Regulation in Fintech - Use case : Rise of fraudulent lending apps in INDIA

Regulations are essential for key institutions in society, such as banking. Every government must strike a balance. Too much regulation creates bureaucracy and red tape, which can slow economic growth. Too little regulation can lead to chaos.

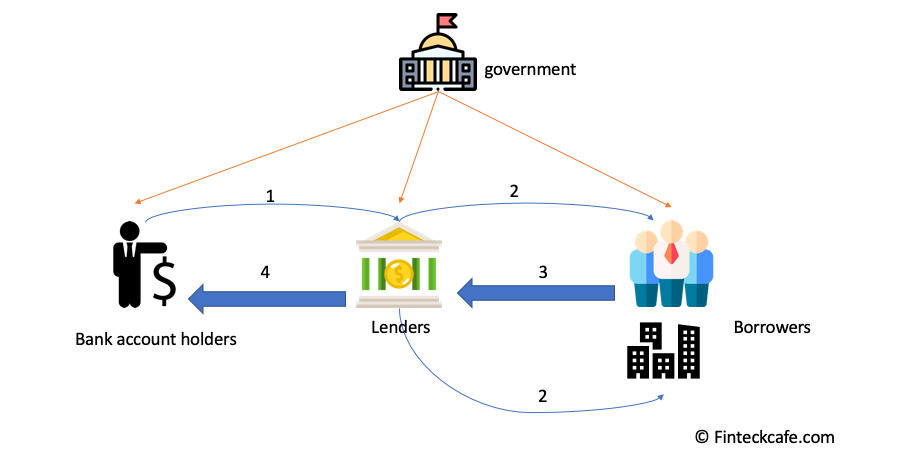

Let's look at a simple banking loan model shown below. Hard-working people ("depositors") save their money in banks (item (1) in the diagram below). For this example, let's say the bank's savings interest rate is 2%, which at least covers losses from inflation.

The bank collects all the deposited money and lends it to "borrowers" (item (2) in the diagram below). These borrowers may be getting personal loans or mortgage loans. The bank may also invest in low-risk options that provide higher returns. Let's say the lending interest rate is 5% for these loans.

The bank makes its profit from the difference between what it pays depositors and what it charges borrowers (items (3) and (4) in the diagram below). Banks also earn money by charging fees to both depositors and borrowers. These include loan service fees, overdraft fees, late fees, and more.

Local governments protect everyone involved in these transactions. This ensures no one has an unfair advantage. Society overall feels safe and protected.

Even with good banking and mortgage regulations in the U.S., no one was able to predict or prevent the subprime crisis of 2008. That crisis brought down the entire global economy.

One of the main causes was "predatory lending." Rising housing prices and low interest rates in the U.S. created the perfect environment for banks to take risks. Banks issued loans to borrowers who could not afford to repay them. When housing prices started to fall and interest rates increased, the economy spiraled downward.

The key lesson here is that there can be blind spots in regulation. Savvy players in the market will exploit these gaps. Predatory lending practices for any type of loan are bad for the banking system.

Lending Apps in INDIA

India has a growing middle class, widespread cell phone usage, and a booming tech scene. This makes it a strong market for all technologies, including fintech.

India's central bank, the Reserve Bank of India (RBI), regulates loan lending. Last month, the RBI issued a press release (Press Release: 2020-2021/819) warning citizens about unauthorized digital lending platforms and mobile apps. These apps claim to offer loans quickly and without hassle. The RBI also urged people to file complaints against such fraudulent apps.

Google powers 98% of India's smartphones. On January 14, 2021, Google published a blog post announcing a crackdown on fraudulent loan apps in India.

"We have reviewed hundreds of personal loan apps in India, based on flags submitted by users and government agencies. The apps that were found to violate our user safety policies were immediately removed from the Store, and we have asked the developers of the remaining identified apps to demonstrate that they comply with applicable local laws and regulations. Apps that fail to do so will be removed without further notice. In addition, we will continue to assist the law enforcement agencies in their investigation of this issue".Suzanne Frey, Vice President, Product, Android Security and Privacy (src: google blog post)

Google cited two key reasons for the crackdown.

(a) Protecting users from deceptive financial products and services: Google has strict rules for loan apps. These apps must disclose details like the minimum and maximum repayment periods and the APR (Annual Percentage Rate).

(b) Protecting user privacy: Google wants to make sure app developers do not ask for access to personal apps and services on the user's phone.

The loan companies reportedly gained access to users' personal contact lists on their phones. When borrowers failed to make payments, the companies called everyone on the contact list. This created unwanted trouble for the borrowers.

In this case, both the government body (RBI) and the technology platform provider (Google) are working together to enforce regulations and educate people.

Related Articles

Regulatory Risk in AI Deployment: What Leaders Underestimate

In 2023, the CFPB sent a clear message to every financial institution using AI for credit decisions: your algorithm is not above the law. Circular 2022-03

PCI DSS Compliance Explained: What Every Product Team Needs to Know

In December 2013, attackers installed malware on Target's point-of-sale systems and stole 40 million credit card numbers over 19 days. The breach cost Target