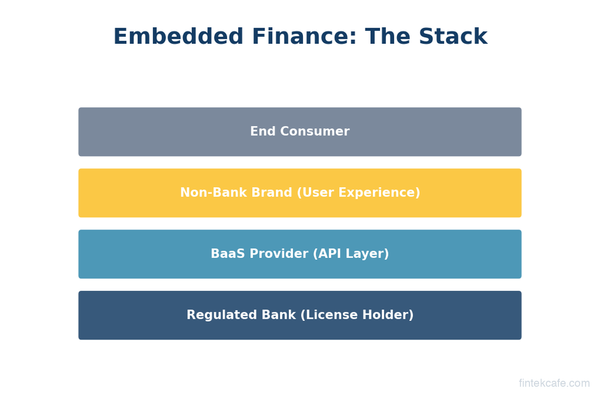

Second, a technology layer — Banking-as-a-Service providers, payment processors, card issuers — makes this integration possible through APIs. The platform does not build financial infrastructure from scratch. It plugs into infrastructure that already exists.

Third, a regulated financial institution sits behind the technology layer, providing the license, the compliance framework, and the deposit insurance that makes the financial product legally viable. This is the sponsor bank — the entity that holds the actual money and bears the actual regulatory responsibility.

The stack, simplified:

| Layer | Role | Examples |

|---|---|---|

| Distribution | The platform the customer already uses | Shopify, Uber, Amazon, Toast |

| Enablement | API infrastructure connecting platform to bank | Unit, Stripe Treasury, Marqeta, Bond |

| Regulation | Licensed bank providing charter and compliance | Cross River, Column, Evolve, Goldman Sachs |

The magic — and the structural tension — is that the customer only sees the top layer. They see Shopify lending them money for inventory. They do not see Cross River Bank originating the loan, or the middleware platform processing the KYC check. The brand relationship belongs to the platform. The regulatory exposure belongs to the bank. The economics are shared, unevenly, across all three.

The Products: What's Being Embedded

Embedded finance is not a single product category. It is a set of financial primitives being integrated across radically different contexts.

Embedded Payments

This is where embedded finance started and where the largest transaction volumes sit. Every time you tap "Pay" inside an Uber ride, order on DoorDash, or check out on Shopify, you are using embedded payments. The payment is processed within the platform, using stored credentials, with no redirect to a third-party payment page.

Stripe is the canonical example. Over 3 million businesses use Stripe to process payments, handling hundreds of billions of dollars in annual volume. Stripe's insight was that payments should be an API call, not an IT project. That insight created a $50 billion company and established the template for every other embedded finance category.

The economics are well-understood. Stripe charges approximately 2.9% plus $0.30 per transaction. The platform passes that cost through to the merchant or absorbs it as a cost of doing business. At scale, the payments margin alone can be substantial — Shopify's payments revenue exceeded $1.7 billion in 2023, representing more than half of its merchant solutions revenue.

Embedded Lending

This is where the revenue opportunity gets interesting. When Shopify Capital offers a merchant a cash advance against future sales, the underwriting is based on data Shopify already has — transaction history, sales trends, seasonal patterns, return rates. No traditional bank has access to that data in real time. The result is faster approval, lower default rates, and higher conversion.

Shopify Capital has disbursed over $5 billion in merchant cash advances and loans since its launch in 2016. Amazon Lending, which extends credit to third-party sellers, has originated over $9 billion in loans since 2011. These are not small experiments. They are multi-billion-dollar lending businesses built on proprietary data advantages that incumbent banks cannot replicate.

The structural advantage is clear: the platform that controls the distribution channel can also control the repayment channel. Shopify Capital repayments are automatically deducted from future sales. There is no collections process because there is no separate payment to collect. The loan is embedded in the cash flow.

Embedded Banking

When a platform offers its users a bank account — a balance, a debit card, the ability to send and receive money — it is embedding banking. Uber's driver debit card, which gives instant access to earnings instead of waiting for weekly ACH transfers, is embedded banking. Lyft's Direct card serves the same purpose. DoorDash's DasherDirect card does the same.

The user value proposition is speed: get your money immediately instead of waiting three to five business days. The platform value proposition is retention: drivers who receive instant payouts through the platform's debit card are measurably less likely to switch to a competing platform.

Apple's entry into embedded banking via its high-yield savings account — launched in April 2023 in partnership with Goldman Sachs, offering a 4.15% APY at launch — demonstrated what happens when the world's most trusted consumer brand embeds a financial product. The account attracted over $10 billion in deposits within four days and nearly $100 billion in the first year. No fintech in history has achieved that speed of deposit accumulation. Apple did it by embedding the savings account directly into the Wallet app, accessible from the lock screen, two taps away from any Apple Card transaction.

