Fintech Newsletter for 6/05/21

Below is news related to the fintech industry this week.

General News

DeFi fuels cryptocurrency volatility

Decentralized finance (DeFi) is a set of financial services which uses Blockchain "smart contracts." Many financial services are popping up using DeFi, such as lending, derivatives, payments, exchanges, etc.

How does DeFi work? Why is it getting popular?

DeFi is a new experiment in finance and has got everyone curious and interested.

Lack of middlemen in financial services and consistent rule-driven "smart contracts" are the main reasons for the rise of DeFi popularity.

Let's take a look at the subprime mortgage lending crisis, which caused a global financial meltdown a decade ago. First, banks gave loans(mortgages) to homebuyers, and homebuyers paid monthly payments with interest. Then, banks got creative, pooled all their mortgages, and sold them as Mortgage(Asset) backed securities(MBS).

Above seems a logical pattern to create a financial instrument. However, the problem was giving more subprime mortgages, i.e., owners who did not have required credit scores (i.e., those who were likely to default on payments) got high-priced mortgages.

As the housing prices started to fall, the homeowners could not pay back their mortgage and defaulted. Thus, causing a spiraling effect and bringing down the financial and insurance institutions.

So in the above situation, human greed was on full display. The banks wanted to make more money, the subprime homebuyer who tried to buy a house that he couldn't afford, and of course hedge funds and other wall street banks that wanted to make money with the derivatives. Thus, we see a formation of the human "greed chain."

If DeFi were in place, the loan approval process would not go through an "underwriter" (i.e., bank person who approves a loan). Hence, removing the middleman and one component from the "greed chain." Instead, a borrower could directly get a loan using "dapps" (DeFi apps), and required rules are pre-defined in the smart contract not managed by a central institution.

So now, let's look at how DeFi based loans work. Let's say John wants to borrow $100 using DeFi.Mary has $10 in cryptocurrency in her digital wallet. And if Mary decides to accrue interest on her cryptocurrency, she would lend her cryptocurrency to a "Loan Pool."Once the loan pool has enough money, John can borrow the funds from the pool. Due to the volatile nature of cryptocurrency, the borrower has to "over collateralized," i.e., if John wants $100, he needs to have $150 of assets. So John, instead of going to the bank and borrowing $100 and getting approval from the bank's underwriting authority. He uses any of the DeFi lending dapps; he needs a digital wallet and some initial crypto assets as collateral to borrow a loan. And Mary will get the part of the interest paid by John to the pool.

All this is good, but how is this causing volatility in cryptocurrency?

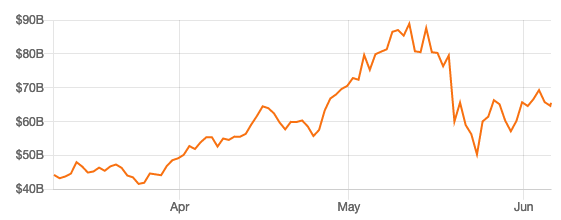

To understand the answer to the above question, we must first get to know Total Value Locked (TVL) - a measure of assets locked in the DeFi ecosystem.

Just May of last year, TVL was less than $1B. However, in the next twelve months, TVL rose to $90B -a lot of money flowing into the DeFi ecosystem in a short period.

Folks using dapps started to liquidate their assets when the cryptocurrency panic sell-off started.This liquidation started to fuel the further downfall of certain cryptocurrencies.

Ethereum is the most popular DeFi Blockchain network, which fuels a lot of dapps and ETH, a cryptocurrency on Ethereum saw this affect.

Data Source: Defi plus

In conclusion, albeit DeFi is convoluted and has only got the tech and finance savvy in the early race. However, as more venture money pours into the fintech space, DeFi based applications will continue to grow.

Will EPI use Russia's Mir Playbook to break MasterCard and Visa domination in Europe?

Last year European Payments Initiative (EPI) had proposed an initiative to a homegrown unified payment solution. However, such an initiative will be a blow to American card companies such as Mastercard and Visa.

Russia had a similar initiative with its own payment card company called MIR after its Crimea fiasco. The initiative started in 2015 has gathered momentum, and as per global data, as of 2020, nearly 75 million Mir cards are in circulation. However, the increase in the card distribution came from mandates provided by the Russian government to use Mir cards to receive funds from the government.

So if EPI wants to break into American cards in Europe, they would have to either provide mandates similar to Mir in Russia or heavily incentivize European consumers to use EPI cards.

With Cryptocurrencies and DeFi in vogue, It will be interesting to watch how the payment industry will evolve in Europe.

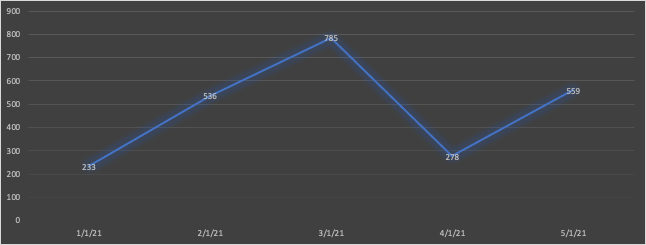

U.S Job number of May Release.

U.S bureau of labor statistics released the May total non-farm employment numbers. In May, employers added only 559K jobs. In April, employers added 278k jobs and 785k in March. The unemployment rate in April was at 6.1%, and for the current month of May, the unemployment rate was 5.8%.

Even though both numbers are better than last month and trending in the right direction, the market expects a faster job growth rate.

Fintech New Venture and IPO

- Synctera raises $33m Series A funding to pair fintechs with banks.

“We’re bringing community banks and FinTechs together. One part marketplace. One part Fintech-as-a-Service platform. Synctera gives you everything you need to stand up a successful partnership, freeing up time to focus on what you do best. By streamlining day-to-day reconciliation, regulatory compliance and operational processes, we unlock growth opportunities, increase efficiency, minimize compliance risk and accelerate speed to market.”-Synctera Team

- MotoRefi,a Washington D.C based auto loan refinancing platform,raised $45m in Series B funding.

- Jeeves,a New York based expense management platform for Latin America,raised $26M in Series A funding.

- Pinwheel, a New York based Payroll API for Neo-Banks,raised $20M in Series A funding.

- Spruce,a New York based title and residential closing tech platform,raised $60m in Series C funding.

- IDwall,a brasil based identity verification platform,raised $38m in Series C funding.

- Jai Kisan,a India based agriculture finance platform for rural India,raised $30m in Series A funding.

- Truebill,a Maryland based personal finance management app,raised $45m in Series D funding.

- Chipper,a San Francisco based payment platform focused on Africa,raised $100m in Series C funding.

If you have any comments or have any topic requests for the blog, please leave your feedback here.