Embedded Insurance

When you book a flight on Expedia and are offered trip cancellation insurance, that is embedded insurance. When you purchase electronics on Amazon and are offered an extended warranty, that is embedded insurance. When Tesla offers auto insurance priced using its own telematics data, that is embedded insurance — and it is structurally different from everything that came before it.

Tesla's insurance product, available in 12 states, uses real-time driving behavior data from the vehicle itself to price policies. This is data that no traditional insurer has access to. The result is more accurate pricing, lower loss ratios, and a customer experience that is entirely contained within the Tesla ecosystem. Tesla's insurance revenue is still small relative to its automotive business, but the model demonstrates the embedded insurance thesis: the company that owns the risk data can price the insurance better than the company that buys the risk data secondhand.

Why Every Company Wants to Do This

The financial incentive is straightforward. Financial services have structurally higher margins than most software and commerce businesses.

A SaaS company operating at a 75% gross margin might be earning $100 in revenue per customer per year. Add a financial product — a business checking account, a lending product, a card program — and the incremental revenue per customer can be $200 to $500 annually, with gross margins of 50-70% on the financial products themselves.

The math is even more compelling for platforms that already have high transaction volumes. Shopify processing billions in gross merchandise volume through its platform captures approximately 2.5-2.9% on payment processing. Adding Shopify Capital — lending to merchants based on their sales data — adds a revenue stream with yields in the 10-30% range on capital deployed, with default rates significantly below traditional small business lending because repayment is embedded in the sales flow.

But the financial margin is only part of the story. The deeper strategic value is in retention, engagement, and data.

Retention: When a merchant's operating account, lending relationship, and payment processing all sit on the same platform, switching costs compound. Moving your Shopify store to WooCommerce is hard enough. Moving your Shopify store plus your Shopify Capital loan plus your Shopify Balance account is nearly unthinkable.

Engagement: Financial products create daily touchpoints. A merchant who checks their Shopify Balance account every morning is a merchant who is deeply embedded in the Shopify ecosystem. That frequency of interaction creates upsell opportunities, reduces churn, and deepens the relationship in ways that a quarterly invoice cycle never could.

Data: Every financial transaction generates data. A platform that processes payments, manages accounts, and underwrites loans has a comprehensive view of its customer's financial health. That data improves underwriting, informs product development, and creates feedback loops that traditional financial institutions cannot match because they only see the financial transaction, not the business activity that generated it.

The Infrastructure Providers: Who Actually Enables This

The companies building embedded finance infrastructure are the real winners in this market — at least so far.

Stripe Treasury

Stripe Treasury, launched in 2020, allows Stripe's existing payment processing customers to offer their users FDIC-insured bank accounts, money movement, and card issuing through the same Stripe APIs they already use for payments. The distribution advantage is enormous: Stripe's 3 million-plus businesses are already integrated. Adding banking is an incremental API call, not a new vendor relationship. Over 60 platforms have built on Stripe Treasury, partnering with Goldman Sachs and Citibank as the underlying bank partners.

Unit

Unit focuses specifically on embedded banking for software companies. Its platform connects to multiple sponsor banks and provides APIs for account opening, card issuing, ACH transfers, and lending. Unit's differentiation is compliance depth — it handles KYC, BSA/AML monitoring, and regulatory reporting on behalf of its platform customers, reducing the compliance burden that would otherwise fall on the software company.

Marqeta

Marqeta powers the card programs behind Cash App, DoorDash, Klarna, and Instacart. Its platform enables "just-in-time" funding — the ability to authorize and fund a card transaction in real time based on custom business logic. When a DoorDash driver swipes their DasherDirect card, Marqeta's system evaluates the transaction against DoorDash's rules and funds it instantly from the driver's earnings balance. Marqeta processed over $200 billion in total payment volume in 2024.

Plaid

Plaid sits in a different part of the embedded finance stack. Rather than enabling new financial products, Plaid connects existing ones. Its data connectivity APIs allow platforms to verify bank accounts, pull transaction history, and confirm income — the foundational data operations that underpin lending, payments, and account funding flows. Plaid connects to over 12,000 financial institutions and is integrated into thousands of fintech and embedded finance applications.

Who Wins and Who Loses

The embedded finance opportunity is large enough that multiple players can win — but they will not all win equally.

Infrastructure providers win the most. Stripe, Unit, Marqeta, and Plaid are building the picks-and-shovels layer of embedded finance. They earn fees on every transaction, every account, every card swipe — regardless of which platform succeeds or fails. Their revenue scales with the total volume of embedded financial activity, not with any single platform's success. This is the most structurally advantaged position in the embedded finance stack.

Platforms with proprietary data advantages win. Shopify, Amazon, and Uber can underwrite financial products using data that no traditional bank has access to. That data advantage translates to better risk assessment, lower default rates, and higher approval rates. It is a genuine, defensible competitive advantage that compounds over time as the data set grows.

Sponsor banks win — selectively. Cross River Bank, which partners with Affirm, Stripe, and Coinbase, earns net interest margin on the deposits and loans that flow through its charter. Column Bank, built from the ground up for BaaS, is positioned to capture the compliance-first segment of the market. But the Synapse collapse and subsequent regulatory crackdown have made clear that sponsor banks bear disproportionate regulatory risk relative to their economic share.

Traditional banks lose distribution. This is the hardest truth. If your customer's primary financial relationship is with Shopify — where they manage their business account, access working capital, and process payments — the traditional business banking relationship becomes redundant. The bank still provides the charter and the deposit insurance, but it loses the customer relationship, the data, and the ability to cross-sell. It becomes a utility.

Traditional banks lose underwriting advantage. A bank evaluating a small business loan application sees financial statements, tax returns, and credit scores. Shopify Capital evaluating the same merchant sees real-time sales data, customer acquisition trends, return rates, seasonal patterns, and marketing spend. The platform's data is fresher, richer, and more predictive. Over time, this data asymmetry will shift the best lending opportunities away from traditional banks and toward platforms.

The Risks Nobody Talks About Enough

Embedded finance is not without structural risks, and the industry's marketing materials systematically understate them.

Regulatory risk is real and increasing. The FDIC, OCC, and Federal Reserve have dramatically tightened oversight of bank-fintech partnerships since 2024. Consent orders against Evolve Bank & Trust and Blue Ridge Bank demonstrated that regulators will hold sponsor banks accountable for the compliance failures of their fintech partners. The Synapse bankruptcy — which left 100,000 customers unable to access their funds — demonstrated the catastrophic consequences of middleware failure.

Concentration risk is underappreciated. A small number of sponsor banks support a disproportionate share of the embedded finance ecosystem. If Cross River Bank or Column Bank faced regulatory action, the downstream impact on dozens of fintech platforms would be immediate and severe.

The "every company is a fintech" thesis has limits. Not every company has the data, the customer relationship, or the operational capacity to deliver financial products well. A food delivery company offering a debit card to its drivers is a sensible extension of the existing relationship. A mattress company offering a savings account is not. The embedded finance opportunity is real, but it is not universal.

The $7 Trillion Question

Embedded finance is not a trend. It is a structural reorganization of how financial services are distributed. The banks that built their businesses on controlling the customer relationship are watching that relationship migrate to software platforms. The platforms that control distribution are discovering that financial products are the highest-margin features they can offer.

The infrastructure layer — Stripe, Unit, Marqeta, Plaid — is the clearest winner because it is agnostic to which platforms succeed. The platforms with proprietary data advantages — Shopify, Amazon, Uber — are building lending and banking businesses that traditional banks cannot replicate. The sponsor banks that provide the regulatory foundation are necessary but increasingly commoditized.

The $7 trillion question is not whether this transition happens. It is how fast. And the answer, based on the evidence so far, is faster than the banking industry is prepared for.

Key Takeaways

- Embedded finance lets non-financial companies offer banking, lending, insurance, and payments directly within their platforms. The customer never leaves. The financial product is invisible infrastructure, not a standalone experience.

- The opportunity is structural, not cyclical. Bain estimated $7 trillion in embedded finance transaction value by 2026. The revenue pool for enablers is projected at $230 billion.

- Platforms with proprietary data — Shopify, Amazon, Uber — can underwrite financial products better than traditional banks because they see the business activity, not just the financial statement.

- Infrastructure providers (Stripe, Unit, Marqeta, Plaid) are the most structurally advantaged because they earn fees regardless of which platform wins.

- Traditional banks are being disintermediated from the customer relationship. They still provide the charter and deposit insurance, but they are becoming utilities rather than primary financial partners.

- The regulatory environment has tightened significantly since 2024. The Synapse collapse and subsequent enforcement actions have raised the cost and complexity of embedded finance, but have not slowed the fundamental shift.

Related Reading

- Banking-as-a-Service: How Fintech Companies Become Banks Overnight — The infrastructure layer that makes embedded finance possible, including what the Synapse collapse revealed about structural fragility.

- Open Banking Explained: What PSD2 and APIs Mean for Your Money — The regulatory framework forcing banks to share data, which accelerates the embedded finance shift.

- How Visa Processes Transactions — and What It Costs You — Understanding interchange economics is essential context for why platforms want to own the payment flow.

Related Articles

Open Banking Failed Its Promise — Here's What Actually Works

Open Banking promised a revolution. Adoption is low and APIs are fragmented. But the real winners are emerging in unexpected places.

How Central Bank Digital Currencies Will Change Finance

What are CBDCs and how will they change banking? A complete guide to central bank digital currencies, from China's digital yuan to the EU's digital euro.

What Is Embedded Finance? How Non-Banks Are Becoming Banks

What is embedded finance and why are non-banks offering financial services? A complete guide to embedded payments, lending, insurance, and banking as a service.